Asset returns#

Let \(P_t\) be the price of an asset at time \(t\). We’ll define the gross return on the asset over one period as

where \(D_t\) denotes the value of any dividends paid during the period.

The net return is simply

The first term is the capital gains yield and the second is the dividend yield.

import wrds

db = wrds.Connection()

Loading library list...

Done

As an example, we’ll work with some historical price data for Apple.

sql = """

SELECT dlycaldt, dlyprc, dlyret, dlyretx

FROM crsp.dsf_v2

WHERE permno = 14593

AND dlycaldt >= '01/01/2019' AND dlycaldt <= '12/31/2020'

"""

aapl = db.raw_sql(sql, date_cols=['dlycaldt'])

aapl = (aapl

.rename(columns={'dlycaldt': 'date', 'dlyprc': 'prc', 'dlyret': 'ret', 'dlyretx': 'retx'})

.set_index('date')

.sort_index())

aapl.loc['2020-08']

| prc | ret | retx | |

|---|---|---|---|

| date | |||

| 2020-08-03 | 435.75 | 0.025198 | 0.025198 |

| 2020-08-04 | 438.66 | 0.006678 | 0.006678 |

| 2020-08-05 | 440.25 | 0.003625 | 0.003625 |

| 2020-08-06 | 455.61 | 0.034889 | 0.034889 |

| 2020-08-07 | 444.45 | -0.022695 | -0.024495 |

| 2020-08-10 | 450.91 | 0.014535 | 0.014535 |

| 2020-08-11 | 437.50 | -0.029740 | -0.029740 |

| 2020-08-12 | 452.04 | 0.033234 | 0.033234 |

| 2020-08-13 | 460.04 | 0.017698 | 0.017698 |

| 2020-08-14 | 459.63 | -0.000891 | -0.000891 |

| 2020-08-17 | 458.43 | -0.002611 | -0.002611 |

| 2020-08-18 | 462.25 | 0.008333 | 0.008333 |

| 2020-08-19 | 462.83 | 0.001255 | 0.001255 |

| 2020-08-20 | 473.10 | 0.022190 | 0.022190 |

| 2020-08-21 | 497.48 | 0.051532 | 0.051532 |

| 2020-08-24 | 503.43 | 0.011960 | 0.011960 |

| 2020-08-25 | 499.30 | -0.008204 | -0.008204 |

| 2020-08-26 | 506.09 | 0.013599 | 0.013599 |

| 2020-08-27 | 500.04 | -0.011954 | -0.011954 |

| 2020-08-28 | 499.23 | -0.001620 | -0.001620 |

| 2020-08-31 | 129.04 | 0.033912 | 0.033912 |

CRSP provides two return variables:

retis the total return, \(R_t\);retxexcludes the dividend (i.e. it is the capital gains yield).

Note

CRSP makes data available in both daily and monthly files. Variables in the daily file are often prepended with dly and those in the monthly file with mth. So the date in one file is dlycaldt while in the other it’s mthcaldt. Similarly, we have dlyret and mthret, and so on.

Notice that

so we can recover the dividend from the difference in these two series by multiplying by the lagged price. And, obviously, if the dividend is zero the two returns will be identical.

divs = (aapl['ret'] - aapl['retx']) * aapl['prc'].shift()

divs[divs>0].round(3)

date

2019-02-08 0.730

2019-05-10 0.770

2019-08-09 0.770

2019-11-07 0.770

2020-02-07 0.770

2020-05-08 0.820

2020-08-07 0.820

2020-11-06 0.205

dtype: float64

db.raw_sql("""

SELECT disexdt, disdivamt, disdeclaredt, disrecorddt, dispaydt

FROM crsp.stkdistributions

WHERE permno = 14593 AND disordinaryflg = 'Y'

AND disexdt >= '01/01/2019' AND disexdt <= '12/31/2020'

""",

date_cols=['disexdt', 'disdeclaredt', 'disrecorddt', 'dispaydt'])

| disexdt | disdivamt | disdeclaredt | disrecorddt | dispaydt | |

|---|---|---|---|---|---|

| 0 | 2019-02-08 | 0.730 | 2019-01-29 | 2019-02-11 | 2019-02-14 |

| 1 | 2019-05-10 | 0.770 | 2019-04-30 | 2019-05-13 | 2019-05-16 |

| 2 | 2019-08-09 | 0.770 | 2019-07-30 | 2019-08-12 | 2019-08-15 |

| 3 | 2019-11-07 | 0.770 | 2019-10-30 | 2019-11-11 | 2019-11-14 |

| 4 | 2020-02-07 | 0.770 | 2020-01-28 | 2020-02-10 | 2020-02-13 |

| 5 | 2020-05-08 | 0.820 | 2020-04-30 | 2020-05-11 | 2020-05-14 |

| 6 | 2020-08-07 | 0.820 | 2020-07-30 | 2020-08-10 | 2020-08-13 |

| 7 | 2020-11-06 | 0.205 | 2020-10-29 | 2020-11-09 | 2020-11-12 |

Compound returns#

Holding the asset for \(k\) periods would earn a gross return of

That is, the \(k\)-period return is simply the product of the \(k\) one-period returns; for this reason it is also called the compound return.

