Factor regressions#

We’ll begin by downloading returns on the Fama-French factors from WRDS.

db = wrds.Connection()

ff = db.get_table('ff', 'factors_monthly', columns=['date', 'mktrf', 'smb', 'hml', 'rf'],

date_cols=['date']).set_index('date')

ff

Loading library list...

Done

| mktrf | smb | hml | rf | |

|---|---|---|---|---|

| date | ||||

| 1926-07-01 | 0.0289 | -0.0255 | -0.0239 | 0.0022 |

| 1926-08-01 | 0.0264 | -0.0114 | 0.0381 | 0.0025 |

| 1926-09-01 | 0.0038 | -0.0136 | 0.0005 | 0.0023 |

| 1926-10-01 | -0.0327 | -0.0014 | 0.0082 | 0.0032 |

| 1926-11-01 | 0.0254 | -0.0011 | -0.0061 | 0.0031 |

| ... | ... | ... | ... | ... |

| 2025-08-01 | 0.0184 | 0.0387 | 0.0442 | 0.0038 |

| 2025-09-01 | 0.0339 | -0.0185 | -0.0105 | 0.0033 |

| 2025-10-01 | 0.0196 | -0.0055 | -0.0309 | 0.0037 |

| 2025-11-01 | -0.0013 | 0.0038 | 0.0376 | 0.003 |

| 2025-12-01 | -0.0036 | -0.0106 | 0.0242 | 0.0034 |

1194 rows × 4 columns

Market, Size, and Value factors#

The data contain monthly returns on four assets:

Mkt-RF is the return on the market portfolio in excess of the riskfree rate. The market portfolio is the CRSP value-weighted portfolio, which includes all stocks traded on U.S. public markets, but uses market-capitalization to weight returns. That is, large stocks have more of an impact on the return of the portfolio than small stocks.

SMB (“small-minus-big”) is the return on a portfolio that is long small stocks and short big stocks.

HML (“high-minus-low”) is the return on a portfolio that is long value stocks and short growth stocks.

RF is the riskfree rate, which is proxied by the 1-month T-Bill.

RMRF, SMB, and HML are known as factor-mimicking portfolios. That is, they are portfolios whose returns are meant to mimick the returns of some underlying economic factor.

The SMB and HML portfolios are constructed from six underlying portfolios that include stocks based on two characteristics:

Size is the market capitalization of the company, equal to number of shares outstanding times the share price;

Book-to-market is the book value of equity divided by market value of equity.

At each point in time, firms with below-median size are called “small” and those above the median are “big”. On the book-to-market dimension, firms are divided into three groups (below 30th percentile, between the 30th and 70th percentile, and above the 70th percentile.) Those with the highest book-to-market are called “value” stocks, while those with the lowest book-to-market are “growth” stocks. Stocks with high book-to-market are typically companies with lots of physical assets but not a lot of growth opportunities, like a utility company. Stocks with low book-to-market are those with a lot of market value relative to their assets, which usually means they have a lot of growth opportunities that make investors willing to pay relatively high prices today to buy shares.

Small |

Big |

|

|---|---|---|

Value |

Small Value |

Big Value |

Neutral |

Small Neutral |

Big Neutral |

Growth |

Small Growth |

Big Growth |

The factors are then long-short portfolios that combine these six building block portfolios differently. The size factor is

and the value factor is

All three factors mimicking are arbitrage, self-financing, or zero net-investment portfolios. While it may be hard to implement for a small investor, theoretically these portfolios could be constructed with no investment — you pay for the long side with funds generated from the short side. With RMRF, for example, we would borrow at the riskfree rate to invest in the market portfolio.

Historical returns#

ff.describe()

| mktrf | smb | hml | rf | |

|---|---|---|---|---|

| count | 1194.0 | 1194.0 | 1194.0 | 1194.0 |

| mean | 0.006915 | 0.001644 | 0.003473 | 0.0027 |

| std | 0.053074 | 0.031521 | 0.035548 | 0.002489 |

| min | -0.2874 | -0.1741 | -0.1383 | -0.0006 |

| 25% | -0.019975 | -0.016275 | -0.01435 | 0.0003 |

| 50% | 0.0108 | 0.0006 | 0.0014 | 0.0023 |

| 75% | 0.036575 | 0.01725 | 0.0176 | 0.0042 |

| max | 0.3881 | 0.3596 | 0.3552 | 0.0135 |

Given monthly returns, the annual return can be approximated as \(12 \times R_t\), where \(R_t\) is the return in month \(t\).

12 * ff.mean()

mktrf 0.08298

smb 0.019729

hml 0.041677

rf 0.032404

dtype: Float64

The variance of the annual return is

so the volatility is

np.sqrt(12) * ff.std()

mktrf 0.183855

smb 0.109193

hml 0.123142

rf 0.008622

dtype: Float64

So on an annualized basis over the last 100 years, the market factor has earned a return of about 8% with a volatility of a little less than 0.2.

The Sharpe ratio is simply the average portfolio return divided by its volatility:

ff.mean() / ff.std()

mktrf 0.130289

smb 0.052157

hml 0.097702

rf 1.084899

dtype: Float64

On an annualized basis, this means we multiply by \(\sqrt{12}\).

np.sqrt(12) * ff.mean() / ff.std()

mktrf 0.451334

smb 0.180677

hml 0.338449

rf 3.7582

dtype: Float64

The one-factor model: CAPM#

The Capital Asset Pricing Model (CAPM) says that an asset’s expected return depends on its beta, denoted \(\beta\). That is,

where \(R^e_i := R_i - R_f\) is the excess return on asset \(i\) and \(R_M\) is the return on the “market portfolio.”

The CAPM is a one-factor model, where the market portfolio is the single factor — the fundamental source of risk in the economy. A factor model of returns says that the returns on an asset come from:

How much return we get from being exposed to any risk factor. In the CAPM, this is \(\E(R_M^e)\), the expected excess return from holding the market.

How much exposure to a factor we get from holding a particular asset. This is the asset’s beta, \(\beta_i = \frac{\cov(R^e_i, R^e_M)}{\var(R^e_M)}.\) It is also called the factor loading. If a stock has high factor loadings, it gives high exposure to the underlying source of risk and is therefore riskier than a stock that has a low factor loading. So high-beta stocks are riskier than low-beta stocks. This is why we say beta is a measure of an asset’s risk.

We saw above that historically the market portfolio has earned an excess return of about 8% per year. If an investor just holds the market portfolio, this is the return they earn for bearing market risk. An investor can earn a higher return by buying a stock with \(\beta_i>1\), allowing them to load up on more of the risk factor. If the investor wants to own a stocks with less risk, she buys a stock with \(\beta_i<1\) (and therefore earn a return below that of the market.

