import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from statsmodels.tsa.ar_model import AutoReg, ar_select_order

from statsmodels.tsa.regime_switching.markov_autoregression import MarkovAutoregression

import pandas_datareader as pdr

Markov Switching model#

A times series \({x_t}\) follows a Markov switching autoregressive model if

with \(\varepsilon_{k,t}\sim N(0,\sigma_k^2)\).

This model has two states or regimes, denoted by \(S_t\), indicating which state we are in at each time. In each state, a different equation describes how \(x_t\) changes over time.

Note

Pay attention to the subscripts; they provide important information. This is saying that the variance, \(\sigma_k^2\), is different for each \(k\) — meaning for each equation, or state of the world, there are two different variances.

The state variable \(S_t\) is a Markov chain with transition probabilities

In words, this says that the probability of transitioning from state 0 to state 1 is \(\eta_0\), and the probability of transitioning from state 1 to state 0 is \(\eta_1\). These \(\eta\)s are additional parameters that we must estimate from the data. Note also that the rows of the transition matrix sum to one.

More generally, we can have a model with \(k\) different states, in which case we have \(k\) equations for \(x_t\) and a \(k\times k\) transition matrix.

GDP growth#

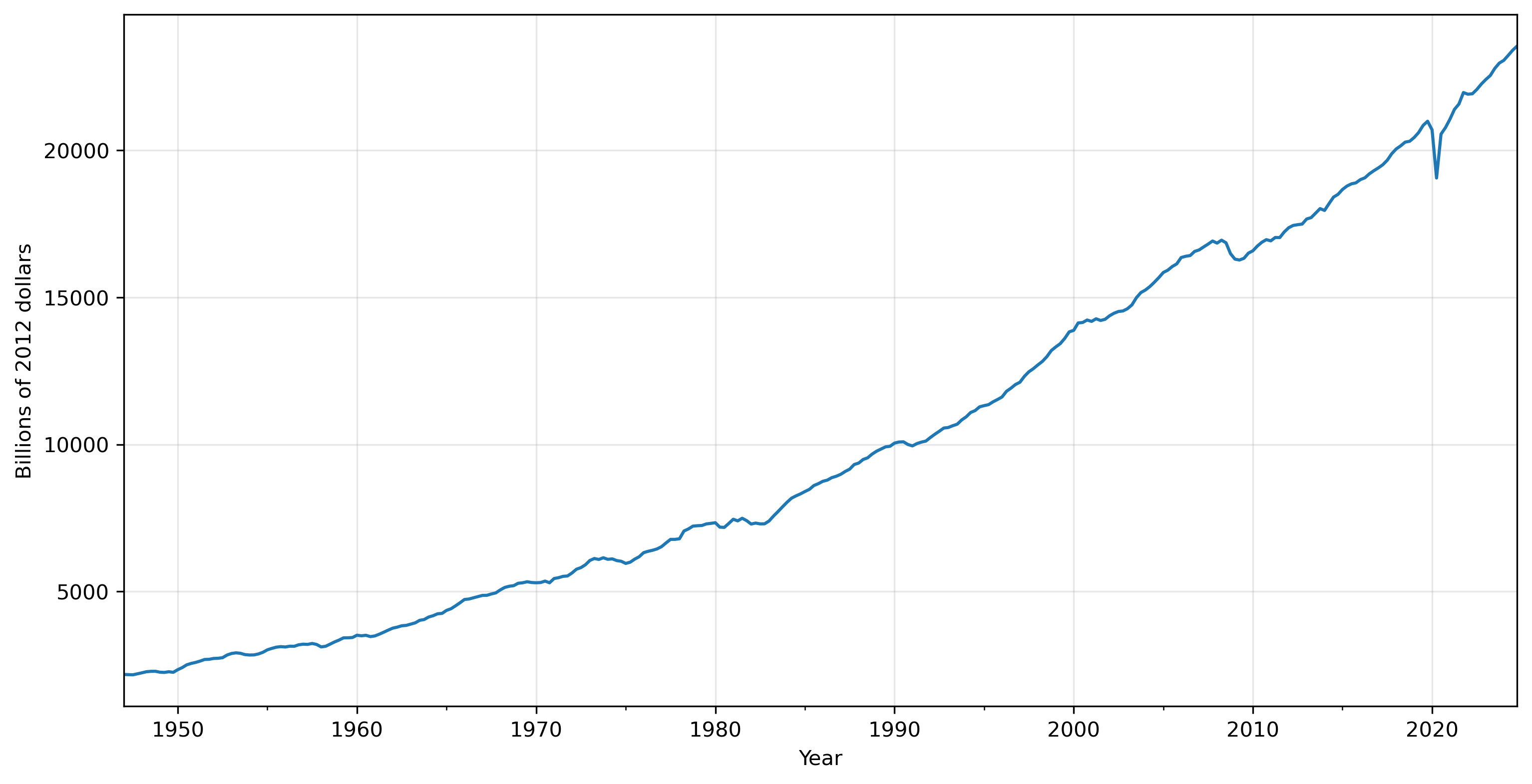

We’ll use the Real Gross Domestic Product series (in Billions of Chained 2012 Dollars, Seasonally Adjusted)

https://fred.stlouisfed.org/series/GDPC1

gdp = pdr.get_data_fred('GDPC1', 1947)

