Time series models#

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import wrds

db = wrds.Connection()

Loading library list...

Done

White noise#

A time series is said to be white noise if its realizations are drawn from an iid (independent and identically distributed) random variable. A special case is Gaussian white noise, where

This assumption has three implications:

\(\E(\varepsilon_t) = \E(\varepsilon_t | \varepsilon_{t-1}, \varepsilon_{t-2}, \ldots) = 0\),

\(\E(\varepsilon_t \varepsilon_{t-j}) = \cov(\varepsilon_{t}, \varepsilon_{t-j}) = 0\),

\(\var(\varepsilon_t) = \var(\varepsilon_t | \varepsilon_{t-1}, \varepsilon_{t-2}, \ldots) = \sigma_{\varepsilon}^2\).

The first and second facts imply the absense of any serial correlation or predictability. The third fact implies that the series is conditionally homoskedastic, or has a constant conditional variance, where “conditional” means that we use what we know about how the time series has behaved up until a point in time.

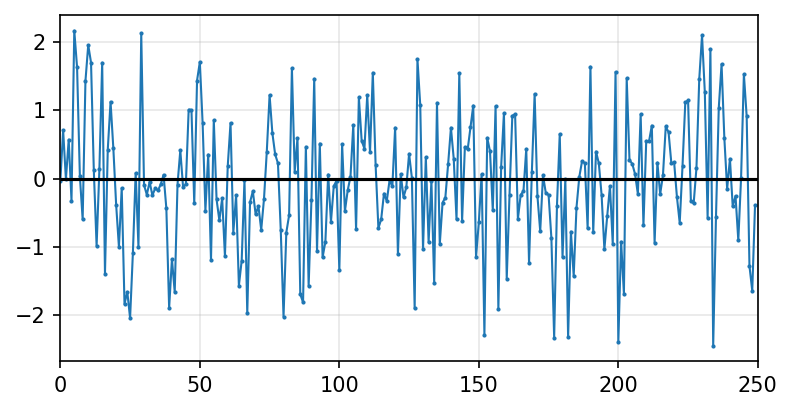

rng = np.random.default_rng(8675309)

T = 250

ε = rng.standard_normal(T)

fig, ax = plt.subplots(figsize=(6,3))

ax.plot(ε, lw=1, marker='.', markersize=2)

ax.set_xlim(0,T)

ax.grid(alpha=0.3)

ax.hlines(0, xmin=0, xmax=T, color='k')

plt.show()

We can construct more complex models of time series by taking linear combinations of white noise:

Type |

Equation |

|---|---|

AR(1) |

\(x_t = \phi x_{t-1} + \varepsilon_t\) |

AR(p) |

\(x_t = \phi_1 x_{t-1} + \phi_2 x_{t-2} + \cdots + \phi_p x_{t-p} +\varepsilon_t\) |

MA(1) |

\(x_t = \varepsilon_t + \theta \varepsilon_{t-1}\) |

MA(q) |

\(x_t = \varepsilon_t + \theta_1 \varepsilon_{t-1} + \theta_2 \varepsilon_{t-2} + \cdots + \theta_q \varepsilon_{t-q}\) |

ARMA(p,q) |

\(x_t = \phi_1 x_{t-1} + \cdots + \phi_p x_{t-p} + \varepsilon_t + \theta_1 \varepsilon_{t-1} + \cdots + \theta_q \varepsilon_{t-q}\) |

Adding a constant to the model will absorb any mean in the underlying process. To see this, suppose that the demeaned value of \(x\) follows an AR(1), so

This is the same thing as

which is simply an AR(1) with an added constant term, \(\phi_0 := (1-\phi)\bar x\). In other words, if we specify a model with a constant term it is equivalent to first subtracting the mean from the series.

Stationarity#

A times series is said to be weakly stationary if

\(\E(r_t) = \mu\); and

\(\cov(r_t,r_{t-k})=\gamma_k\).

That is, the expected return is constant over time, and the covariance between the return at time \(t\) and time \(t-k\) depends only on the horizon \(k\), not on where in the time series we are, \(t\).

Autocorrelation function (ACF)#

We will define the autocovariance of a time series \(\{r_t\}\) with \(k\) lags as

That is, what is the covariance of a series with itself where we compare the value at time \(t\) with the value at some earlier time \(t-k\). Note that it follows immediately that \(\gamma_0 = \var(r_t).\)

Recall that the correlation coefficient between two random variables \(X\) and \(Y\) is defined as

The correlation between \(r_t\) and \(r_{t-k}\) is therefore

Notice that this definition assumes the series is weakly stationary, so \(\var(r_t) = \var(r_{t-k}) = \var(r)\).

\(\rho(k)\) is the autocorrelation function. It gives the autocorrelation for a time series as a function of \(k\).

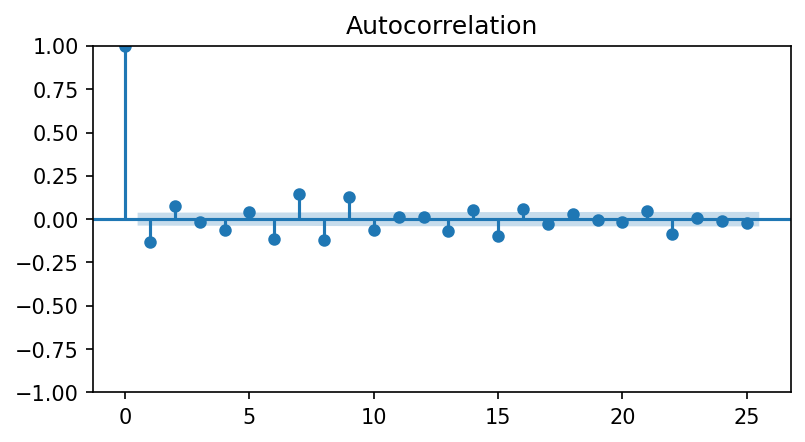

Let’s calculate \(\rho(1)\) for S&P 500 index using the last ten years of daily data. We’ll multiply by 100 to avoid precision problems later.

sp500 = db.get_table('crsp', 'dsp500', date_cols=['caldt'], columns=['caldt', 'spindx']).set_index('caldt')

sp500 = sp500.dropna().squeeze()

rets = sp500.loc['2014':].pct_change().dropna() * 100

rets

caldt

2014-01-03 -0.033297

2014-01-06 -0.251178

2014-01-07 0.608177

2014-01-08 -0.02122

2014-01-09 0.03483

...

2024-12-24 1.104272

2024-12-26 -0.040563

2024-12-27 -1.105574

2024-12-30 -1.070201

2024-12-31 -0.428479

Name: spindx, Length: 2767, dtype: Float64

# calculate the 1-period autocovariance

covmat = np.cov(rets[:-1], rets[1:])

covmat

array([[ 1.19287291, -0.15691324],

[-0.15691324, 1.1929527 ]])

# 1-period autocorrelation

covmat[0,1] / covmat[0,0]

-0.13154229872535833

The ACF is built-in to the statsmodels library, along with a helpful plotting function.

import statsmodels.api as sm

from statsmodels.tsa import stattools as st

st.acf(rets, nlags=10)

array([ 1. , -0.13153323, 0.07357237, -0.01855214, -0.06314426,

0.04068317, -0.11227941, 0.1431176 , -0.12037467, 0.12920954,

-0.06164976])

fig, ax = plt.subplots(figsize=(6,3))

fig = sm.graphics.tsa.plot_acf(rets, lags=25, ax=ax)