What is risk?#

The CAPM says that a high-beta stock should earn a higher return than a low beta stock. As long as arbitrage opportunities are not common in financial markets, we can only earn higher returns by taking on more risk. Therefore, the higher returns from high betas must be due to higher risk. But why is beta a measure of risk?

It is easiest to understand this if we step back and define what we mean by risk. Economically, a risky asset is one that pays off when times are “good.” This might strange, but stop and think: if you buy an insurance contract against something bad happening, are you increasing your risk or decreasing it? You should agree that insurance reduces risk. Home insurance pays you when your house burns down. It pays off in bad times. (Insurance also has a negative expected return. It has regular negative cash flows, and with a very small probability has a large positive cash flow.)

In economic models, times are “good” when people have low marginal utility. Their needs are being met. They have food to eat, and so having more food won’t increase their utility much. Times are “bad” when they have high marginal utility; their utility would increase a lot if they were able to consume more.

So a low-risk asset should be one that pays off when times are bad. It will allow you to buy more food precisely at the time that you are hungry, just like the insurance contract allows you to build a house when your house burns down. A high-risk asset pays off in good times, when you already have what you need and another dollar isn’t going to have much of an effect on your utility.

In the CAPM, the measure of whether times are good or bad is the market portfolio. This obviously ignores all kinds of important economic information about the welfare of people in an economy, but it is the measure that CAPM uses. (There are other asset pricing models that use other proxies to measure marginal utility.)

Assets with high betas must earn higher expected returns in order to incentivise investors to own these assets. People who are risk averse are willing to hold risky assets, but must be compensated for doing so.

Key fact

In the CAPM model, the measure of an asset’s risk is its beta. The bigger its beta, the more the asset loads on the single risk factor in the economy, and the higher its expected returns must be.

Estimating one-factor regressions#

We can estimate an asset’s \(\beta\) by running a time series regression,

The prediction of the CAPM in this context is that the \(\alpha_i\) should be zero.

# get daily Fama-French factors

ff = db.get_table('ff', 'factors_daily',

columns=['date', 'mktrf', 'smb', 'hml', 'rf'],

date_cols=['date']).set_index('date')

ff = ff['2015':]

# Get a list of stocks on 12/31/2015

crsp = db.raw_sql("""

select dlycaldt, ticker, permno, dlycap

from crsp.dsf_v2

where dlycaldt = '2015-12-31'

and sharetype = 'NS'

and securitytype = 'EQTY'

and securitysubtype = 'COM'

and usincflg = 'Y'

and issuertype = 'CORP'

and dlycap > 0

""")

# Assign each observation to a size decile

crsp['decile'] = pd.qcut(crsp['dlycap'], 10, labels=False) + 1

crsp

| dlycaldt | ticker | permno | dlycap | decile | |

|---|---|---|---|---|---|

| 0 | 2015-12-31 | EGAS | 10001 | 78262.25 | 2 |

| 1 | 2015-12-31 | AEPI | 10025 | 393696.45 | 5 |

| 2 | 2015-12-31 | JJSF | 10026 | 2179045.59 | 8 |

| 3 | 2015-12-31 | DGSE | 10028 | 4057.68 | 1 |

| 4 | 2015-12-31 | PLXS | 10032 | 1161997.92 | 7 |

| ... | ... | ... | ... | ... | ... |

| 3747 | 2015-12-31 | BSFT | 93428 | 1028268.8 | 6 |

| 3748 | 2015-12-31 | CBOE | 93429 | 5327576.1 | 9 |

| 3749 | 2015-12-31 | VLTC | 93433 | 44975.0 | 2 |

| 3750 | 2015-12-31 | SANW | 93434 | 61920.06 | 2 |

| 3751 | 2015-12-31 | TSLA | 93436 | 31543314.25 | 10 |

3752 rows × 5 columns

# Sample 100 records from each decile

crsp_smpl = crsp.groupby('decile').apply(lambda x: x.sample(100, random_state=42)).reset_index(drop=True)

crsp_smpl

| dlycaldt | ticker | permno | dlycap | decile | |

|---|---|---|---|---|---|

| 0 | 2015-12-31 | CKX | 89948 | 19303.48 | 1 |

| 1 | 2015-12-31 | MHH | 92797 | 31820.43 | 1 |

| 2 | 2015-12-31 | ONVI | 87797 | 26505.0 | 1 |

| 3 | 2015-12-31 | URRE | 75672 | 28218.32 | 1 |

| 4 | 2015-12-31 | WGA | 63829 | 5717.32 | 1 |

| ... | ... | ... | ... | ... | ... |

| 995 | 2015-12-31 | AGR | 15859 | 9685824.0 | 10 |

| 996 | 2015-12-31 | HPQ | 27828 | 21215480.32 | 10 |

| 997 | 2015-12-31 | COF | 81055 | 38403008.1 | 10 |

| 998 | 2015-12-31 | CMG | 91068 | 14965561.8 | 10 |

| 999 | 2015-12-31 | GILD | 77274 | 143892180.0 | 10 |

1000 rows × 5 columns

# Average market cap by decile; note that cap is in thousands

crsp_smpl.groupby('decile')['dlycap'].mean()

decile

1 19496.3003

2 61685.4049

3 123253.9379

4 243560.0629

5 432396.5162

6 754680.4412

7 1405437.5624

8 2599697.0889

9 5875866.3458

10 49096214.9178

Name: dlycap, dtype: Float64

Next, we’ll download daily returns for every stock in our sample over the next ten years.

sql = """

SELECT permno, ticker, dlycaldt, dlyret

FROM crsp.dsf_v2

WHERE permno IN %(permnos)s

AND dlycaldt >= '2016-01-01'