# set index frequency to quarterly

gdp = gdp.asfreq('QS')

gdp.plot(xlabel='Year', ylabel='Billions of 2012 dollars', grid=True, legend=False);

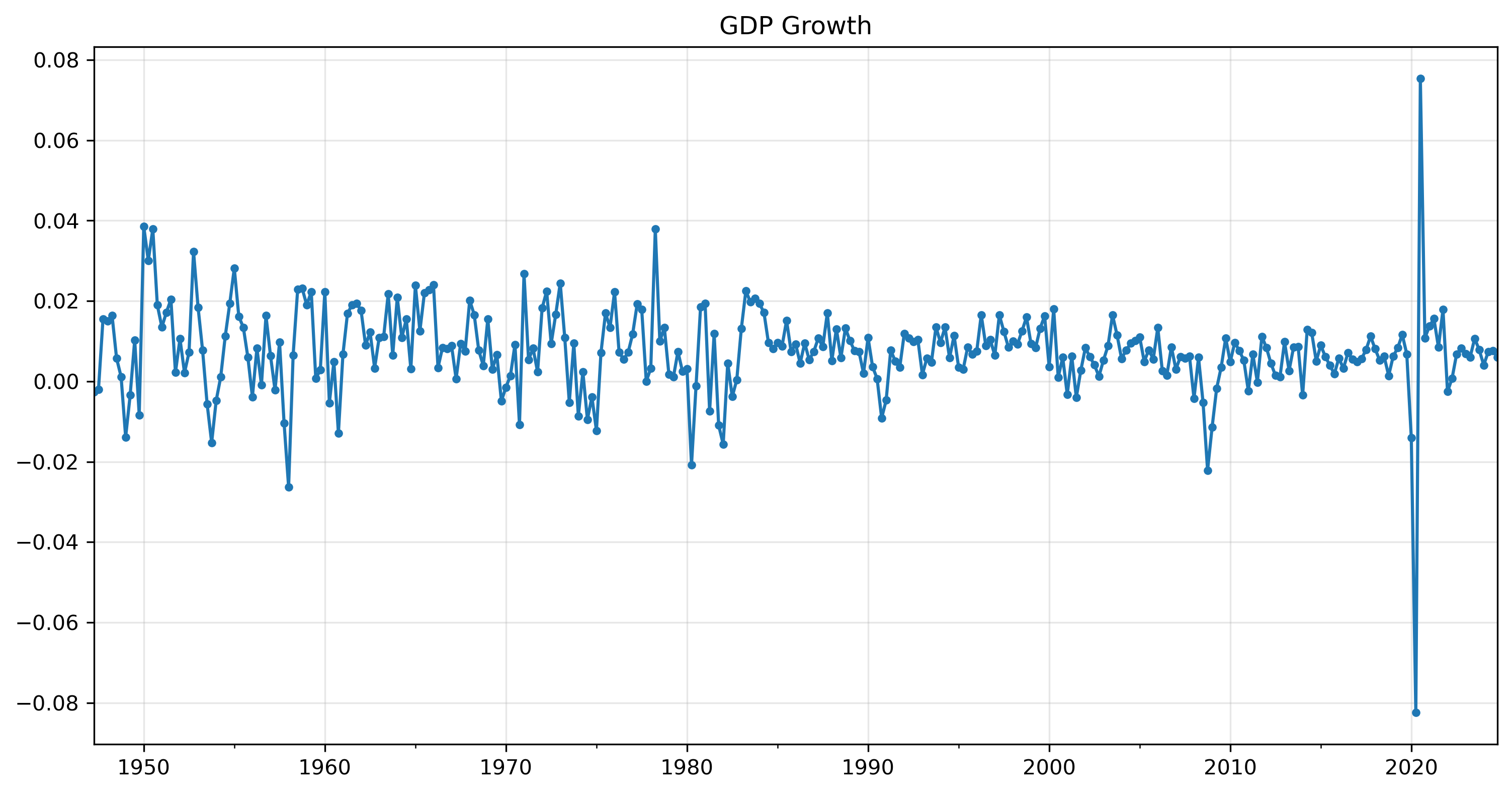

gdpgr = np.log(gdp).diff().dropna()

gdpgr.plot(marker='.', title='GDP Growth', legend=None, xlabel='', grid=True);

# restrict series to pre-COVID period

gdpgr = gdpgr.loc[:'2019']

gdpgr.describe()

| GDPC1 | |

|---|---|

| count | 291.000000 |

| mean | 0.007778 |

| std | 0.009282 |

| min | -0.026302 |

| 25% | 0.003114 |

| 50% | 0.007701 |

| 75% | 0.012460 |

| max | 0.038564 |

modsel = ar_select_order(gdpgr, maxlag=12, old_names=False, ic='aic')

modsel.ar_lags

[1, 2, 3]

gdpgr_ar3 = AutoReg(gdpgr, 3, old_names=False).fit()

print(gdpgr_ar3.summary())

AutoReg Model Results

==============================================================================

Dep. Variable: GDPC1 No. Observations: 291

Model: AutoReg(3) Log Likelihood 963.626

Method: Conditional MLE S.D. of innovations 0.009

Date: Tue, 15 Apr 2025 AIC -1917.253

Time: 08:01:05 BIC -1898.938

Sample: 01-01-1948 HQIC -1909.913

- 10-01-2019

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0049 0.001 6.467 0.000 0.003 0.006

GDPC1.L1 0.3323 0.058 5.697 0.000 0.218 0.447

GDPC1.L2 0.1519 0.061 2.498 0.012 0.033 0.271

GDPC1.L3 -0.1168 0.058 -2.008 0.045 -0.231 -0.003

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 -2.0707 -0.0000j 2.0707 -0.5000

AR.2 1.6856 -1.1375j 2.0335 -0.0945

AR.3 1.6856 +1.1375j 2.0335 0.0945

-----------------------------------------------------------------------------

Start with a simple model where only the mean varies between the states.

gdpgr_mod = MarkovAutoregression(gdpgr, k_regimes=2, order=3, switching_ar=False)

gdpgr_res = gdpgr_mod.fit(disp=True)

print(gdpgr_res.summary())

Optimization terminated successfully.