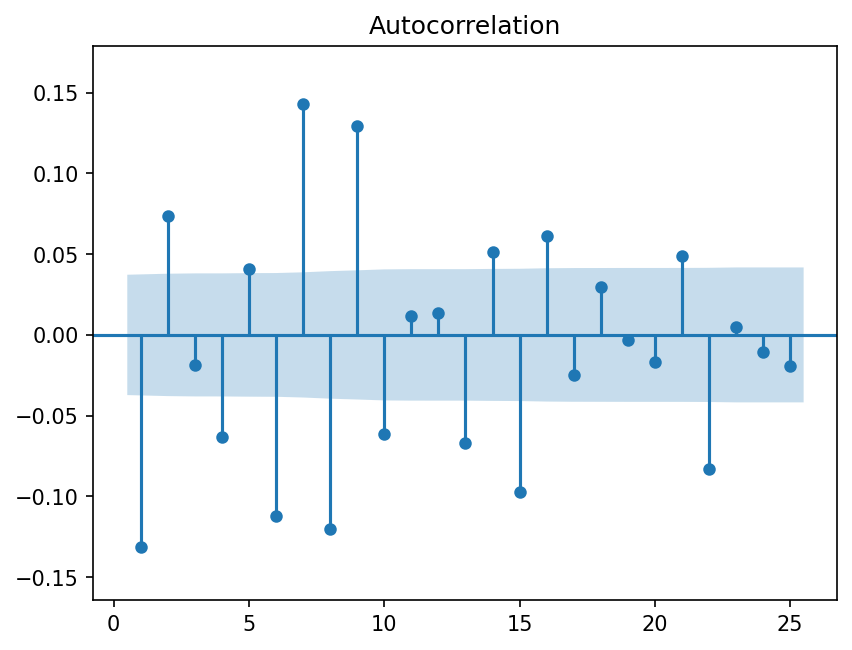

Since \(\rho(1)\) is always equal to one, it is common to plot the autocorrelation without this value.

fig = sm.graphics.tsa.plot_acf(rets, lags=25, zero=False, auto_ylims=True)

Testing for autocorrelation at multiple horizons is done using a portmanteau test such as the Ljung-Box statistic,

where we choose some number \(m\) as the maximum number of lags to consider.

m = 5

acfs = st.acf(rets, nlags=m)

T = len(rets)

k = np.arange(1,len(acfs))

# Q(m) statistic

q = T * (T+2) * (acfs[1:]**2 / (T-k)).sum()

q

79.52483849195411

How do we interpret this value? Is it big? Small?

We need to know what we would expect it to be if there aren’t significant correlations. In other words, under the null hypothesis of no autocorrelation at all \(m\) lags, what is the distribution of the \(Q(m)\) statistic? How surprised should we be at seeing a number like 149?

Ljung and Box (1978) showed that under the null of no autocorrelations, the test statistic has a \(\chi^2\) distribution with \(m\) degrees of freedom.

If \(Q\) is larger than \(\chi^2_{\alpha}\) then we reject the null at the \(\alpha\) significance level. For example, the cutoff for a 5% test is about 11.

from scipy.stats import chi2

chi2.ppf(0.95, df=m)

11.070497693516351

Clearly, the \(Q\) statistic we calculated is far greater than this value, indicating that we can easily reject the null hypothesis.

By specifying qstat=True we get \(Q\)-statistics with corresponding \(p\)-values. (Recall that a \(p\)-value is the probability of observing a statistic of some magnitude under the null hypothesis. In this case, the null hypothesis is that there is no serial correlation. If the test-statistic is larger than the corresponding “critical value” then the probability of getting this result if the null hypothesis is true is small. We take this as evidence against the null.)

acf, qstats, pvals = st.acf(rets, nlags=10, qstat=True)

qstats

array([ 47.92376387, 62.92290611, 63.87698069, 74.93351291,

79.52483849, 114.50855801, 171.36885614, 211.60817794,

257.98778164, 268.55007335])

pvals

array([4.43118117e-12, 2.17002404e-14, 8.72063582e-14, 2.05816403e-15,

1.05499815e-15, 2.31492106e-22, 1.29154929e-33, 2.27821811e-41,

2.05052164e-50, 6.75920631e-52])

AR models#

from statsmodels.tsa.arima_process import ArmaProcess, arma_acf

from statsmodels.tsa.arima.model import ARIMA

Suppose returns, \(r_t\), follow and AR(1) model,

We can calculate conditional mean and variance of \(r_t\) as

and

To find the unconditional mean, begin by taking the expectation of each side of the equation:

Notice that this result requires the stationarity assumption so \(\E(r_t) = \E(r_{t-1}).\) Similarly, the variance is

In the more general case of the AR(p) model, the unconditional mean is

The unconditional variance is more complicated to solve in the general case because there are covariance terms that complicate the math and require a recursive solution procedure.

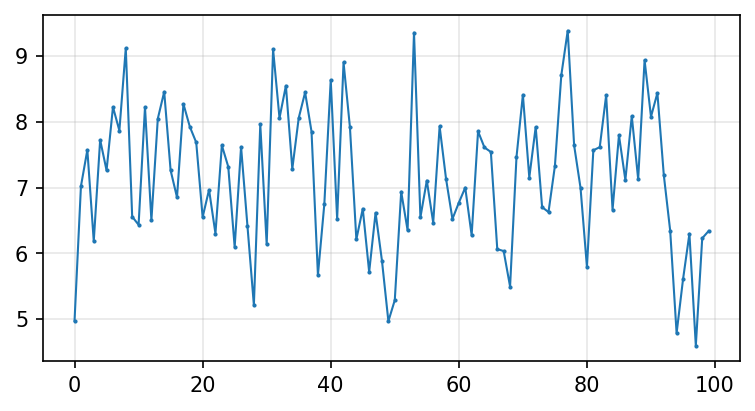

We can simulate an AR(p) process as follows:

def simulate_ar1(φ0, φ1, T=1000):

rng = np.random.default_rng()

# initilize series

r = np.zeros(T+1)

# simulate AR(1) process with forward recursion

ε = rng.standard_normal(T+1)

for t in range(1,T+1):

r[t] = φ0 + φ1*r[t-1] + ε[t]

# return the series without the initial value

return r[1:]

r = simulate_ar1(5, .3)

print('Theoretical mean: {:0.3f}'.format(5/(1-.3)))

print('Sample mean: {:0.3f}'.format(r.mean()))

print('Theoretical variance: {:0.3f}'.format(1/(1-.3**2)))

print('Sample variance: {:0.3f}'.format(r.var()))

Theoretical mean: 7.143

Sample mean: 7.078

Theoretical variance: 1.099

Sample variance: 1.077

# plot the first 100 observations

fig, ax = plt.subplots(figsize=(6,3))

ax.plot(r[:100], lw=1, marker='.', markersize=2)

ax.grid(alpha=0.3)

r = simulate_ar1(0, .8)

fig, ax = plt.subplots(figsize=(6,3))

ax.plot(r[:100], lw=1, marker='.', markersize=2)

ax.grid(alpha=0.3)