"""

params = {'permnos': tuple(crsp_smpl['permno'].to_list())}

rets = db.raw_sql(sql, params=params, date_cols=['dlycaldt'])

rets = rets.pivot(index='dlycaldt', columns='permno', values='dlyret').sort_index(axis=1)

rets

| permno | 10001 | 10025 | 10026 | 10028 | 10032 | 10051 | 10104 | 10145 | 10158 | 10180 | ... | 93132 | 93177 | 93185 | 93264 | 93266 | 93272 | 93289 | 93312 | 93339 | 93399 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| dlycaldt | |||||||||||||||||||||

| 2016-01-04 | 0.009396 | -0.051329 | -0.030685 | -0.054546 | -0.020046 | -0.047416 | -0.017246 | -0.009655 | -0.0384 | 0.021174 | ... | -0.030157 | -0.0286 | -0.018683 | -0.044866 | -0.065268 | -0.029225 | -0.03666 | -0.027098 | 0.020661 | 0.019324 |

| 2016-01-05 | -0.013298 | 0.016532 | -0.005836 | 0.089744 | 0.0 | -0.011487 | -0.003077 | 0.00819 | 0.014975 | 0.009186 | ... | -0.012901 | -0.001319 | 0.010216 | 0.028907 | -0.012469 | -0.039267 | -0.049331 | 0.000903 | 0.072875 | -0.009479 |

| 2016-01-06 | 0.014825 | 0.041532 | 0.002135 | -0.073529 | -0.02104 | -0.005165 | 0.005051 | -0.011314 | -0.018033 | 0.001821 | ... | -0.011394 | -0.012655 | 0.005286 | -0.028095 | -0.046717 | -0.009537 | 0.156412 | -0.025421 | -0.049057 | -0.023923 |

| 2016-01-07 | 0.014608 | -0.038586 | -0.01642 | 0.031746 | -0.023881 | -0.022713 | -0.021776 | -0.029441 | -0.046745 | -0.012461 | ... | -0.011186 | -0.035211 | -0.000229 | -0.04336 | -0.022517 | -0.045392 | -0.041667 | -0.038586 | -0.079365 | 0.0 |

| 2016-01-08 | 0.019634 | 0.004295 | -0.002075 | -0.015385 | -0.024159 | -0.041833 | -0.01113 | -0.008062 | -0.02627 | -0.014984 | ... | -0.019198 | 0.001095 | 0.010748 | 0.01983 | -0.02168 | 0.089337 | 0.000669 | -0.012201 | 0.030172 | 0.014706 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 2025-12-24 | <NA> | <NA> | 0.013073 | 0.021243 | 0.001366 | <NA> | 0.011007 | 0.007315 | 0.00033 | <NA> | ... | 0.006447 | 0.005426 | <NA> | 0.015576 | 0.010345 | -0.014613 | -0.008479 | -0.000898 | <NA> | <NA> |

| 2025-12-26 | <NA> | <NA> | -0.008934 | -0.03698 | 0.001429 | <NA> | 0.002532 | 0.002234 | -0.005274 | <NA> | ... | 0.004681 | -0.014114 | <NA> | -0.018405 | -0.015017 | -0.006408 | 0.010832 | 0.00674 | <NA> | <NA> |

| 2025-12-29 | <NA> | <NA> | 0.00868 | 0.0248 | -0.018999 | <NA> | -0.013183 | -0.001419 | -0.003645 | <NA> | ... | -0.009073 | -0.023158 | <NA> | 0.003125 | 0.0 | -0.015478 | -0.00846 | -0.002678 | <NA> | <NA> |

| 2025-12-30 | <NA> | <NA> | -0.009378 | -0.021858 | -0.011303 | <NA> | 0.009366 | -0.003704 | -0.021949 | <NA> | ... | -0.00631 | -0.001724 | <NA> | 0.037383 | -0.003465 | -0.008235 | 0.006826 | -0.009846 | <NA> | <NA> |

| 2025-12-31 | <NA> | <NA> | 0.00646 | 0.067837 | -0.017248 | <NA> | -0.011663 | -0.006468 | -0.00408 | <NA> | ... | -0.011207 | -0.0557 | <NA> | 0.012012 | -0.000695 | -0.001132 | -0.015254 | -0.012203 | <NA> | <NA> |

2514 rows × 1000 columns

To start, we’ll focus on the returns of just one stock — Oracle (permno 10104). We’ll merge those with the factor returns and then set up a regression.

reg = ff.merge(rets[10104], left_index=True, right_index=True)

reg['exret'] = reg[10104] - reg['rf']

# regression doesn't work NaNs

reg = reg.dropna()

# # pandas recently added a data type that doesn't play well with statsmodels so we'll convert to float

reg = reg.apply(lambda x: x.astype(float))

reg

| mktrf | smb | hml | rf | 10104 | exret | |

|---|---|---|---|---|---|---|

| 2016-01-04 | -0.0159 | -0.0087 | 0.0052 | 0.0000 | -0.017246 | -0.017246 |

| 2016-01-05 | 0.0013 | -0.0018 | 0.0000 | 0.0000 | -0.003077 | -0.003077 |

| 2016-01-06 | -0.0134 | -0.0013 | 0.0001 | 0.0000 | 0.005051 | 0.005051 |

| 2016-01-07 | -0.0244 | -0.0029 | 0.0008 | 0.0000 | -0.021776 | -0.021776 |

| 2016-01-08 | -0.0111 | -0.0049 | -0.0003 | 0.0000 | -0.011130 | -0.011130 |

| ... | ... | ... | ... | ... | ... | ... |

| 2025-12-24 | 0.0029 | 0.0003 | 0.0001 | 0.0002 | 0.011007 | 0.010807 |

| 2025-12-26 | -0.0006 | -0.0032 | 0.0009 | 0.0002 | 0.002532 | 0.002332 |

| 2025-12-29 | -0.0041 | -0.0018 | 0.0007 | 0.0002 | -0.013183 | -0.013383 |

| 2025-12-30 | -0.0020 | -0.0060 | 0.0028 | 0.0002 | 0.009366 | 0.009166 |

| 2025-12-31 | -0.0076 | 0.0007 | -0.0009 | 0.0002 | -0.011663 | -0.011863 |

2514 rows × 6 columns

import statsmodels.api as sm

reg_model = sm.OLS(reg['exret'], sm.add_constant(reg['mktrf']))

reg_rslt = reg_model.fit()

print(reg_rslt.summary())

OLS Regression Results

==============================================================================

Dep. Variable: exret R-squared: 0.309

Model: OLS Adj. R-squared: 0.308

Method: Least Squares F-statistic: 1122.