Current function value: -3.372021

Iterations: 57

Function evaluations: 72

Gradient evaluations: 72

Markov Switching Model Results

================================================================================

Dep. Variable: GDPC1 No. Observations: 288

Model: MarkovAutoregression Log Likelihood 971.142

Date: Tue, 15 Apr 2025 AIC -1926.284

Time: 08:01:07 BIC -1896.980

Sample: 04-01-1947 HQIC -1914.541

- 10-01-2019

Covariance Type: approx

Regime 0 parameters

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const -0.0136 0.004 -3.591 0.000 -0.021 -0.006

Regime 1 parameters

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0084 0.001 11.122 0.000 0.007 0.010

Non-switching parameters

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

sigma2 5.673e-05 5.48e-06 10.347 0.000 4.6e-05 6.75e-05

ar.L1 0.3864 0.061 6.299 0.000 0.266 0.507

ar.L2 0.2276 0.078 2.924 0.003 0.075 0.380

ar.L3 -0.2170 0.070 -3.117 0.002 -0.353 -0.081

Regime transition parameters

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

p[0->0] 3.2e-12 nan nan nan nan nan

p[1->0] 0.0293 0.015 1.961 0.050 1.44e-05 0.059

==============================================================================

Warnings:

[1] Covariance matrix calculated using numerical (complex-step) differentiation.

Looking at the estimates of the transition probability, it’s clear that the optimizer didn’t find a good solution, which is why the standard errors on the probabilities are infinite. The likelihood function was likely not actually maximized. Let’s try again with a bit more control over the optmizer.

We should get a log-likelihood of about 974.

gdpgr_mod2 = MarkovAutoregression(gdpgr, k_regimes=2, order=3, switching_ar=False)

Optimization terminated successfully.

Current function value: -3.381781

Iterations: 30

Function evaluations: 38

Gradient evaluations: 38

Markov Switching Model Results

================================================================================

Dep. Variable: GDPC1 No. Observations: 288

Model: MarkovAutoregression Log Likelihood 973.953

Date: Tue, 15 Apr 2025 AIC -1931.906

Time: 08:01:54 BIC -1902.602

Sample: 04-01-1947 HQIC -1920.163

- 10-01-2019

Covariance Type: approx

Regime 0 parameters

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const -0.0122 0.003 -4.177 0.000 -0.018 -0.006

Regime 1 parameters

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0089 0.001 11.241 0.000 0.007 0.010

Non-switching parameters

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

sigma2 5.015e-05 5.27e-06 9.518 0.000 3.98e-05 6.05e-05

ar.L1 0.4410 0.066 6.717 0.000 0.312 0.570

ar.L2 0.2594 0.069 3.748 0.000 0.124 0.395

ar.L3 -0.2662 0.069 -3.836 0.000 -0.402 -0.130

Regime transition parameters

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

p[0->0] 0.2316 0.138 1.682 0.093 -0.038 0.501

p[1->0] 0.0416 0.018 2.319 0.020 0.006 0.077

==============================================================================

Warnings:

[1] Covariance matrix calculated using numerical (complex-step) differentiation.

The DataFrame below shows how the parameter values changed through the iteration steps.

param_store.param_history

| p[0->0] | p[1->0] | const[0] | const[1] | sigma2 | ar.L1 | ar.L2 | ar.L3 | Log-Like | |

|---|---|---|---|---|---|---|---|---|---|

| iteration | |||||||||

| 1 | 0.207039 | 0.028825 | -0.011880 | 0.008544 | 0.000056 | 0.292192 | 0.163504 | -0.163383 | 969.920612 |

| 2 | 0.207039 | 0.028825 | -0.011911 | 0.008622 | 0.000056 | 0.292201 | 0.163514 | -0.163386 | 969.928504 |

| 3 | 0.207039 | 0.028825 | -0.012120 | 0.008609 | 0.000056 | 0.292273 | 0.163591 | -0.163407 | 969.942013 |

| 4 | 0.207046 | 0.028832 | -0.012225 | 0.008616 | 0.000056 | 0.302166 | 0.174178 | -0.166545 | 970.485798 |

| 5 | 0.207056 | 0.028874 | -0.012492 | 0.008636 | 0.000055 | 0.324868 | 0.194296 | -0.183971 | 971.495154 |

| 6 | 0.207088 | 0.029050 | -0.013029 | 0.008694 | 0.000052 | 0.374596 | 0.236686 | -0.227985 | 973.074853 |

| 7 | 0.207216 | 0.029423 | -0.013549 | 0.008761 | 0.000051 | 0.430162 | 0.277880 | -0.274869 | 973.552750 |