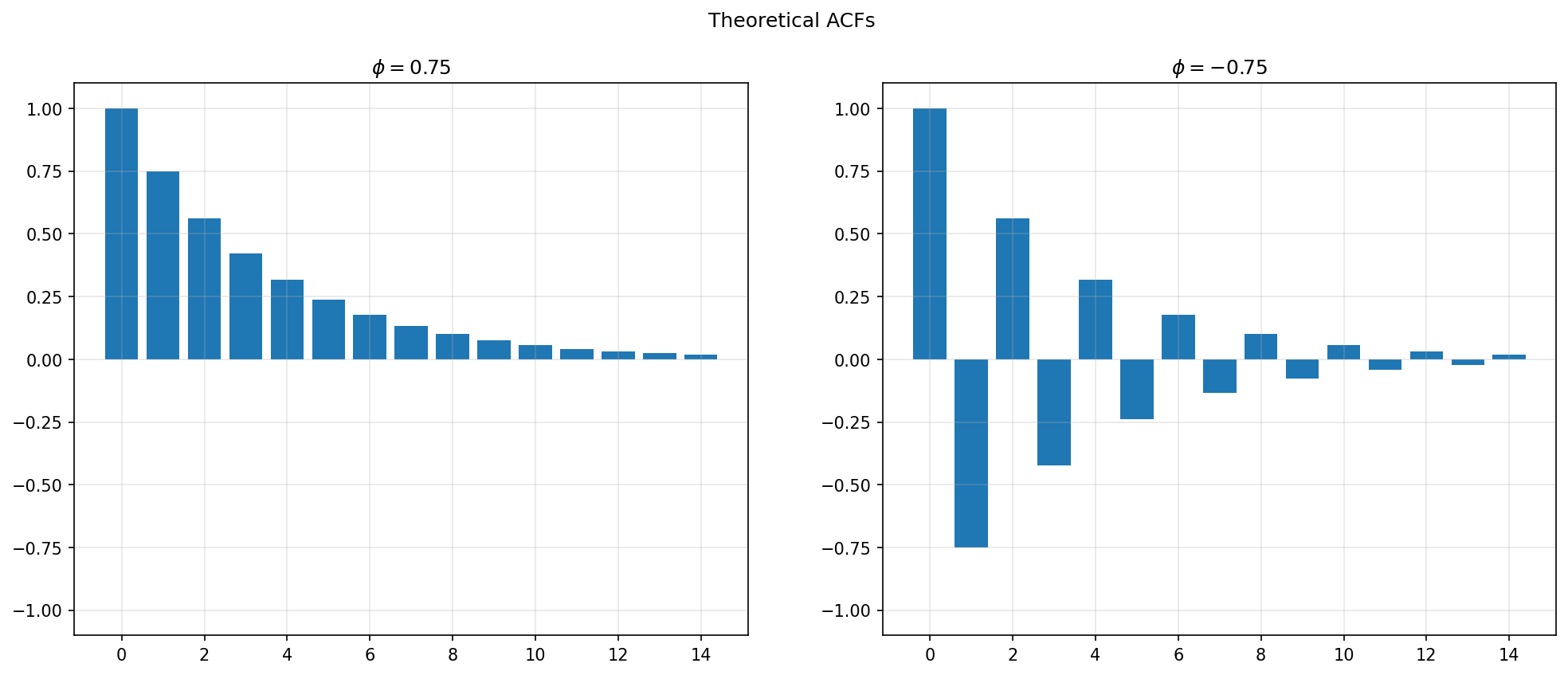

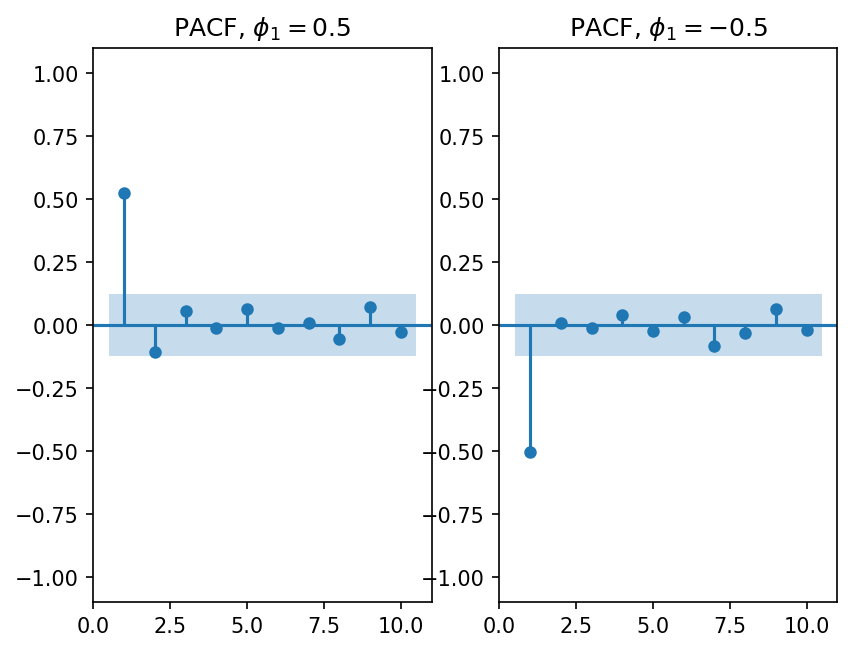

Consider the plot of the ACF for two different AR(1) models: one with \(\phi=0.75\) and the other with \(\phi=-0.75\).

Clearly the autocorrelations for an AR process die out as \(k\) increases. To see why, notice that the model

means that of course

We can then calculate \(\gamma_1\):

and therefore \(\rho(1) = \phi\).

But notice also that, by subsituting the value for \(r_{t-1}\) into the first equation,

This implies that \(\rho(2) = \phi^2\).

But we don’t have to stop there. We could do the same recursion again, which gives

implying that \(\rho(3) = \phi^3\).

Repeating this recursion ad infinitum leads to the general result that

so

So, as we see in the graph above, when \(\phi=0.75\) we’ll find:

\(\rho(1) = 0.75\)

\(\rho(2) = 0.75^2 \approx 0.56\)

\(\rho(3) = 0.75^3 \approx 0.42\)

and so on.

As we take \(k\rightarrow\infty\), the first term disappears because \(\phi<1\). We’ll see below that this means we are left with an MA model where \(q=\infty\). In other words, an AR(1) model is equivalent to an MA(\(\infty\)) model.

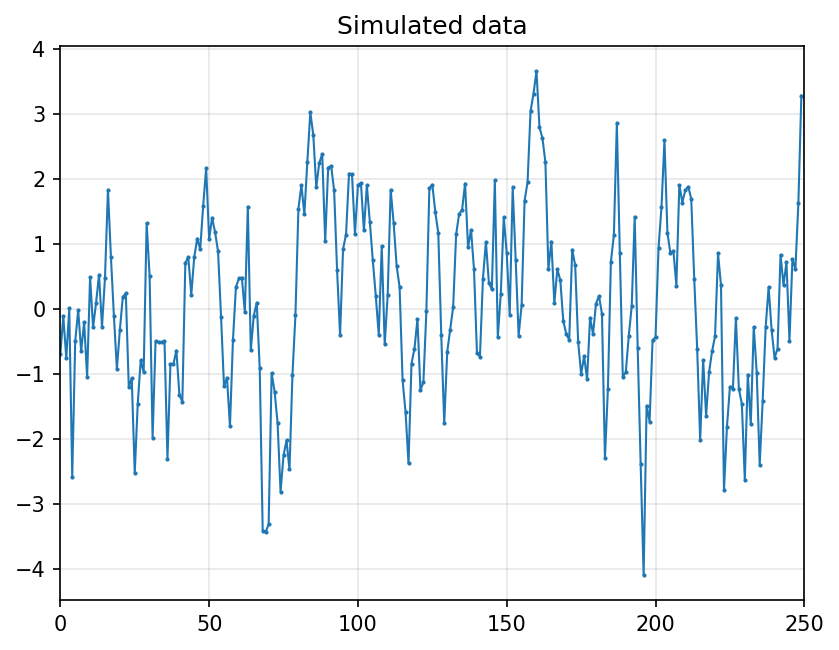

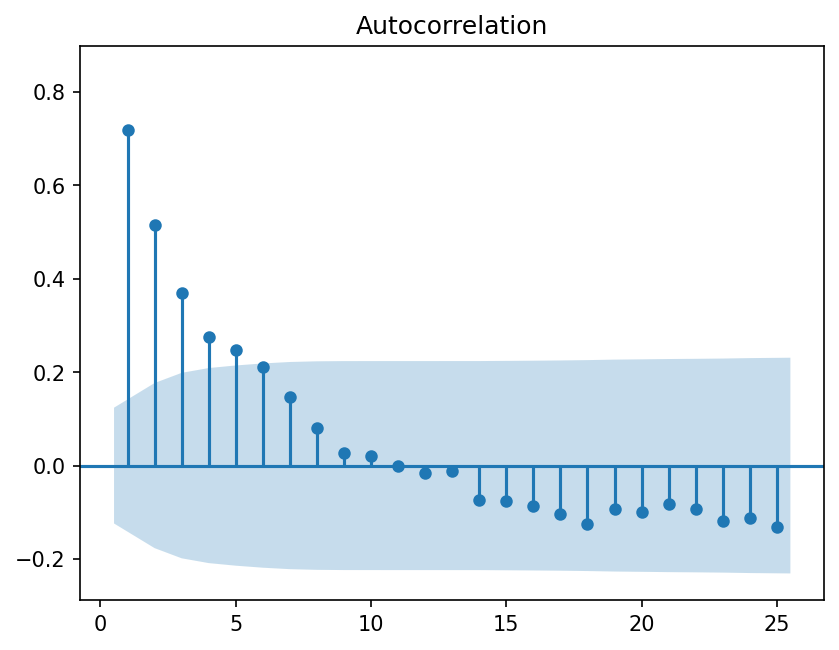

While we can simulate series as we did above, the ArmaProcess function provides a built-in functionality to do this kind of simulation, and also works with other types of time series models.