Date: Sun, 15 Feb 2026 Prob (F-statistic): 1.06e-203

Time: 19:54:33 Log-Likelihood: 6636.6

No. Observations: 2514 AIC: -1.327e+04

Df Residuals: 2512 BIC: -1.326e+04

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0003 0.000 0.945 0.345 -0.000 0.001

mktrf 0.9838 0.029 33.498 0.000 0.926 1.041

==============================================================================

Omnibus: 2360.470 Durbin-Watson: 2.032

Prob(Omnibus): 0.000 Jarque-Bera (JB): 740086.464

Skew: 3.707 Prob(JB): 0.00

Kurtosis: 86.727 Cond. No. 85.2

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

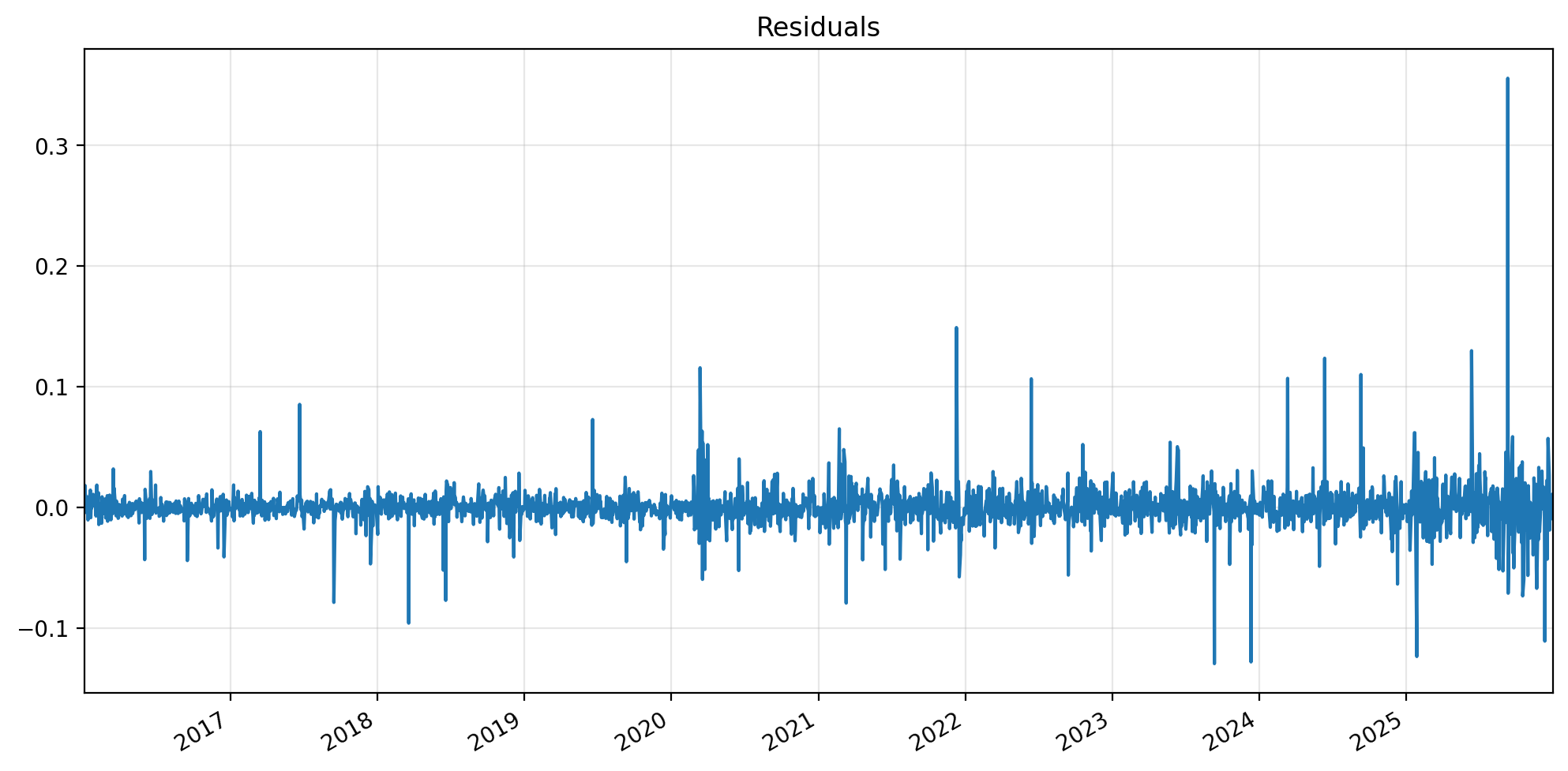

ax = reg_rslt.resid.plot(figsize=(12,6));

ax.set_xlim(reg.index.min(), reg.index.max())

ax.set_xlabel('')

ax.grid(alpha=0.3)

ax.set_title('Residuals')

plt.show()

The volatility of the residuals give the idiosyncratic volatility of the returns.

reg_rslt.resid.std()

0.017272941420857096

Note that, by construction, the total volatility of the stock return must be greater than the idiosyncratic volatility. (This is just a different way of saying that \(RSS\leq TSS\).)

reg['exret'].std()

0.0207756215162608

The regression equation implies a decomposition of the total variance:

Exercise

Write an expression that verifies that this equation holds for this regression.

Solution

np.isclose(reg_rslt.params['mktrf']**2 * reg['mktrf'].var() + reg_rslt.resid.var(),

reg['exret'].var())

Fama–French 3-factor model#

The 3-factor model regression equation is:

reg_model = sm.OLS(reg['exret'],

sm.add_constant(reg[['mktrf', 'smb', 'hml']]))

reg_rslt = reg_model.fit()

print(reg_rslt.summary())

OLS Regression Results

==============================================================================

Dep. Variable: exret R-squared: 0.323

Model: OLS Adj. R-squared: 0.322

Method: Least Squares F-statistic: 398.9

Date: Sun, 15 Feb 2026 Prob (F-statistic): 7.28e-212

Time: 19:54:33 Log-Likelihood: 6662.5

No. Observations: 2514 AIC: -1.332e+04

Df Residuals: 2510 BIC: -1.329e+04

Df Model: 3

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0003 0.000 0.800 0.424 -0.000 0.001

mktrf 1.0268 0.030 34.104 0.000 0.968 1.086

smb -0.3549 0.052 -6.761 0.000 -0.458 -0.252

hml -0.0879 0.037 -2.351 0.019 -0.161 -0.015

==============================================================================

Omnibus: 2356.117 Durbin-Watson: 2.032

Prob(Omnibus): 0.000 Jarque-Bera (JB): 748357.886

Skew: 3.690 Prob(JB): 0.00

Kurtosis: 87.201 Cond. No. 156.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

reg_rslt.resid.std()

0.017096011983458715

Exercise

Notice that the idiosyncratic volatility from the three-factor model is (a little) less than it was in the one-factor model. Do you think this will always be true? Why?