| 8 | 0.207285 | 0.029530 | -0.013189 | 0.008739 | 0.000052 | 0.425794 | 0.263744 | -0.262679 | 973.625840 |

| 9 | 0.207402 | 0.029738 | -0.013306 | 0.008743 | 0.000052 | 0.428603 | 0.256207 | -0.258248 | 973.652543 |

| 10 | 0.207699 | 0.030254 | -0.013267 | 0.008752 | 0.000051 | 0.437020 | 0.248603 | -0.255674 | 973.679306 |

| 11 | 0.208042 | 0.030826 | -0.013247 | 0.008758 | 0.000051 | 0.441883 | 0.246273 | -0.256050 | 973.699708 |

| 12 | 0.208680 | 0.031882 | -0.013168 | 0.008769 | 0.000051 | 0.446550 | 0.244904 | -0.257256 | 973.736175 |

| 13 | 0.209896 | 0.033938 | -0.013000 | 0.008788 | 0.000051 | 0.451137 | 0.244816 | -0.259621 | 973.799291 |

| 14 | 0.212335 | 0.038309 | -0.012621 | 0.008827 | 0.000050 | 0.454306 | 0.247976 | -0.264062 | 973.890612 |

| 15 | 0.214269 | 0.041913 | -0.012260 | 0.008860 | 0.000050 | 0.450723 | 0.253989 | -0.267176 | 973.931406 |

| 16 | 0.214585 | 0.042268 | -0.012190 | 0.008867 | 0.000050 | 0.445428 | 0.257661 | -0.267334 | 973.941682 |

| 17 | 0.214557 | 0.041812 | -0.012226 | 0.008863 | 0.000050 | 0.440825 | 0.259826 | -0.266630 | 973.944946 |

| 18 | 0.214592 | 0.041656 | -0.012239 | 0.008859 | 0.000050 | 0.440421 | 0.259797 | -0.266355 | 973.945102 |

| 19 | 0.214790 | 0.041510 | -0.012255 | 0.008855 | 0.000050 | 0.440127 | 0.259697 | -0.266056 | 973.945308 |

| 20 | 0.215271 | 0.041369 | -0.012270 | 0.008851 | 0.000050 | 0.439869 | 0.259581 | -0.265729 | 973.945669 |

| 21 | 0.216236 | 0.041225 | -0.012284 | 0.008846 | 0.000050 | 0.439625 | 0.259454 | -0.265371 | 973.946315 |

| 22 | 0.218119 | 0.041073 | -0.012298 | 0.008842 | 0.000050 | 0.439407 | 0.259305 | -0.264968 | 973.947459 |

| 23 | 0.221823 | 0.040935 | -0.012307 | 0.008839 | 0.000050 | 0.439297 | 0.259134 | -0.264572 | 973.949340 |

| 24 | 0.229164 | 0.040937 | -0.012293 | 0.008842 | 0.000050 | 0.439619 | 0.258998 | -0.264486 | 973.951655 |

| 25 | 0.231531 | 0.041167 | -0.012263 | 0.008851 | 0.000050 | 0.440169 | 0.259116 | -0.265053 | 973.952458 |

| 26 | 0.232263 | 0.041530 | -0.012220 | 0.008864 | 0.000050 | 0.440909 | 0.259364 | -0.266000 | 973.952934 |

| 27 | 0.231739 | 0.041597 | -0.012213 | 0.008866 | 0.000050 | 0.441025 | 0.259427 | -0.266200 | 973.952960 |

| 28 | 0.231586 | 0.041600 | -0.012213 | 0.008866 | 0.000050 | 0.441026 | 0.259434 | -0.266218 | 973.952960 |

| 29 | 0.231578 | 0.041599 | -0.012213 | 0.008866 | 0.000050 | 0.441024 | 0.259433 | -0.266219 | 973.952961 |

| 30 | 0.231578 | 0.041599 | -0.012213 | 0.008866 | 0.000050 | 0.441024 | 0.259433 | -0.266220 | 973.952961 |

We have two states, with constant terms \(\phi_{0,0} = -0.0122\) and \(\phi_{0,1} = 0.0089\). Clearly, the first state is a low-growth (or “recession”) state and the second state is the high-growth state.

The transition probability matrix is

so if you’re in the high-growth state, there’s about a 96% chance you’ll stay there, but if you’re in the recession state there’s a 77% chance you’ll transition out of it. If you think about how long recessions last, this makes perfect sense.

The expected duration of the two states are given by \(\frac{1}{0.7685}\) and \(\frac{1}{0.0415}.\)

gdpgr_res2.expected_durations

array([ 1.30136812, 24.0389007 ])