φ = 0.75

T = 250

y = ArmaProcess([1, -φ]).generate_sample(T)

fig = sm.graphics.tsa.plot_acf(y, lags=25, zero=False, auto_ylims=True)

Estimating AR coefficients#

We can estimate the \(\phi\) parameters using OLS.

res_ols = sm.OLS(y[1:], sm.add_constant(y[:-1])).fit()

print(res_ols.summary())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.528

Model: OLS Adj. R-squared: 0.526

Method: Least Squares F-statistic: 276.3

Date: Mon, 06 Apr 2026 Prob (F-statistic): 3.78e-42

Time: 14:49:40 Log-Likelihood: -344.37

No. Observations: 249 AIC: 692.7

Df Residuals: 247 BIC: 699.8

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0432 0.062 0.702 0.483 -0.078 0.164

x1 0.7337 0.044 16.621 0.000 0.647 0.821

==============================================================================

Omnibus: 6.007 Durbin-Watson: 1.966

Prob(Omnibus): 0.050 Jarque-Bera (JB): 5.846

Skew: -0.372 Prob(JB): 0.0538

Kurtosis: 3.098 Cond. No. 1.41

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

A better way to fit a model like this uses AugtoReg.

from statsmodels.tsa.ar_model import AutoReg, ar_select_order

res = AutoReg(y, lags=1, trend='c').fit()

print(res.summary())

AutoReg Model Results

==============================================================================

Dep. Variable: y No. Observations: 250

Model: AutoReg(1) Log Likelihood -344.371

Method: Conditional MLE S.D. of innovations 0.965

Date: Mon, 06 Apr 2026 AIC 694.742

Time: 14:49:42 BIC 705.294

Sample: 1 HQIC 698.989

250

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0432 0.061 0.705 0.481 -0.077 0.163

y.L1 0.7337 0.044 16.689 0.000 0.648 0.820

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 1.3630 +0.0000j 1.3630 0.0000

-----------------------------------------------------------------------------

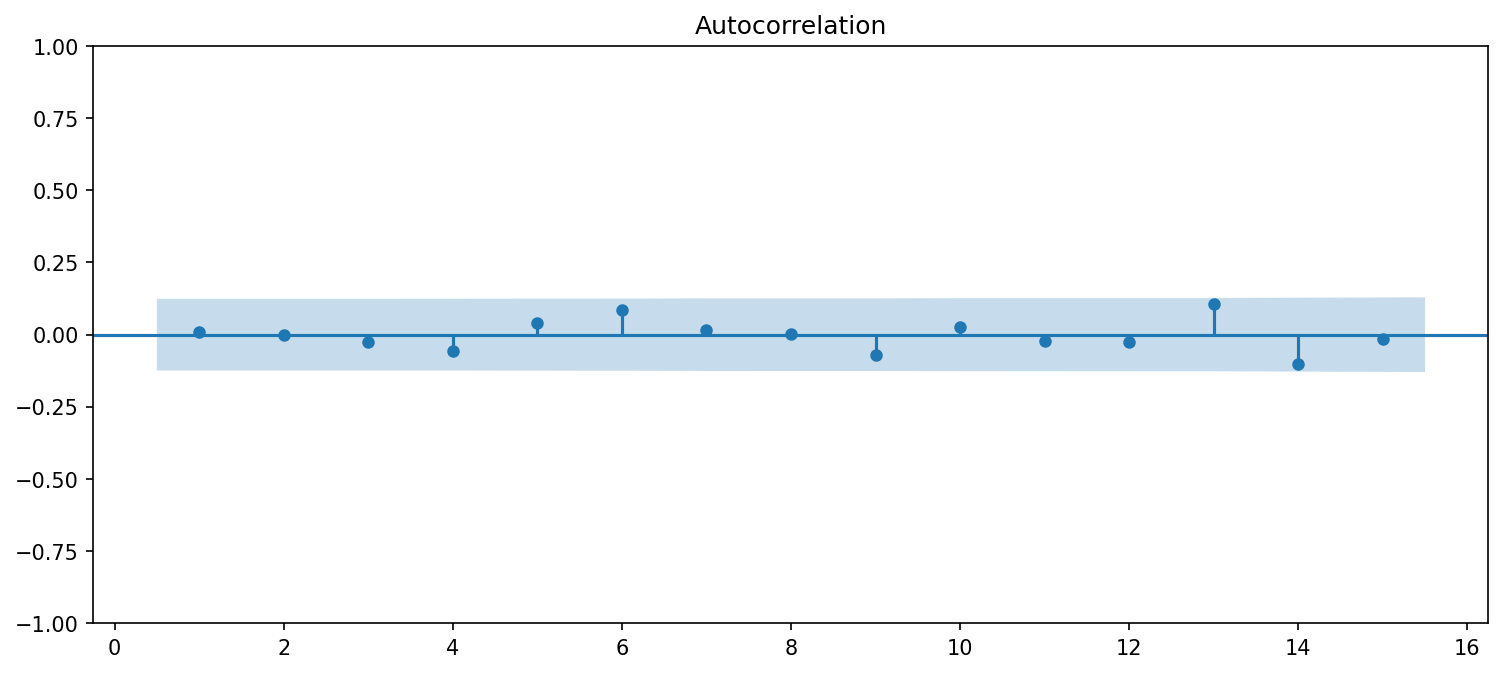

fig, ax = plt.subplots(figsize=(12,5))

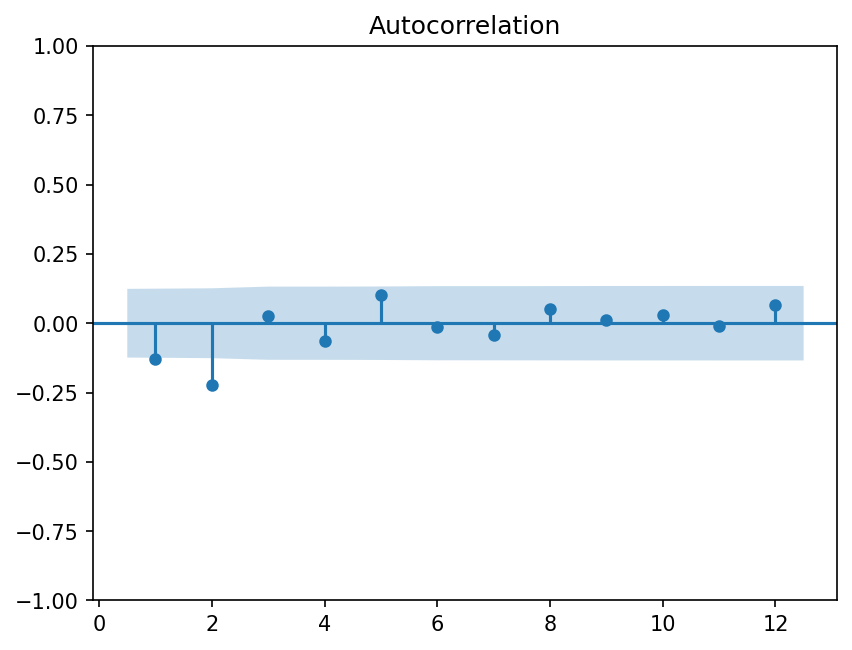

fig = sm.graphics.tsa.plot_acf(res.resid, lags=15, zero=False, ax=ax)

Partial autocorrelation function (PACF)#

With real data we don’t know the correct \(p\) and must estimate it. This can be done using the Partial Autocorrelation Function (PACF).