def regression(permno):

reg = ff.merge(rets[permno], left_index=True, right_index=True)

reg['exret'] = reg[permno] - reg['rf']

reg = reg.dropna()

reg = reg.apply(lambda x: x.astype(float))

reg_model = sm.OLS(reg['exret'],

sm.add_constant(reg[['mktrf', 'smb', 'hml']]))

reg_rslt = reg_model.fit()

params = reg_rslt.params

tvals = reg_rslt.tvalues

tvals.index = map(lambda x: 't_'+x, tvals.index) # rename t-value index values

rslt = pd.concat([params, tvals])

rslt['idiovol'] = reg_rslt.resid.std()

rslt['R2'] = reg_rslt.rsquared

rslt['N'] = reg_rslt.nobs

return(rslt)

regression(10104)

const 0.000273

mktrf 1.026765

smb -0.354892

hml -0.087928

t_const 0.800287

t_mktrf 34.103529

t_smb -6.760801

t_hml -2.350719

idiovol 0.017096

R2 0.322855

N 2514.000000

dtype: float64

We can now run regressions for each stock in our sample, simply by iterating over the columns of rets dataframe.

betas = {}

resids = {}

for permno in rets:

rslt = regression(permno)

betas[permno] = rslt

resids = pd.DataFrame(resids)

# transpose betas dataframe so coefficient estimates are columns

betas = pd.DataFrame(betas).T

betas.index.name = 'permno'

betas

/opt/anaconda3/envs/data/lib/python3.12/site-packages/statsmodels/regression/linear_model.py:1782: RuntimeWarning: divide by zero encountered in scalar divide

return 1 - self.ssr/self.centered_tss

| N | R2 | const | hml | idiovol | mktrf | smb | t_const | t_hml | t_mktrf | t_smb | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| permno | |||||||||||

| 10001 | 401.0 | 0.004700 | 0.001831 | 0.348477 | 0.034141 | 0.077337 | 0.152102 | 1.065768 | 1.141784 | 0.306119 | 0.429521 |

| 10025 | 266.0 | 0.052959 | 0.001478 | 0.156676 | 0.036224 | 0.361120 | 1.288365 | 0.656756 | 0.397269 | 1.265723 | 2.935178 |

| 10026 | 2514.0 | 0.243397 | -0.000257 | 0.434668 | 0.015573 | 0.628506 | 0.332158 | -0.825597 | 12.757001 | 22.916744 | 6.946431 |

| 10028 | 2514.0 | 0.059242 | 0.002000 | -0.116842 | 0.040246 | 0.581258 | 0.868260 | 2.486884 | -1.326913 | 8.200980 | 7.026191 |

| 10032 | 2514.0 | 0.474473 | 0.000275 | 0.381584 | 0.014681 | 0.935942 | 0.898653 | 0.935770 | 11.880024 | 36.201666 | 19.936335 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 93272 | 2514.0 | 0.283822 | 0.000685 | -0.240025 | 0.027414 | 1.120369 | 1.195174 | 1.250121 | -4.001759 | 23.206363 | 14.198773 |

| 93289 | 2514.0 | 0.364591 | -0.000096 | -0.279522 | 0.029620 | 1.619436 | 1.130870 | -0.163033 | -4.313268 | 31.046068 | 12.434518 |

| 93312 | 2514.0 | 0.478956 | -0.000040 | 0.090056 | 0.012845 | 1.021770 | 0.189439 | -0.154002 | 3.204478 | 45.169867 | 4.803289 |

| 93339 | 2190.0 | 0.051517 | -0.000048 | 0.062933 | 0.049997 | 0.758708 | 0.854044 | -0.044591 | 0.551746 | 8.131942 | 5.227847 |

| 93399 | 768.0 | 0.011111 | -0.001056 | 0.677137 | 0.067454 | -0.597287 | -0.298509 | -0.432363 | 1.539241 | -2.051509 | -0.616744 |

1000 rows × 11 columns

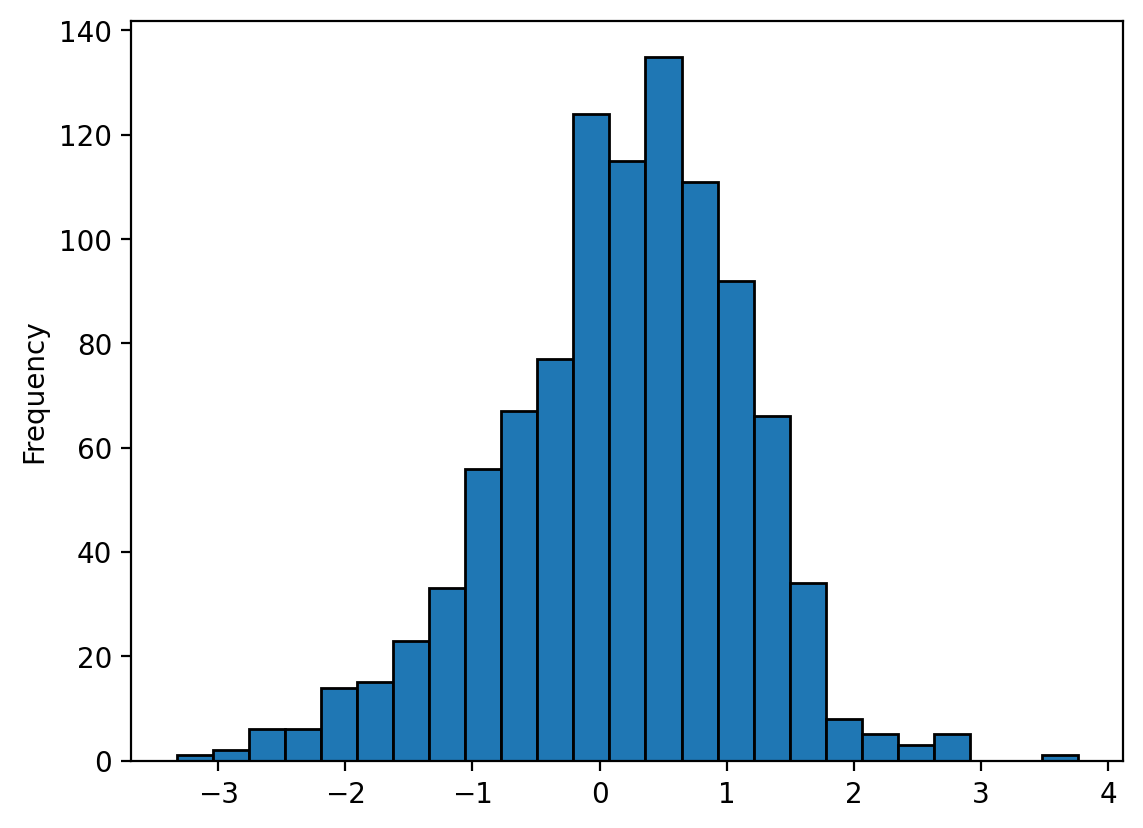

betas['mktrf'].plot.hist(bins=25, edgecolor='k');

betas['mktrf'].mean()