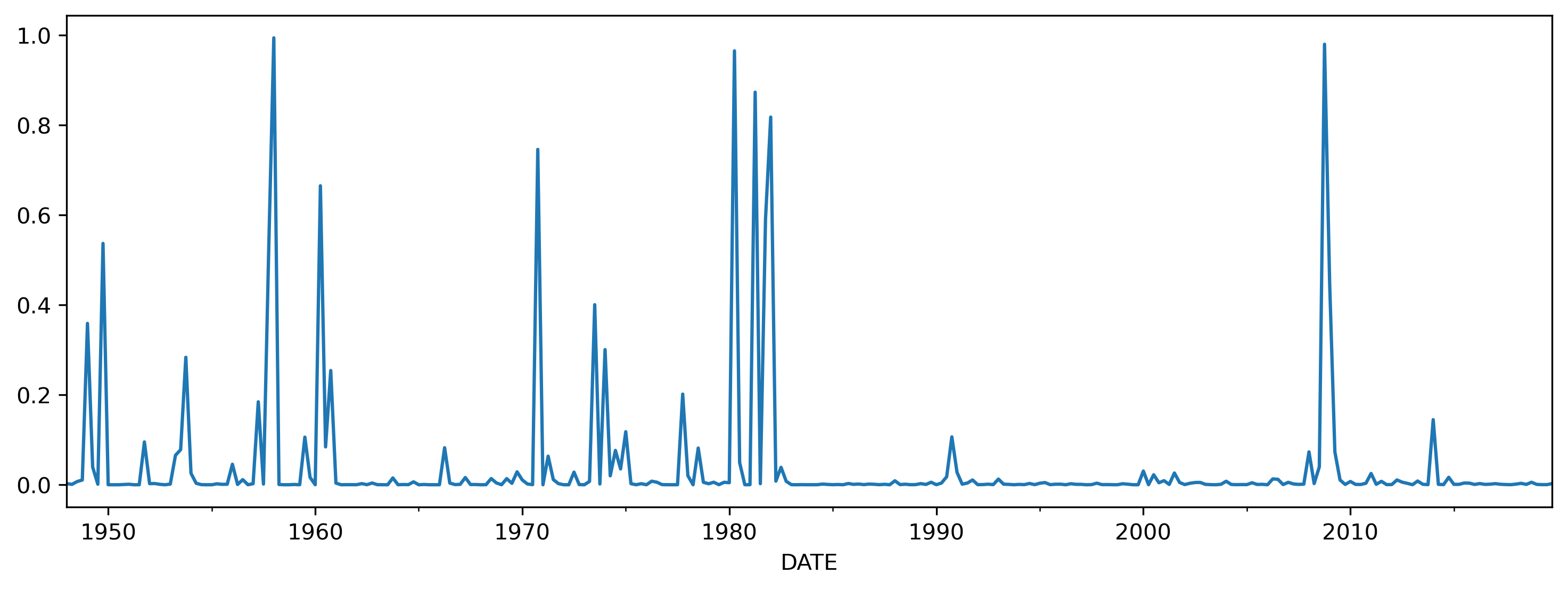

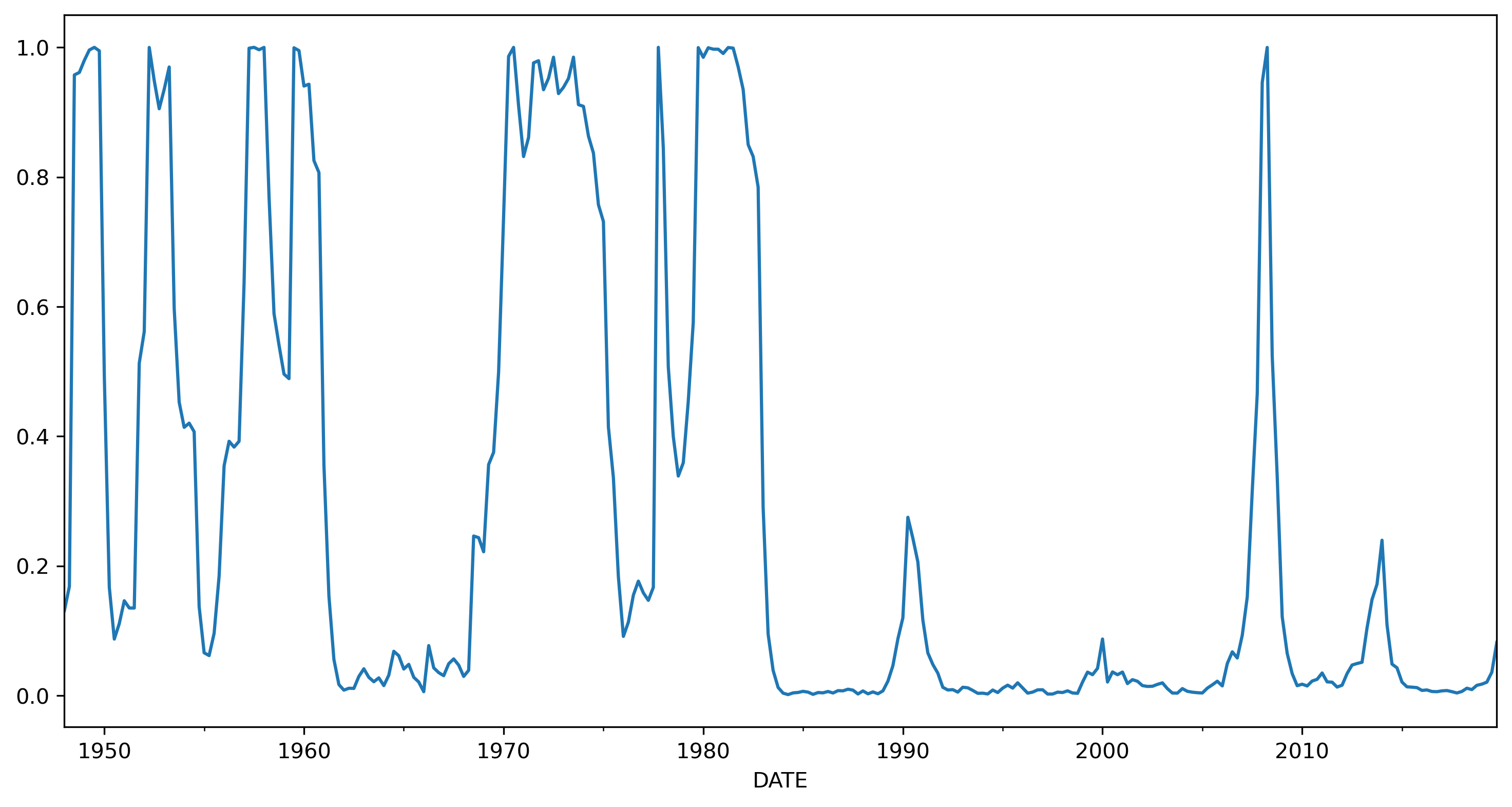

Let’s look at the filtered probabilities of state 0.

gdpgr_res2.filtered_marginal_probabilities[0].plot(figsize=(12,4))

<Axes: xlabel='DATE'>

# get NBER recessions data

usrec = pdr.get_data_fred('USREC', start=1947).squeeze()

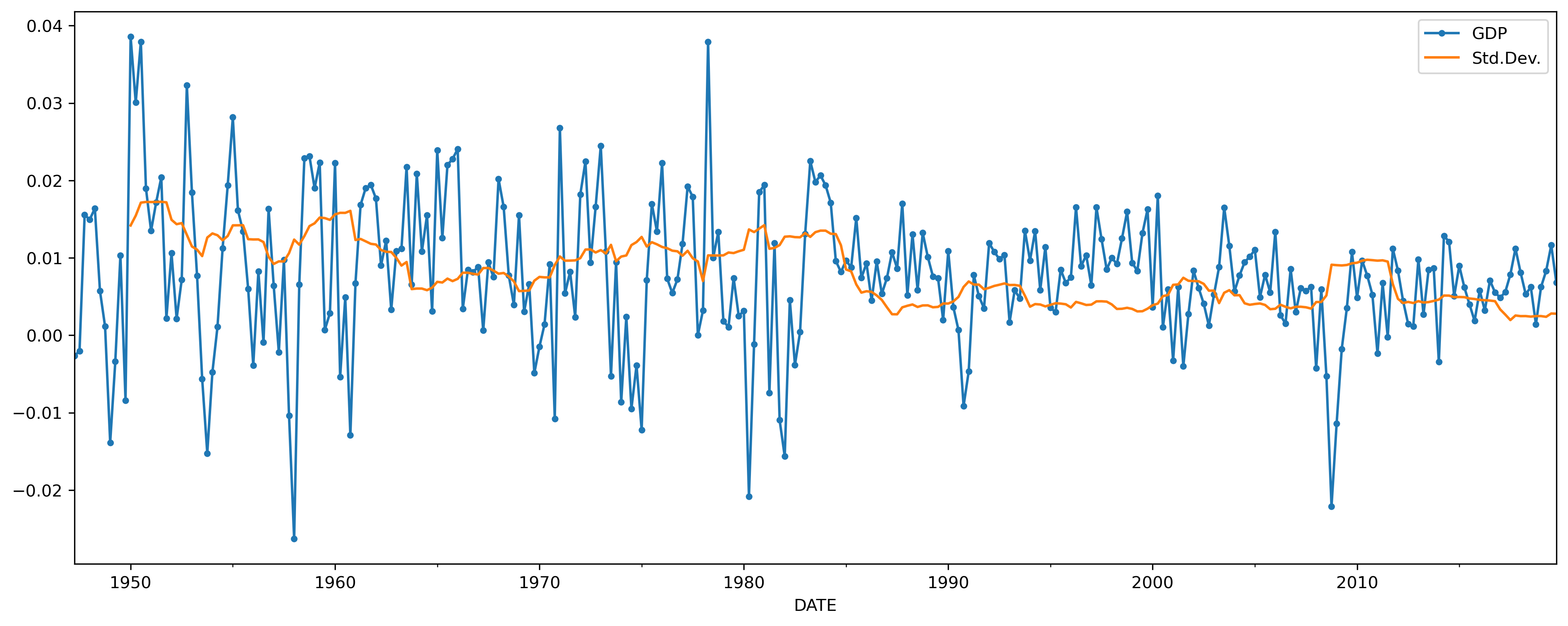

The Great Moderation#

ax = gdpgr.loc[:'2019'].plot(figsize=(16,6), marker='.')

gdpgr.rolling(4*3).std().plot(ax=ax)

ax.legend(['GDP', 'Std.Dev.'])

<matplotlib.legend.Legend at 0x176d657f0>

The volatility in the series after 1985 is about half of what it is before that.

gdpgr[:'1985'].std()

GDPC1 0.011468

dtype: float64

gdpgr['1985':].std()

GDPC1 0.005629

dtype: float64

This decline in the volatility of GDP growth is known as the Great Moderation.

We can estimate a Markov Switching Model where the autoregressive structure changes depending on which state we are in.

mod_gdpgr2 = MarkovAutoregression(gdpgr, k_regimes=2, order=3,

switching_ar=True,

switching_variance=True)

res_gdpgr2 = mod_gdpgr2.fit(disp=True)

print(res_gdpgr2.summary())

Optimization terminated successfully.