Consider this sequence of regressions, where we add one more lag to each subsequent regression:

The terms \(\phi_{1,1}, \phi_{2,2}, \phi_{3,3}, \phi_{4,4}, \ldots\) are the relevant coefficients. Each gives the marginal effect of adding one additional lag to the autoregression.

Estimating these regressions using OLS, we get estimates for the \(\phi\), which have these properties:

\(\hat \phi_{p,p}\) converges to \(\phi_p\) as \(T\rightarrow \infty\); and

\(\hat \phi_{k,k}\) converges to zero for all \(k>p\).

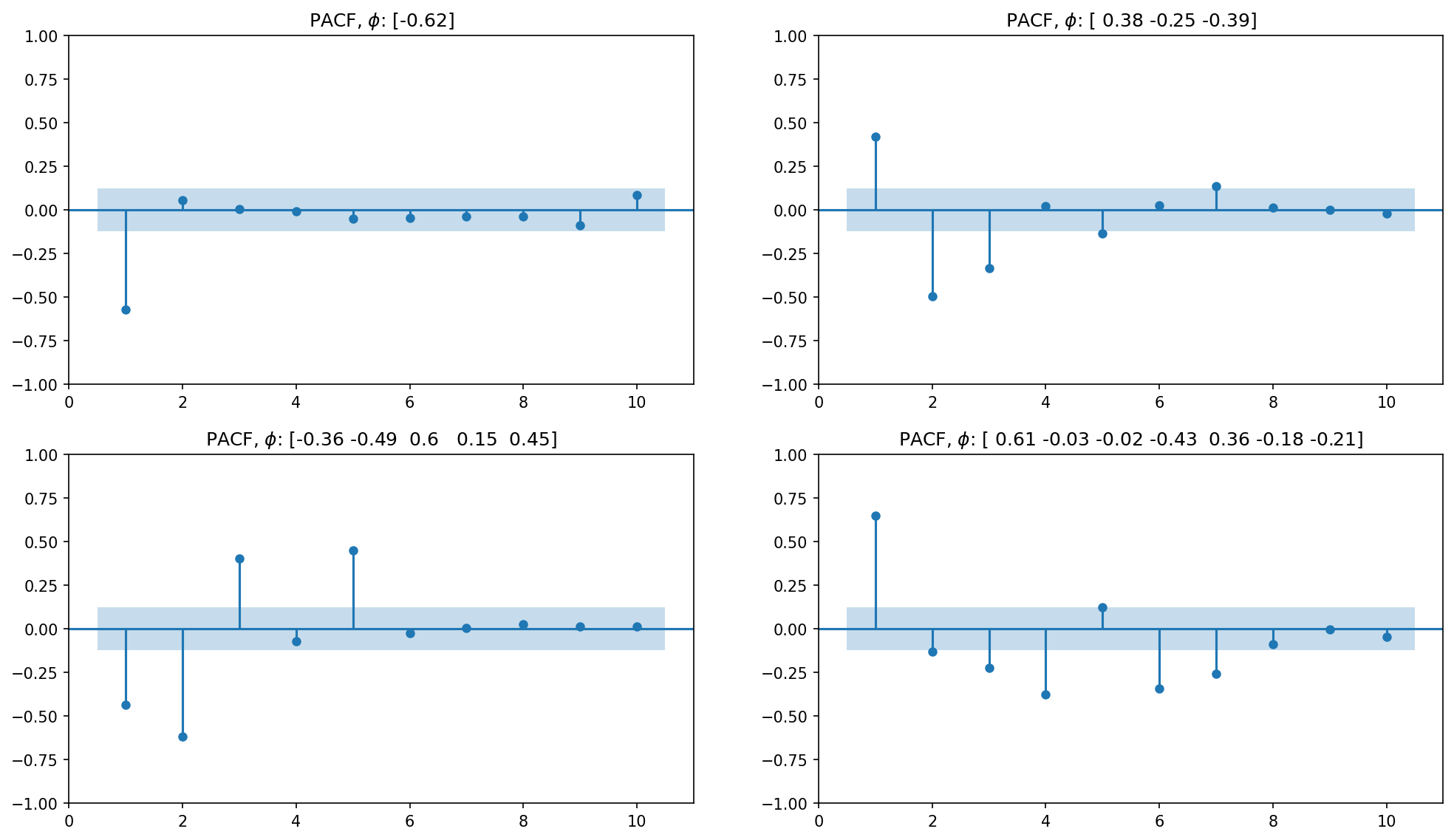

This means that we can determine \(p\) by looking at where the PACF drops off. For example, consider these figures:

fig, axes = plt.subplots(2,2,figsize=(16,9))

lags = [1, 3, 5, 7]

for n,ax in zip(lags, axes.ravel()):

y, params = simulate_ar(n)

fig = sm.graphics.tsa.plot_pacf(y, lags=10, ax=ax, zero=None)

ax.set_title(r'PACF, $\phi$: {}'.format(params))

Information criteria#

We can select among different possible models by evaluating an information criterion. In particular, we can use either the Akaike information criterion (AIC) or the Schwarz-Bayesian information criterion (BIC). Both criteria begin with the log-likelihood function, which measures how likely we are to see the observed data given the model parameters we have estimated.

In the case of the autoregression model, the log-likelihood is given by

where \(T\) is the number of time series observations, \(\ell\) is the number of lags in the model, and \(\hat\sigma_{\varepsilon}^2\) is the variance of the residuals. We can think of \(T-\ell\) as the effictive number of observations, since we lose one observation for each additional lag we include in the model.

Notice that this is smaller when the variance of the residuals, \(\hat\sigma_{\varepsilon}^2\), is greater. That is, the more variance our model leaves unexplained, the lower is the likelihood of the model, and the worse is its fit.

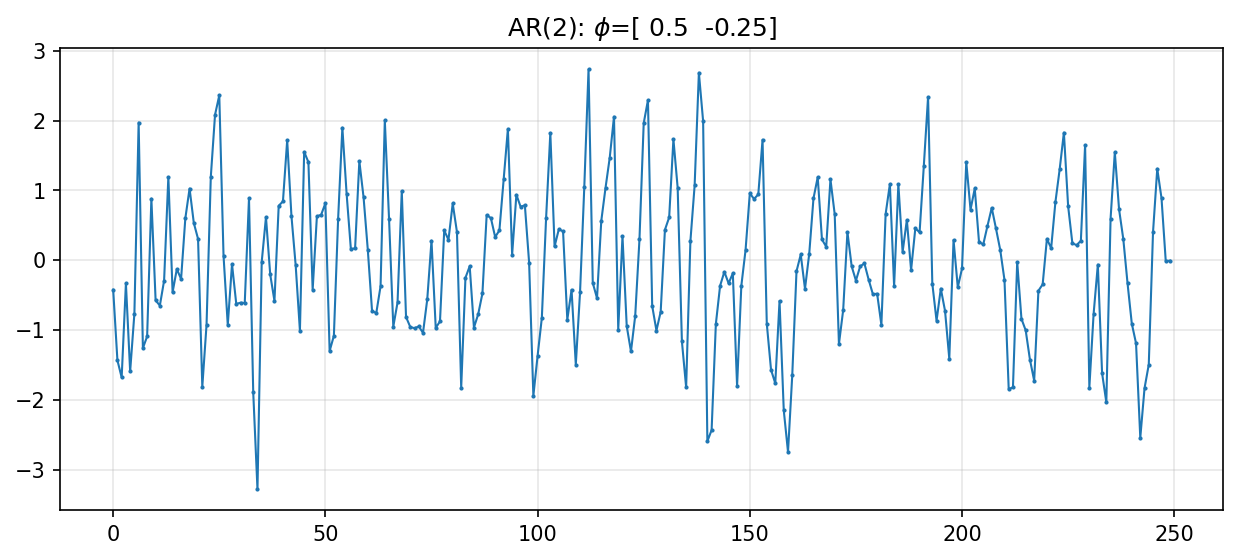

We’ll begin by simulating a new time series to work with.

y, params = simulate_ar(2, coefs=[0.5, -0.25])

fig, ax = plt.subplots(figsize=(10,4))

ax.plot(y, lw=1, marker='.', markersize=2)

ax.grid(alpha=0.3)

ax.set_title(r'AR({}): $\phi$={}'.format(len(params), params))

plt.show()

# fit AR(1) model

res = AutoReg(y, lags=1, trend='c').fit()

print(res.summary())

AutoReg Model Results

==============================================================================

Dep. Variable: y No. Observations: 250

Model: AutoReg(1) Log Likelihood -350.849

Method: Conditional MLE S.D. of innovations 0.990

Date: Mon, 06 Apr 2026 AIC 707.698

Time: 14:57:22 BIC 718.251

Sample: 1 HQIC 711.946

250

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const -0.0145 0.063 -0.231 0.817 -0.138 0.109

y.L1 0.4229 0.057 7.367 0.000 0.310 0.535

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 2.3644 +0.0000j 2.3644 0.0000

-----------------------------------------------------------------------------

res.sigma2

0.9803828131430133

res.llf

-350.8490811049661

The AIC is then defined as

where \(k\) is the degrees of freedom in the model, or the number of lags (plus one if there is a constant term).

We prefer models with a lower AIC. This happens when the likelihood is higher or when we have fewer parameters to estimate.

print('Volatility of residuals: {:.4f}'.format(np.sqrt(res.sigma2)))

print('Number of observations: {}'.format(res.nobs))

print('Degrees of freedom: {}'.format(res.df_model))

print('AIC: {:.3f}'.format(-2*res.llf + 2*(1+res.df_model)))

Volatility of residuals: 0.9901

Number of observations: 249

Degrees of freedom: 2

AIC: 707.698

res.aic

707.6981622099322

The BIC is defined as

-2*res.llf + (res.df_model+1)*np.log(res.nobs)

718.2505208993264

res.bic

718.2505208993264

We can use AIC or BIC to aid in order selection.

modsel = ar_select_order(y, maxlag=6, old_names=False)

# best model appears first

modsel.aic

{(1, 2): 677.3421077542574,

(1, 2, 3): 679.0364587384304,

(1, 2, 3, 4): 680.3446488925334,

(1, 2, 3, 4, 5): 682.3372111722496,

(1, 2, 3, 4, 5, 6): 684.2853092734316,

(1,): 691.5814367086749,

0: 736.108125654351}

modsel.bic

{(1, 2): 687.833612430137,

(1, 2, 3): 693.0251316396032,

(1, 2, 3, 4): 697.8304900189994,

(1,): 698.5757731592613,

(1, 2, 3, 4, 5): 703.3202205240087,

(1, 2, 3, 4, 5, 6): 708.765486850484,

0: 739.6052938796443}

# number of lags selected by default selected criterion (default is BIC)

modsel.ar_lags

[1, 2]

areg = AutoReg(y, lags=2, trend='c', old_names=False).fit()

print(areg.summary())

AutoReg Model Results

==============================================================================

Dep. Variable: y No. Observations: 250

Model: AutoReg(2) Log Likelihood -341.577

Method: Conditional MLE S.D. of innovations 0.959

Date: Mon, 06 Apr 2026 AIC 691.153

Time: 14:58:44 BIC 705.207

Sample: 2 HQIC 696.811

250

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const -0.0137 0.061 -0.224 0.823 -0.133 0.106

y.L1 0.5240 0.061 8.535 0.000 0.404 0.644

y.L2 -0.2426 0.061 -3.953 0.000 -0.363 -0.122

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 1.0797 -1.7191j 2.0301 -0.1607

AR.2 1.0797 +1.7191j 2.0301 0.1607

-----------------------------------------------------------------------------

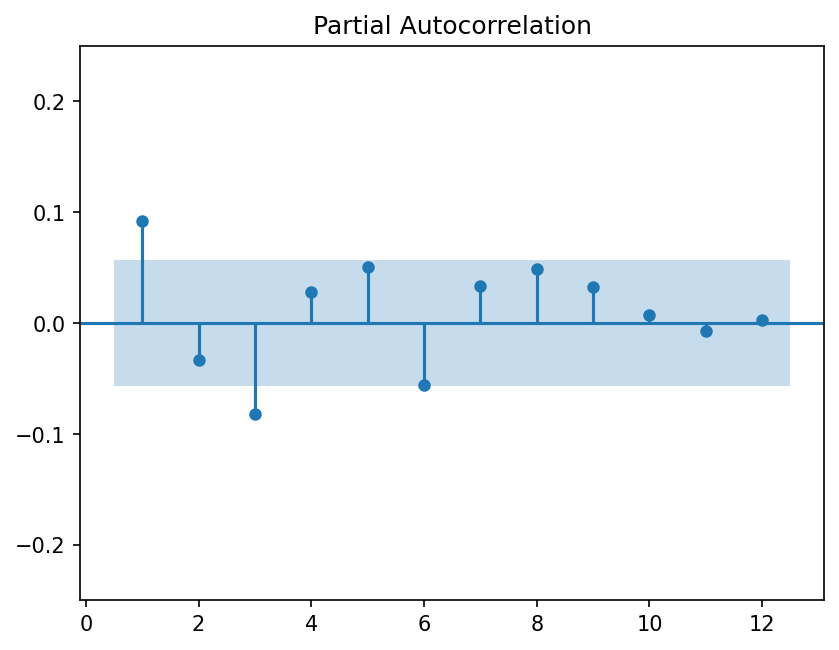

Next, let’s look at the monthly return on the value-weighted market series. The series starts in 1926.

vwret = db.get_table('crsp', 'msi', columns=['date', 'vwretd'], date_cols=['date'])

vwret = vwret.dropna().set_index('date').squeeze()

# move dates to end of month to avoid warnings with model selection

vwret = vwret.asfreq('ME', method='ffill')

vwret

date

1926-01-31 0.000561

1926-02-28 -0.033046

1926-03-31 -0.064002

1926-04-30 0.037029

1926-05-31 0.012095

...

2024-08-31 0.021572

2024-09-30 0.020969

2024-10-31 -0.008298

2024-11-30 0.064855

2024-12-31 -0.031582

Freq: ME, Name: vwretd, Length: 1188, dtype: Float64

fig = sm.graphics.tsa.plot_pacf(vwret, lags=12, zero=False)

fig.axes[0].set_ylim(top=0.25, bottom=-0.25)

(-0.25, 0.25)

modsel = ar_select_order(vwret, maxlag=12, old_names=False)

modsel.bic

{(1,): -3556.6940863383184,

0: -3553.820302624299,

(1, 2, 3): -3551.593418073359,

(1, 2): -3550.9120156201748,

(1, 2, 3, 4): -3545.5448105552946,

(1, 2, 3, 4, 5): -3541.5049850061137,

(1, 2, 3, 4, 5, 6): -3538.088094282661,

(1, 2, 3, 4, 5, 6, 7): -3532.2932200378154,

(1, 2, 3, 4, 5, 6, 7, 8): -3528.0679679759337,

(1, 2, 3, 4, 5, 6, 7, 8, 9): -3522.3229333570007,

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10): -3515.3199157587605,

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11): -3508.3045433948228,

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12): -3501.244838723008}

vwret_ar1 = AutoReg(vwret, lags=1, old_names=False).fit()

print(vwret_ar1.summary())