0.8982117048905841

# Add stock names to the betas dataframe

names = db.get_table('crsp', 'stocknames', columns=['permno', 'comnam', 'nameenddt'], date_cols=['nameenddt'])

# Keep only the last name for each permno

names = names.groupby('permno').last()

betas = betas.merge(names, left_index=True, right_index=True)

betas[betas['mktrf']<0].sort_values('mktrf')

| N | R2 | const | hml | idiovol | mktrf | smb | t_const | t_hml | t_mktrf | t_smb | comnam | nameenddt | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| permno | |||||||||||||

| 92805 | 83.0 | 0.025865 | -0.002946 | 1.504742 | 0.099863 | -1.264681 | 1.803016 | -0.262254 | 0.842205 | -1.181817 | 0.894746 | TIANYIN PHARMACEUTICAL CO INC | 2016-04-29 |

| 12509 | 452.0 | 0.002087 | 0.006419 | 0.658607 | 0.137706 | -0.735246 | -0.168119 | 0.983660 | 0.552994 | -0.742823 | -0.121706 | WOLVERINE BANCORP INC | 2017-10-16 |

| 93399 | 768.0 | 0.011111 | -0.001056 | 0.677137 | 0.067454 | -0.597287 | -0.298509 | -0.432363 | 1.539241 | -2.051509 | -0.616744 | NATIONAL AMERICAN UNIV HLDGS INC | 2019-01-18 |

| 15292 | 366.0 | 0.033693 | 0.001854 | 0.283895 | 0.016705 | -0.440383 | 0.150763 | 2.104024 | 1.772076 | -3.266097 | 0.814962 | CARDCONNECT CORP | 2017-07-05 |

| 13970 | 814.0 | 0.003625 | 0.001215 | -0.261854 | 0.052162 | -0.270108 | 0.421342 | 0.662382 | -0.789101 | -1.219093 | 1.145360 | TRUETT HURST INC | 2019-03-27 |

| 88257 | 495.0 | 0.014157 | 0.001129 | 0.465077 | 0.024545 | -0.256056 | 0.261237 | 1.015032 | 2.276387 | -1.478651 | 1.108905 | PEOPLES FINANCIAL CORP MS | 2017-12-15 |

| 59192 | 10.0 | 0.228028 | -0.002826 | -0.920269 | 0.007992 | -0.158150 | 0.345276 | -0.475726 | -0.773162 | -0.517802 | 0.299794 | CHUBB CORP | 2016-01-14 |

| 12922 | 191.0 | 0.070417 | 0.001682 | 0.289971 | 0.034447 | -0.152218 | 1.998889 | 0.667511 | 0.629909 | -0.521535 | 3.666602 | SKULLCANDY INC | 2016-10-03 |

| 90954 | 390.0 | 0.000587 | 0.002236 | 0.064411 | 0.047161 | -0.136648 | 0.189104 | 0.929387 | 0.151369 | -0.391066 | 0.381752 | SAJAN INC | 2017-07-19 |

| 14880 | 292.0 | 0.008853 | 0.004246 | -0.810888 | 0.056288 | -0.129838 | 0.426573 | 1.273035 | -1.365786 | -0.296054 | 0.651811 | WAFERGEN BIO SYSTEMS INC | 2017-02-28 |

| 15011 | 884.0 | 0.002241 | 0.000342 | 0.042635 | 0.016072 | -0.073369 | -0.041232 | 0.629508 | 0.434761 | -1.107577 | -0.378958 | MELROSE BANCORP INC | 2019-07-08 |

| 83762 | 2464.0 | 0.022696 | -0.001237 | -1.018439 | 0.069745 | -0.068131 | 0.794118 | -0.878637 | -6.642836 | -0.542151 | 3.685498 | AIM IMMUNOTECH INC | 2024-12-31 |

| 15905 | 621.0 | 0.000233 | 0.001361 | 0.165555 | 0.084723 | -0.052705 | 0.200668 | 0.397848 | 0.251666 | -0.115932 | 0.288514 | NAKED BRAND GROUP INC | 2018-06-19 |

betas['R2'].describe()

count 1000.000000

mean -inf

std NaN

min -inf

25% 0.066643

50% 0.195681

75% 0.341969

max 0.828717

Name: R2, dtype: float64

betas[betas['R2'] < 0.0]

| N | R2 | const | hml | idiovol | mktrf | smb | t_const | t_hml | t_mktrf | t_smb | comnam | nameenddt | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| permno | |||||||||||||

| 47088 | 1.0 | -inf | NaN | -0.71047 | NaN | 2.172398 | 1.18867 | NaN | -0.0 | 0.0 | 0.0 | KANSAS CITY LIFE INS CO | 2015-12-31 |

betas = betas.drop(47088)