Current function value: -3.464792

Iterations: 60

Function evaluations: 74

Gradient evaluations: 74

Markov Switching Model Results

================================================================================

Dep. Variable: GDPC1 No. Observations: 288

Model: MarkovAutoregression Log Likelihood 997.860

Date: Tue, 15 Apr 2025 AIC -1971.720

Time: 08:03:14 BIC -1927.765

Sample: 04-01-1947 HQIC -1954.106

- 10-01-2019

Covariance Type: approx

Regime 0 parameters

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0039 0.003 1.461 0.144 -0.001 0.009

sigma2 0.0002 4.68e-05 3.710 0.000 8.19e-05 0.000

ar.L1 0.1701 0.294 0.578 0.563 -0.406 0.747

ar.L2 0.0333 0.152 0.220 0.826 -0.264 0.330

ar.L3 -0.0172 0.197 -0.088 0.930 -0.403 0.369

Regime 1 parameters

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0089 0.001 9.467 0.000 0.007 0.011

sigma2 2.747e-05 3.59e-06 7.645 0.000 2.04e-05 3.45e-05

ar.L1 0.3493 0.095 3.680 0.000 0.163 0.535

ar.L2 0.3082 0.076 4.041 0.000 0.159 0.458

ar.L3 -0.2095 0.086 -2.438 0.015 -0.378 -0.041

Regime transition parameters

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

p[0->0] 0.8760 0.131 6.674 0.000 0.619 1.133

p[1->0] 0.0464 0.029 1.605 0.108 -0.010 0.103

==============================================================================

Warnings:

[1] Covariance matrix calculated using numerical (complex-step) differentiation.

The main difference in the models is the huge difference in the estimate of the volatility parameters in each regime:

res_gdpgr2.params.loc['sigma2[0]'] / res_gdpgr2.params.loc['sigma2[1]']

np.float64(6.318021262238154)

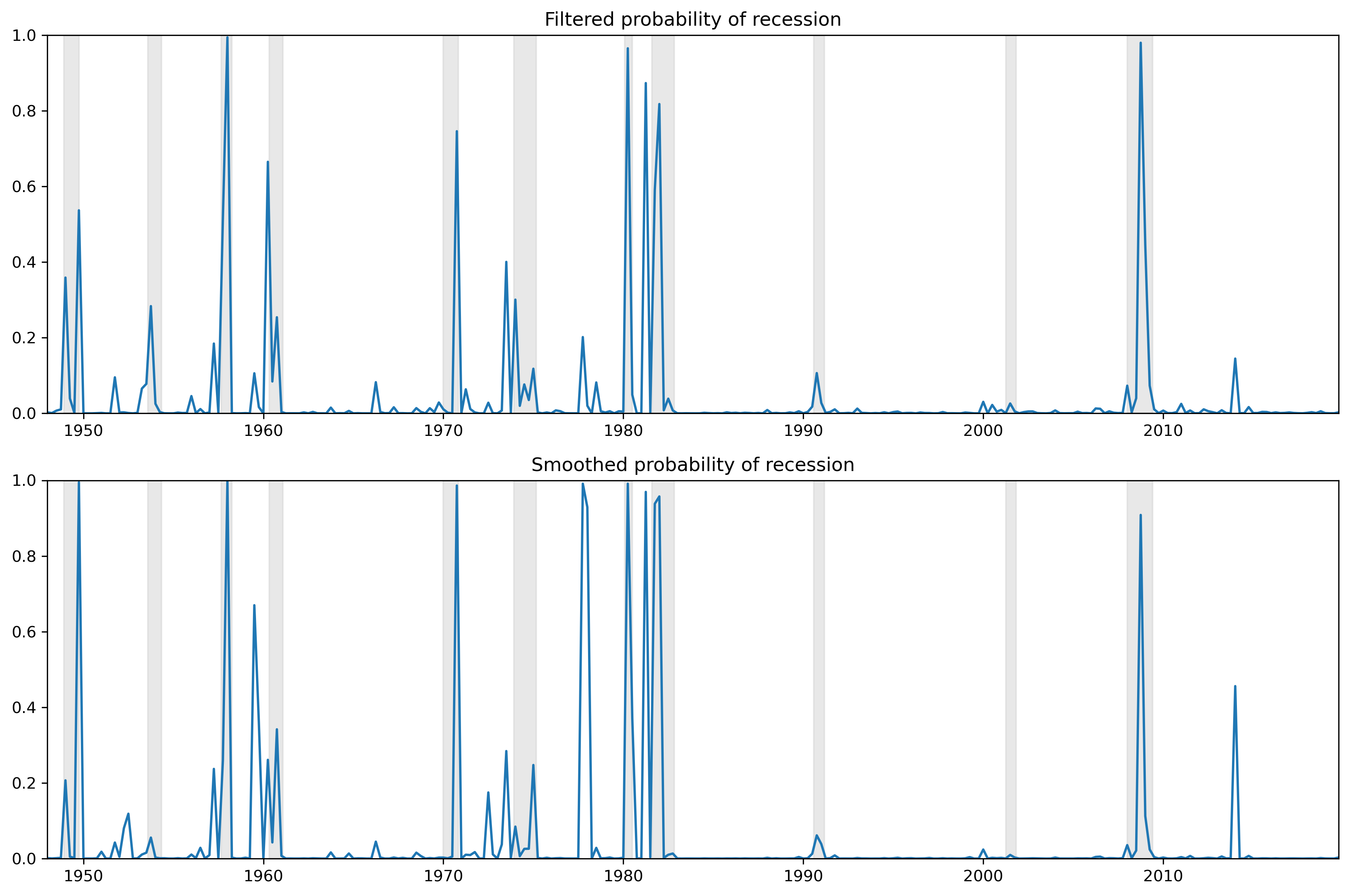

res_gdpgr2.smoothed_marginal_probabilities[0].plot();