Assets may generate a return that is compounded over varying intervals. For example, an asset generating a return per year of \(R\) but compouning \(n\) times per year will have a total return of

R = 0.1

prds = [1, 2, 4, 12, 52, 365, 24*365]

vals = [(1+R/n)**n for n in prds]

tbl = pd.DataFrame(vals, index=prds, columns=['Gross return'])

tbl.index.name = 'Frequency'

tbl

| Gross return | |

|---|---|

| Frequency | |

| 1 | 1.100000 |

| 2 | 1.102500 |

| 4 | 1.103813 |

| 12 | 1.104713 |

| 52 | 1.105065 |

| 365 | 1.105156 |

| 8760 | 1.105170 |

In the limit this leads to a continuous compounding,

With continuous compounding, the asset value after one year is

np.exp(0.1)

np.float64(1.1051709180756477)

Log returns#

The log return, or continuously compounded return is

where \(\Delta x_t := x_t - x_{t-1}\) is the difference operator.

The multiperiod log return is simply the sum of the continuously compounded one-period returns.

Using the first-order Taylor expansion of \(\ln(1+x)\) we can see that

so, for small returns, the log return will be close to the net return; this similarity breaks down as price changes become larger.

Exercise

Calculate the log return using Apple’s returns. On what dates is the difference between the log return and the standard return greater than 0.005?

Solution

aapl['logret'] = np.log(1+aapl['ret'])

# create a "mask" of Boolean values to select rows

mask = (aapl['logret'] - aapl['ret']).abs() > 0.005

aapl[mask]

We can see that the returns differ on days when Apple’s return is either very high or very low bigger than about 9% in absolute value.

Aggregating returns#

aapl.resample('ME')['logret'].sum().head()

date

2019-01-31 0.053687

2019-02-28 0.043799

2019-03-31 0.092601

2019-04-30 0.054900

2019-05-31 -0.132581

Freq: ME, Name: logret, dtype: float64

aapl.resample('ME')['ret'].apply(lambda x: (1+x).product()-1).head()

date

2019-01-31 0.055154

2019-02-28 0.044772

2019-03-31 0.097024

2019-04-30 0.056435

2019-05-31 -0.124168

Freq: ME, Name: ret, dtype: float64

We can compare these to the monthly return data in CRSP.

db.raw_sql("""

SELECT mthcaldt, mthprc, mthret, mthretx

FROM crsp.msf_v2

WHERE permno = 14593

AND mthcaldt >= '01/01/2019' AND mthcaldt <= '06/30/2019'

""")

| mthcaldt | mthprc | mthret | mthretx | |

|---|---|---|---|---|

| 0 | 2019-01-31 | 166.44 | 0.055154 | 0.055154 |

| 1 | 2019-02-28 | 173.15 | 0.044771 | 0.040315 |

| 2 | 2019-03-29 | 189.95 | 0.097026 | 0.097026 |

| 3 | 2019-04-30 | 200.67 | 0.056436 | 0.056436 |

| 4 | 2019-05-31 | 175.07 | -0.124166 | -0.127573 |

| 5 | 2019-06-28 | 197.92 | 0.130519 | 0.130519 |

When we resample, we can aggregate data with numerous arbitrary functions.

# quarterly return statistics

aapl.resample('QE')['ret'].agg(['mean', 'std', 'min', 'max'])

| mean | std | min | max | |

|---|---|---|---|---|

| date | ||||

| 2019-03-31 | 0.003335 | 0.020664 | -0.099607 | 0.068335 |

| 2019-06-30 | 0.000845 | 0.016248 | -0.058120 | 0.049086 |

| 2019-09-30 | 0.002132 | 0.016704 | -0.052348 | 0.042348 |

| 2019-12-31 | 0.004351 | 0.011300 | -0.025068 | 0.028381 |

| 2020-03-31 | -0.001418 | 0.041778 | -0.128647 | 0.119808 |

| 2020-06-30 | 0.006022 | 0.021979 | -0.052617 | 0.087238 |

| 2020-09-30 | 0.004156 | 0.028080 | -0.080061 | 0.104689 |

| 2020-12-31 | 0.002386 | 0.021687 | -0.056018 | 0.063521 |

Constructing a price index#

1+aapl['ret'].head()