AutoReg Model Results

==============================================================================

Dep. Variable: vwretd No. Observations: 1188

Model: AutoReg(1) Log Likelihood 1805.381

Method: Conditional MLE S.D. of innovations 0.053

Date: Mon, 06 Apr 2026 AIC -3604.763

Time: 15:01:39 BIC -3589.525

Sample: 02-28-1926 HQIC -3599.020

- 12-31-2024

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0085 0.002 5.445 0.000 0.005 0.012

vwretd.L1 0.0923 0.029 3.191 0.001 0.036 0.149

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 10.8394 +0.0000j 10.8394 0.0000

-----------------------------------------------------------------------------

# testing for serial correlation in residuals

sm.stats.acorr_ljungbox(vwret_ar1.resid, lags=[3,6,9,12], return_df=True)

| lb_stat | lb_pvalue | |

|---|---|---|

| 3 | 9.749551 | 0.020820 |

| 6 | 17.014753 | 0.009229 |

| 9 | 21.864175 | 0.009320 |

| 12 | 22.474247 | 0.032536 |

modsel.aic

{(1, 2, 3, 4, 5, 6, 7, 8): -3573.6968351320606,

(1, 2, 3, 4, 5, 6): -3573.5772131818712,

(1, 2, 3, 4, 5, 6, 7, 8, 9): -3573.0216746415863,

(1, 2, 3, 4, 5, 6, 7): -3572.852213065484,

(1, 2, 3, 4, 5): -3571.924229776865,

(1, 2, 3): -3571.872914587193,

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10): -3571.088531171805,

(1, 2, 3, 4): -3570.8941811975874,

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11): -3569.1430329363257,

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12): -3567.1532023929694,

(1,): -3566.8338345952357,

(1, 2): -3566.1216380055503,

0: -3558.8901767527577}

vwret_ar8 = AutoReg(vwret, lags=8, old_names=False).fit()

print(vwret_ar8.summary())

AutoReg Model Results

==============================================================================

Dep. Variable: vwretd No. Observations: 1188

Model: AutoReg(8) Log Likelihood 1803.623

Method: Conditional MLE S.D. of innovations 0.052

Date: Mon, 06 Apr 2026 AIC -3587.247

Time: 15:02:04 BIC -3536.514

Sample: 09-30-1926 HQIC -3568.120

- 12-31-2024

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0085 0.002 4.994 0.000 0.005 0.012

vwretd.L1 0.0959 0.029 3.297 0.001 0.039 0.153

vwretd.L2 -0.0183 0.029 -0.626 0.531 -0.076 0.039

vwretd.L3 -0.0908 0.029 -3.114 0.002 -0.148 -0.034

vwretd.L4 0.0249 0.029 0.852 0.394 -0.032 0.082

vwretd.L5 0.0613 0.029 2.098 0.036 0.004 0.119

vwretd.L6 -0.0579 0.029 -1.986 0.047 -0.115 -0.001

vwretd.L7 0.0291 0.029 0.996 0.319 -0.028 0.086

vwretd.L8 0.0491 0.029 1.690 0.091 -0.008 0.106

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 1.4255 -0.0000j 1.4255 -0.0000

AR.2 0.9871 -1.0260j 1.4238 -0.1281

AR.3 0.9871 +1.0260j 1.4238 0.1281

AR.4 0.0778 -1.3564j 1.3586 -0.2409

AR.5 0.0778 +1.3564j 1.3586 0.2409

AR.6 -1.1774 -0.8620j 1.4592 -0.3994

AR.7 -1.1774 +0.8620j 1.4592 0.3994

AR.8 -1.7923 -0.0000j 1.7923 -0.5000

-----------------------------------------------------------------------------

Now we can test the residuals for autocorrelation and whether they appear to come from a Normal distribution. In the first test, the null hypothesis is no autocorrelation; in the second it is normally-distributed data.

sm.stats.acorr_ljungbox(vwret_ar8.resid, lags=[3,6,9,12], return_df=True)

| lb_stat | lb_pvalue | |

|---|---|---|

| 3 | 0.009867 | 0.999740 |

| 6 | 0.098975 | 0.999981 |

| 9 | 1.814828 | 0.994069 |

| 12 | 1.967005 | 0.999455 |

vwret_ar8.test_normality()

Jarque-Bera 1993.004718

P-value 0.000000

Skewness 0.098459

Kurtosis 9.363718

dtype: float64

MA(q) models#

As above, the MA(q) model is

Since the \(\varepsilon\) have zero mean, the expected value is given by

The variance is

In order to calculate the autocovariance, we’ll start with the simplest case: \(\gamma_1\) for an MA(1) model. First, notice that

implies that

Therefore,

where the last equality follows from the fact that \(\cov(r_t,r_{t-k}) = 0\) for all \(k\neq 0\).

Next let’s consider a model with one more lag:

In this case, we have

Similarly, we can calculate \(\gamma_2\) as

Notice that any autocovariances of a higher order (i.e. \(\gamma_k\) when \(k>q\)) will be zero.

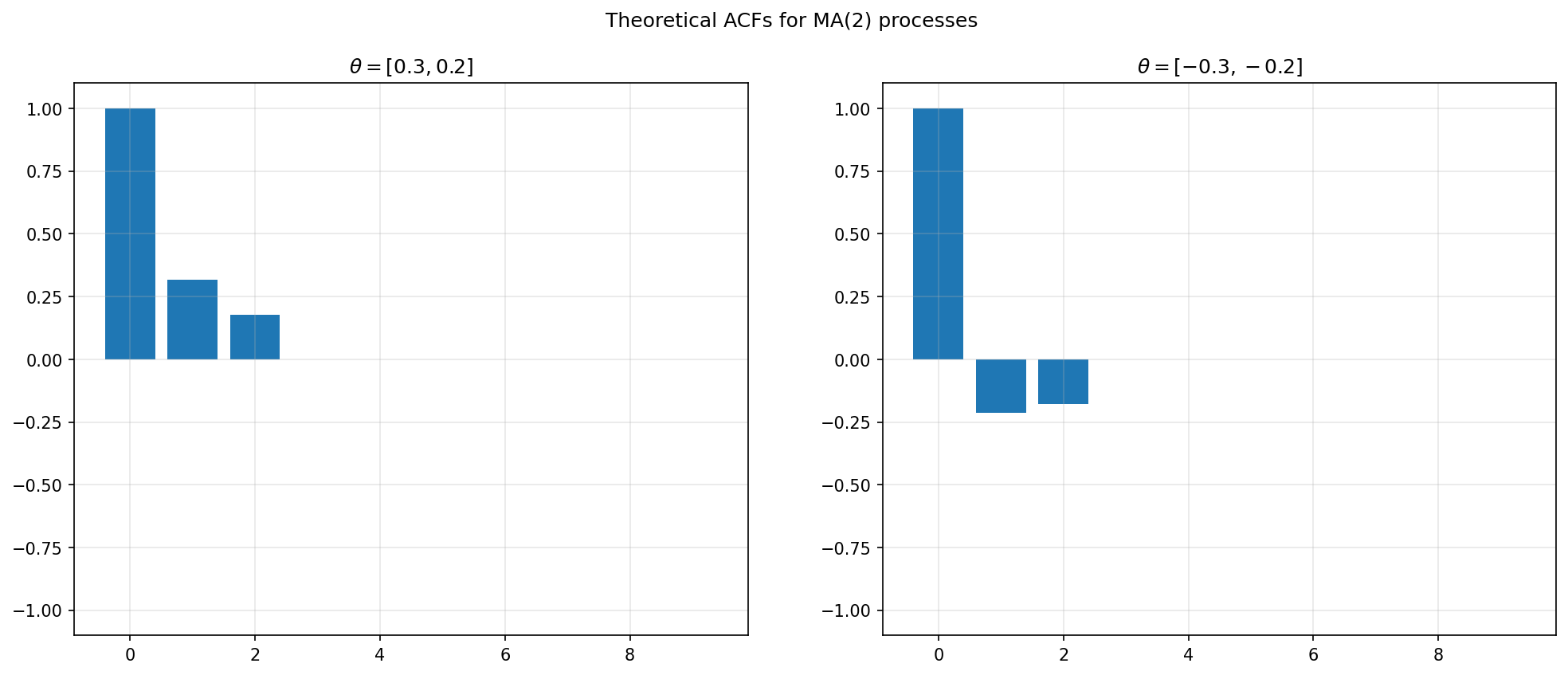

Generalizing the pattern from these examples, we can see that the autocovariance function for a MA(2) model is

For example, suppose \(\theta_1=0.3\) and \(\theta_2=0.2\). And for simplicity, let’s assume \(\mu=0\). Then

The variance is

We also have

and

Therefore,

θ = np.array([0.3, 0.2])

lags = 10

fig, (ax1, ax2) = plt.subplots(1,2,figsize=(16,6))

# MA(2) process

ma_coefs = np.r_[1, θ]

acf = arma_acf([1], ma_coefs, lags=lags)

ax1.bar(np.arange(lags), acf)

ax1.set_title(rf'$\theta={[float(x) for x in θ]}$')

# MA(2)

ma_coefs = np.r_[1, -θ]

acf = arma_acf([1], ma_coefs, lags=lags)

ax2.bar(np.arange(lags), acf)

ax2.set_title(rf'$\theta={[float(x) for x in -θ]}$')

for ax in (ax1, ax2):

ax.set_ylim((-1.1,1.1))

ax.grid(alpha=0.3)

fig.suptitle('Theoretical ACFs for MA(2) processes')

plt.show()

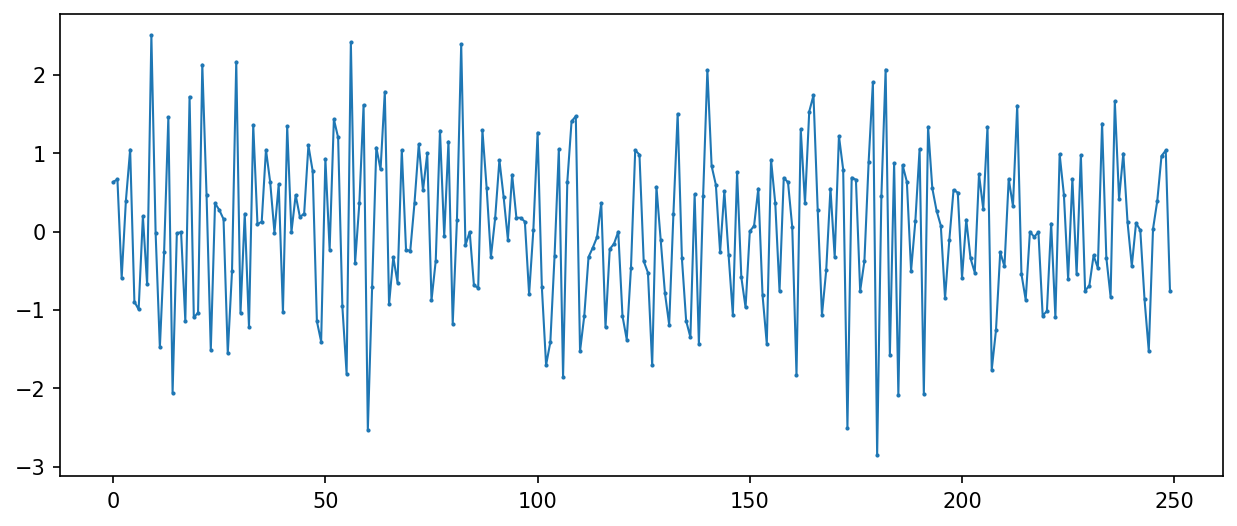

y = ArmaProcess(ma=ma_coefs).generate_sample(250)

fig, ax = plt.subplots(figsize=(10,4))

ax.plot(y, lw=1, marker='.', markersize=2)

plt.show()

fig = sm.graphics.tsa.plot_acf(y, lags=12, zero=None)

vwret_ma9 = ARIMA(vwret, order=(0, 0, 9)).fit()

print(vwret_ma9.summary())

SARIMAX Results

==============================================================================

Dep. Variable: vwretd No. Observations: 1188

Model: ARIMA(0, 0, 9) Log Likelihood 1818.875

Date: Mon, 06 Apr 2026 AIC -3615.750

Time: 15:05:08 BIC -3559.869

Sample: 01-31-1926 HQIC -3594.690

- 12-31-2024

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0093 0.002 4.862 0.000 0.006 0.013

ma.L1 0.0944 0.019 5.097 0.000 0.058 0.131

ma.L2 -0.0087 0.021 -0.413 0.679 -0.050 0.033

ma.L3 -0.0932 0.022 -4.303 0.000 -0.136 -0.051

ma.L4 0.0078 0.023 0.346 0.729 -0.036 0.052

ma.L5 0.0740 0.023 3.281 0.001 0.030 0.118

ma.L6 -0.0277 0.021 -1.292 0.196 -0.070 0.014

ma.L7 0.0203 0.023 0.875 0.382 -0.025 0.066

ma.L8 0.0316 0.017 1.840 0.066 -0.002 0.065

ma.L9 0.0604 0.019 3.135 0.002 0.023 0.098

sigma2 0.0027 6.62e-05 41.370 0.000 0.003 0.003

===================================================================================

Ljung-Box (L1) (Q): 0.00 Jarque-Bera (JB): 1917.60

Prob(Q): 0.99 Prob(JB): 0.00

Heteroskedasticity (H): 0.46 Skew: 0.10

Prob(H) (two-sided): 0.00 Kurtosis: 9.22

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

vwret_ma9 = ARIMA(vwret, order=(0, 0, [1,3,5,9])).fit()

print(vwret_ma9.summary())

SARIMAX Results

=====================================================================================

Dep. Variable: vwretd No. Observations: 1188

Model: ARIMA(0, 0, [1, 3, 5, 9]) Log Likelihood 1817.328

Date: Mon, 06 Apr 2026 AIC -3622.656

Time: 15:05:17 BIC -3592.176

Sample: 01-31-1926 HQIC -3611.169

- 12-31-2024

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0093 0.002 5.200 0.000 0.006 0.013

ma.L1 0.0990 0.018 5.413 0.000 0.063 0.135

ma.L3 -0.0998 0.021 -4.855 0.000 -0.140 -0.060

ma.L5 0.0779 0.022 3.550 0.000 0.035 0.121

ma.L9 0.0545 0.018 3.095 0.002 0.020 0.089

sigma2 0.0027 6.52e-05 42.138 0.000 0.003 0.003

===================================================================================

Ljung-Box (L1) (Q): 0.02 Jarque-Bera (JB): 1836.61

Prob(Q): 0.89 Prob(JB): 0.00

Heteroskedasticity (H): 0.46 Skew: 0.09

Prob(H) (two-sided): 0.00 Kurtosis: 9.09

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

ARMA(p,q) model#

ARMA models combine properties of both AR and MA processes. They are particularly useful in modeling volatility.

vwret_arma = ARIMA(vwret, order=(1, 0, 2)).fit()

print(vwret_arma.summary())

SARIMAX Results

==============================================================================

Dep. Variable: vwretd No. Observations: 1188

Model: ARIMA(1, 0, 2) Log Likelihood 1808.439

Date: Mon, 06 Apr 2026 AIC -3606.878

Time: 15:05:20 BIC -3581.478

Sample: 01-31-1926 HQIC -3597.306

- 12-31-2024

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0093 0.002 5.487 0.000 0.006 0.013

ar.L1 0.5229 0.352 1.485 0.138 -0.167 1.213

ma.L1 -0.4340 0.355 -1.223 0.221 -1.129 0.261

ma.L2 -0.0784 0.027 -2.863 0.004 -0.132 -0.025

sigma2 0.0028 6.04e-05 46.125 0.000 0.003 0.003

===================================================================================

Ljung-Box (L1) (Q): 0.02 Jarque-Bera (JB): 2254.04

Prob(Q): 0.90 Prob(JB): 0.00

Heteroskedasticity (H): 0.43 Skew: 0.09

Prob(H) (two-sided): 0.00 Kurtosis: 9.75

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).