import statsmodels.api as sm

from statsmodels.tsa import stattools as st

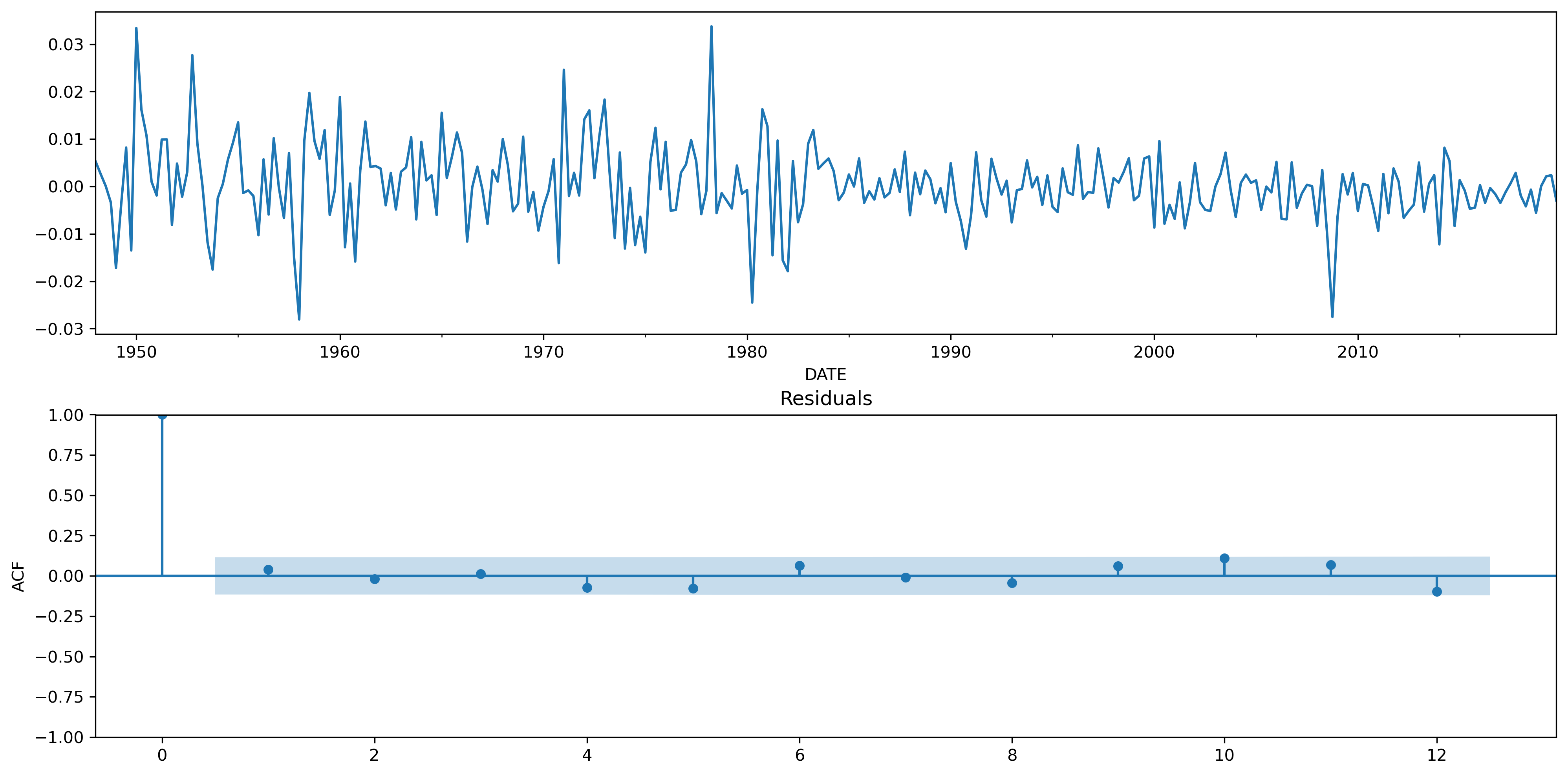

fig, (ax1, ax2) = plt.subplots(2,1, figsize=(16,8))

plt.subplots_adjust(hspace=0.25)

res_gdpgr2.resid.plot(ax=ax1)

fig = sm.graphics.tsa.plot_acf(res_gdpgr2.resid.values, lags=12, ax=ax2)

ax2.set_title('Residuals')

ax2.set_ylabel('ACF')

plt.show()

acf, qstats, pvals = st.acf(res_gdpgr2.resid, nlags=12, qstat=True)

pvals

array([0.49704508, 0.75425769, 0.8932877 , 0.70526199, 0.56530032,

0.52849255, 0.64202275, 0.68052737, 0.65837221, 0.40848839,

0.37669856, 0.26197076])