date

2019-01-02 1.001141

2019-01-03 0.900393

2019-01-04 1.042689

2019-01-07 0.997774

2019-01-08 1.019063

Name: ret, dtype: float64

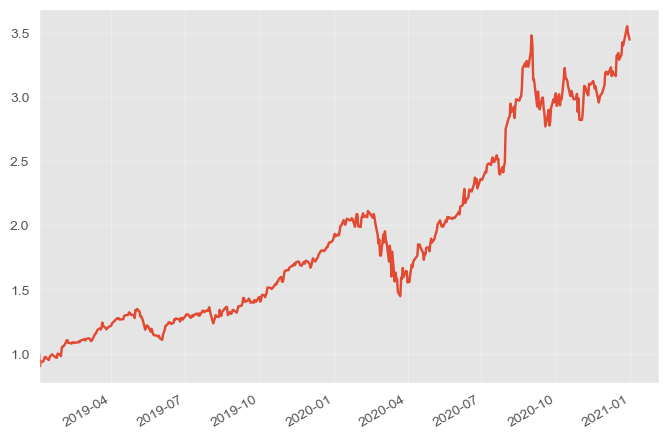

ax = (1+aapl['ret']).cumprod().plot(xlabel='')

ax.grid(alpha=0.3)

ax.set_xlim(aapl.index[0], None)

plt.show()

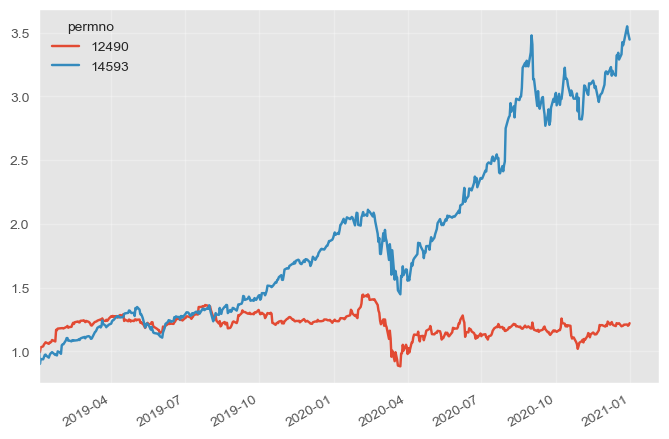

rets = db.raw_sql("""

SELECT permno, dlycaldt, dlyret

FROM crsp.dsf_v2

WHERE permno IN (14593, 12490)

AND dlycaldt >= '01/01/2019' AND dlycaldt <= '12/31/2020'

""", date_cols=['dlycaldt'])

rets.head()

| permno | dlycaldt | dlyret | |

|---|---|---|---|

| 0 | 12490 | 2019-01-02 | 0.013548 |

| 1 | 12490 | 2019-01-03 | -0.019964 |

| 2 | 12490 | 2019-01-04 | 0.039058 |

| 3 | 12490 | 2019-01-07 | 0.007075 |

| 4 | 12490 | 2019-01-08 | 0.014219 |

rets = rets.pivot(index='dlycaldt', columns='permno', values='dlyret')

rets.head()

| permno | 12490 | 14593 |

|---|---|---|

| dlycaldt | ||

| 2019-01-02 | 0.013548 | 0.001141 |

| 2019-01-03 | -0.019964 | -0.099607 |

| 2019-01-04 | 0.039058 | 0.042689 |

| 2019-01-07 | 0.007075 | -0.002226 |

| 2019-01-08 | 0.014219 | 0.019063 |

ax = (1+rets).cumprod().plot(xlabel='')

ax.grid(alpha=0.3)

ax.set_xlim(rets.index[0], None)

plt.show()

Exercise

Calculate the total return for Apple during the period of April–June, 2020 three different ways:

Use the price index we just created to calculate the desired return.

Aggregate the daily return series.

Separately download the monthly returns from CRSP and aggregate those.

Verify that all three methods yield the same result.

Solution

# using a price index

pidx = (1+rets[14593]).cumprod()

r1 = pidx.loc['2020-06-30'] / pidx.loc['2020-03-31'] - 1

# aggregating daily returns

r2 = rets[14593].resample('QE').apply(lambda x: (1+x).prod()-1).loc['2020-06']

# using monthly returns

mthrets = db.raw_sql("""

SELECT mthcaldt, mthret

FROM crsp.msf_v2

WHERE permno = 14593 and mthcaldt between '4/1/2020' and '6/30/2020'

""", date_cols=['mthcaldt'], index_col='mthcaldt')

r3 = (1+mthrets).prod() - 1

# check that r1, r2, and r3 are the same

print([x.item() for x in [r1, r2, r3]])

Day and night returns#

Exercise

The SPDR S&P 500 Trust ETF, introduced in 1993, is an exchange-traded fund that tracks the performance of the S&P 500 Index.

Download the complete history of price data for this ETF. You’ll need to first find its

permno.Calculate the return earned while the market is open (Open-to-Close) and the overnight return (Close-to-Open).

Confirm that the total day-time and overnight return equals close-to-close return.

Calculate the volatility of each return. Interpret your finding.

Calculate and plot the cumulative return of the day and night returns. What do you learn from the graph?

Calculate the day and night returns for each year. Create a bar chart showing the returns by year. Do you notice any interesting pattern to the data?

You can read more about this empirical fact in this article in the New York Times. Two recent research articles that further explore this phenomenon are: