U.S. market returns#

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import wrds

db = wrds.Connection()

Loading library list...

Done

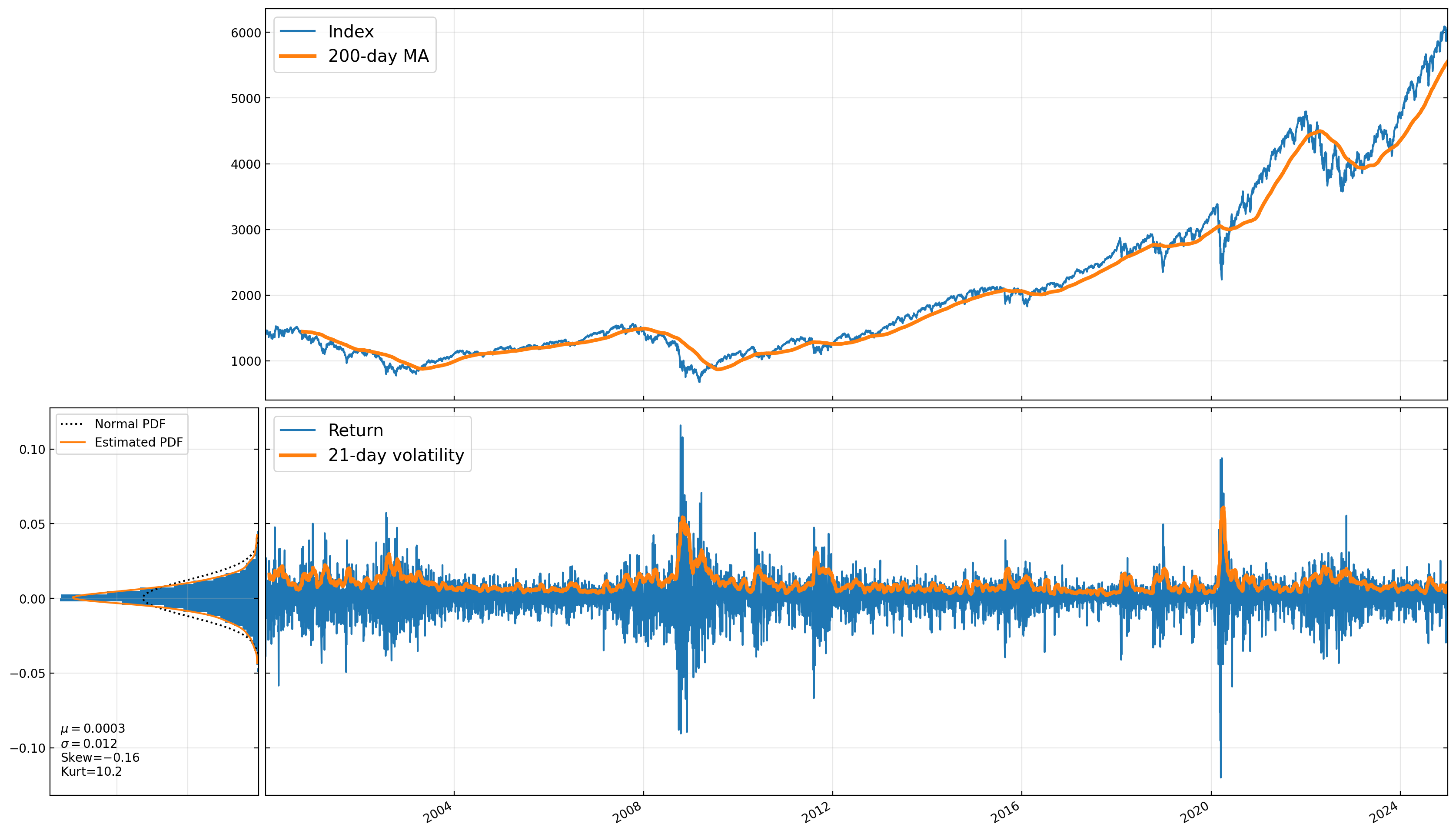

Any data that we observe at regular intervals over time is a time series. An example could be stock prices or returns. For example, let’s look the S&P 500 index since 2000.

sp500 = db.get_table('crsp', 'dsp500', date_cols=['caldt'], columns=['caldt', 'spindx']).set_index('caldt')

sp500 = sp500.dropna().squeeze()

sp500 = sp500.loc['2000-01-01':]

rets = sp500.pct_change().dropna()

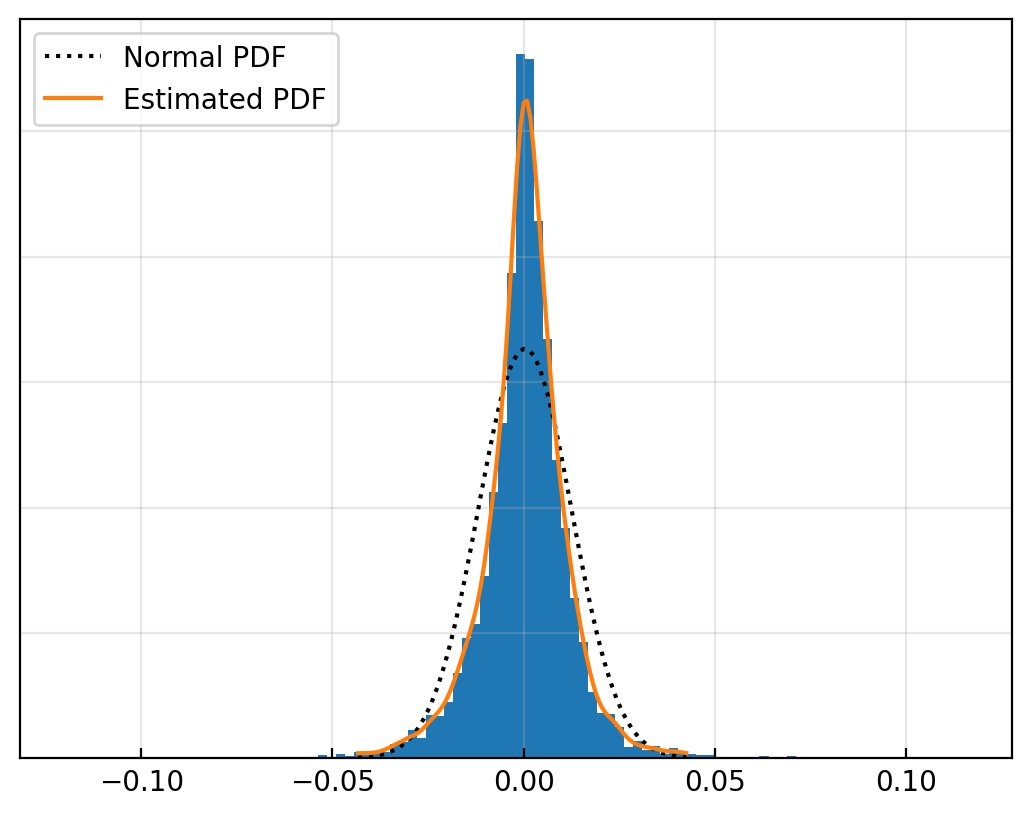

# Plot return histogram

ax = rets.hist(bins=100, density=True)

# Add pdf of normal distribution

from scipy.stats import norm, gaussian_kde

μ, σ = rets.mean(), rets.std()

x = np.linspace(rets.quantile(0.005), rets.quantile(0.995), 100)

pdf = norm.pdf(x, μ, σ)

ax.plot(x, pdf, 'k:', label='Normal PDF')

# Kernel density estimation

kde = gaussian_kde(rets.dropna())

ax.plot(x, kde.pdf(x), label='Estimated PDF')

ax.legend(loc='upper left')

ax.tick_params(direction='in', left=False, labelleft=False)

ax.grid(alpha=0.3)

plt.show()

rets.describe()

count 6288.0

mean 0.000297

std 0.012215

min -0.119841

25% -0.004793

50% 0.000597

75% 0.005928

max 0.1158

Name: spindx, dtype: Float64

rets.skew(), rets.kurt()

(-0.16201426750865283, 10.19031755909176)

There are several statistical tests we can use to test the null hypothesis that data are drawn from a normal distribution. Two that are available in scipy are due to D'agostino and Pearson [1973] and the Shapiro and Wilk [1965]. The former combines information about the skewness and kurtosis of a series; the latter is a more complicated test that uses information about order statistics.

Extra credit

To calculate the D’agostino and Pearson test statistic, we calculate the sample mean and standard deviation of the data,

We then calculate the sample skewness and kurtosis:

Next, we make some statistical adjustments to make the skewness and kurtosis statistics normally distributed:

The normalized statistics are then:

Finally, we calculate the \(K^2\) statistic.

This statistic has a \(\chi^2_{(2)}\) distribution under the null hypothesis that the \(X_i\) are drawn from a Normal distribution.

from scipy.stats import normaltest, shapiro

normaltest(rets)

NormaltestResult(statistic=1141.688127847064, pvalue=1.2177917029121804e-248)

shapiro(rets)

/var/folders/8b/3b5yf0214zvg3prfcqs6wx3c0000gq/T/ipykernel_62578/2132643539.py:1: UserWarning: scipy.stats.shapiro: For N > 5000, computed p-value may not be accurate. Current N is 6288.

shapiro(rets)

ShapiroResult(statistic=0.9019364062429657, pvalue=4.684110917502552e-53)