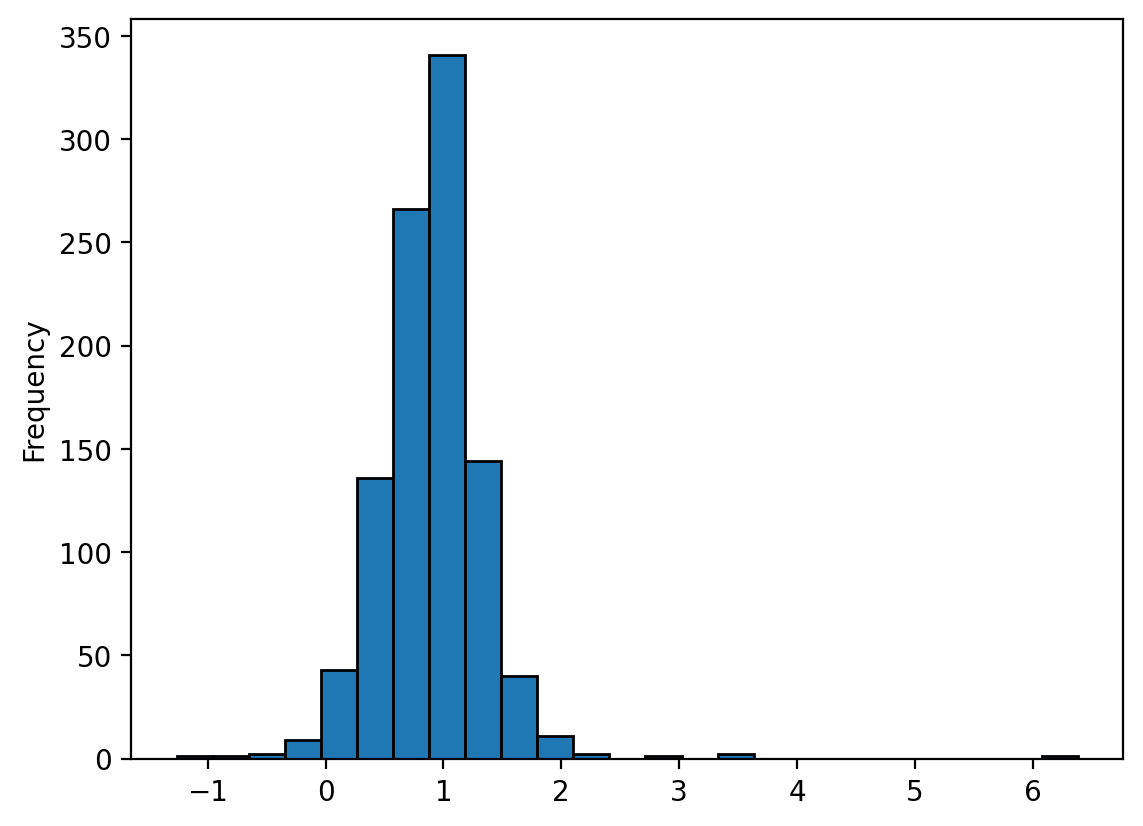

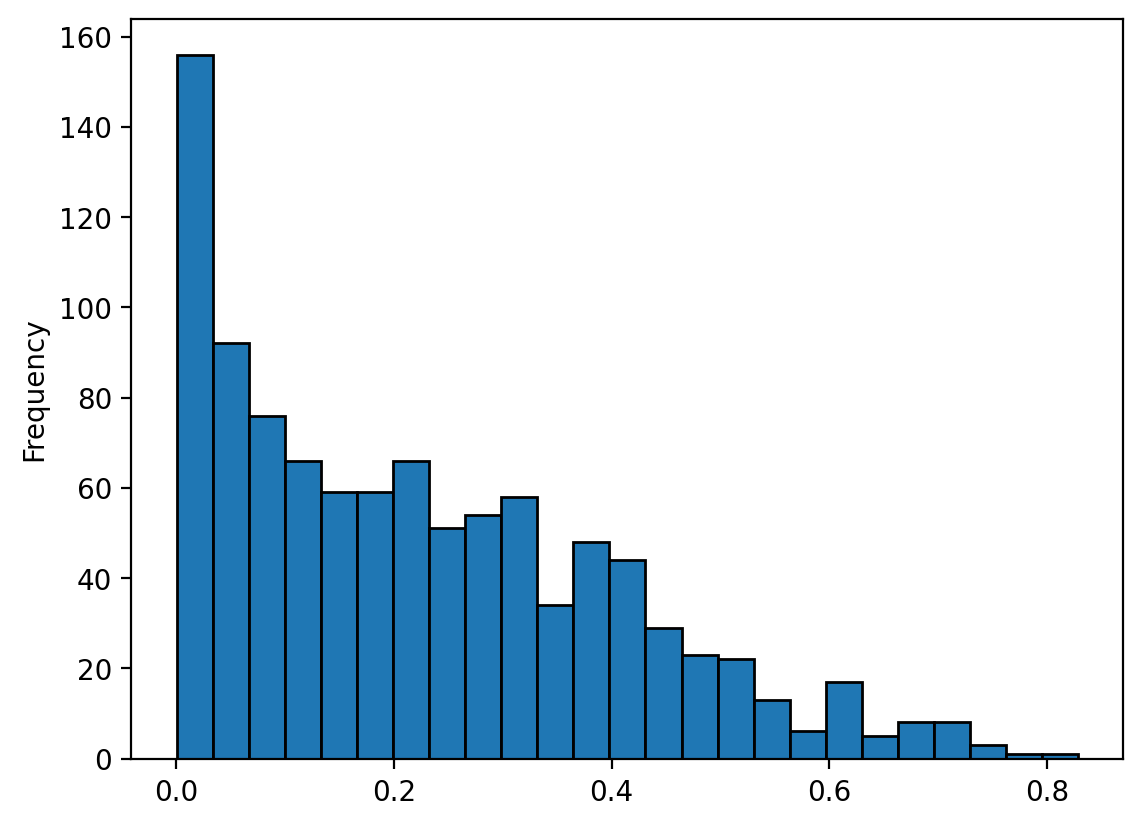

betas['R2'].plot.hist(bins=25, edgecolor='k');

betas[betas['R2']>0.7]

| N | R2 | const | hml | idiovol | mktrf | smb | t_const | t_hml | t_mktrf | t_smb | comnam | nameenddt | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| permno | |||||||||||||

| 10932 | 2514.0 | 0.717934 | -0.000057 | 1.420335 | 0.013391 | 1.361483 | 0.782681 | -0.212183 | 48.479595 | 57.734119 | 19.036142 | WEBSTER FINANCIAL CORP | 2024-12-31 |

| 35044 | 2514.0 | 0.746665 | 0.000121 | 1.349310 | 0.011505 | 1.298547 | 0.523922 | 0.528387 | 53.604703 | 64.091542 | 14.831443 | REGIONS FINANCIAL CORP NEW | 2024-12-31 |

| 47896 | 2514.0 | 0.728335 | 0.000210 | 0.892704 | 0.009058 | 1.139786 | -0.169259 | 1.162418 | 45.044981 | 71.451985 | -6.085798 | JPMORGAN CHASE & CO | 2024-12-31 |

| 66157 | 2514.0 | 0.707452 | -0.000225 | 1.093414 | 0.010319 | 1.122059 | 0.147498 | -1.089499 | 48.430625 | 61.745204 | 4.655304 | U S BANCORP DEL | 2024-12-31 |

| 71563 | 2514.0 | 0.719005 | -0.000195 | 1.198307 | 0.011222 | 1.238374 | 0.308653 | -0.869878 | 48.803316 | 62.659223 | 8.957321 | TRUIST FINANCIAL CORP | 2024-12-31 |

| 76624 | 10.0 | 0.755154 | 0.001325 | 0.535250 | 0.003929 | 0.518561 | -0.654305 | 0.453867 | 0.914690 | 3.453483 | -1.155578 | P M C SIERRA INC | 2016-01-14 |

| 76684 | 2514.0 | 0.745275 | 0.000123 | 1.487470 | 0.012616 | 1.307638 | 0.896711 | 0.486731 | 53.890514 | 58.857750 | 23.149540 | HANCOCK WHITNEY CORP | 2024-12-31 |

| 80808 | 30.0 | 0.828717 | 0.000751 | 1.076955 | 0.008316 | 1.060967 | 0.770422 | 0.446386 | 4.733552 | 9.252303 | 2.454555 | METRO BANCORP INC | 2016-02-12 |

| 81564 | 1133.0 | 0.768737 | 0.000275 | 1.666323 | 0.013799 | 1.372409 | 0.964430 | 0.669330 | 31.113339 | 40.372397 | 13.562480 | IBERIABANK CORP | 2020-07-01 |

| 86004 | 1802.0 | 0.716823 | -0.000103 | 1.156500 | 0.011686 | 1.108619 | 0.737802 | -0.375276 | 40.969616 | 48.727848 | 17.090251 | UMPQUA HOLDINGS CORP | 2023-02-28 |

| 86382 | 2514.0 | 0.720587 | -0.000077 | 1.153640 | 0.010462 | 0.928959 | 0.927366 | -0.370439 | 50.398813 | 50.419518 | 28.868681 | FIRST BUSEY CORP | 2024-12-31 |

| 88197 | 2514.0 | 0.709473 | -0.000018 | 1.257466 | 0.011364 | 1.044199 | 0.767379 | -0.077457 | 50.573076 | 52.174549 | 21.991694 | FULTON FINANCIAL CORP PA | 2024-12-31 |

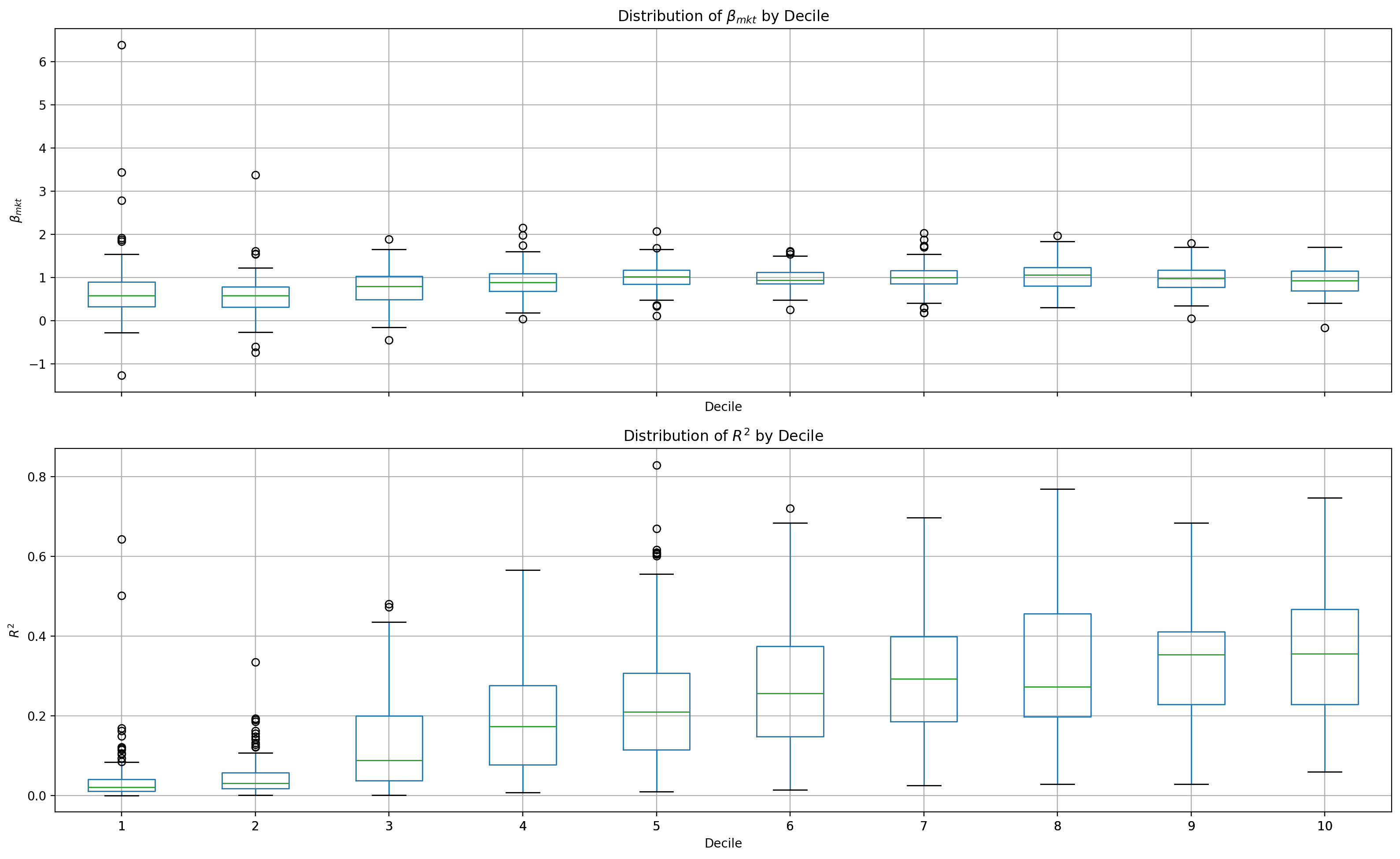

Next, we’ll generate a box-and-whiskers plot, which summarizes the distribution of estimated market betas within each size decile. For each decile, the box shows the median and interquartile range, while the whiskers show outliers of betas, highlighting how market exposure varies across firm sizes.

# add back the decile information

betas = betas.merge(crsp_smpl[['permno', 'decile']], left_index=True, right_on='permno')

fig, axes = plt.subplots(2, 1, figsize=(16, 10), sharex=True)

betas.boxplot(column='mktrf', by='decile', ax=axes[0])

betas.boxplot(column='R2', by='decile', ax=axes[1])

for i, col in enumerate(['mktrf', 'R2']):

axes[i].set_xlabel('Decile')

label = r'$\beta_{mkt}$' if col == 'mktrf' else r'$R^2$'

axes[i].set_ylabel(label)

axes[i].set_title(f'Distribution of {label} by Decile')

fig.suptitle('')

fig.tight_layout()

plt.show()

Are alphas zero?#

betas['const'].describe()

count 999.000000

mean 0.000240

std 0.012683

min -0.106850

25% -0.000215

50% 0.000128

75% 0.000518

max 0.381501

Name: const, dtype: float64

To determine whether the \(\alpha_i\) are statistically different from zero, we divide the average \(\alpha\) by the standard error of the mean, \(\sigma/\sqrt{n}\), to calculate a \(t\)-statistic.

import scipy.stats as scs

print("SEM:\t{:.4f}".format(scs.sem(betas['const'])))

print("t-stat:\t{:.2f}".format(betas['const'].mean() / scs.sem(betas['const'])))

SEM: 0.0004

t-stat: 0.60

betas['t_const'].plot.hist(bins=25, edgecolor='k');