Volatility modeling#

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import wrds

db = wrds.Connection()

Loading library list...

Done

import statsmodels.api as sm

from statsmodels.tsa.arima.model import ARIMA

from statsmodels.tsa.stattools import acf, pacf

# This code will supress certain unnecessary warnings from the statsmodels package

import warnings

from statsmodels.tools.sm_exceptions import ValueWarning

warnings.filterwarnings('ignore', module='statsmodels', category=FutureWarning)

warnings.filterwarnings('ignore', module='statsmodels', category=ValueWarning)

We’ll be using the arch package, so be sure to have that installed.

from arch import arch_model

from arch.univariate import ARX, GARCH, EGARCH, ConstantMean, StudentsT, SkewStudent

sql = """

SELECT dlycaldt, dlyret

FROM crsp.dsf_v2

WHERE ticker = 'SPY' AND dlycaldt >= '1992-01-01'

"""

spy = db.raw_sql(sql, date_cols=['dlycaldt']).set_index('dlycaldt').dropna().sort_index()

spy = spy.squeeze()

spy.name = 'ret'

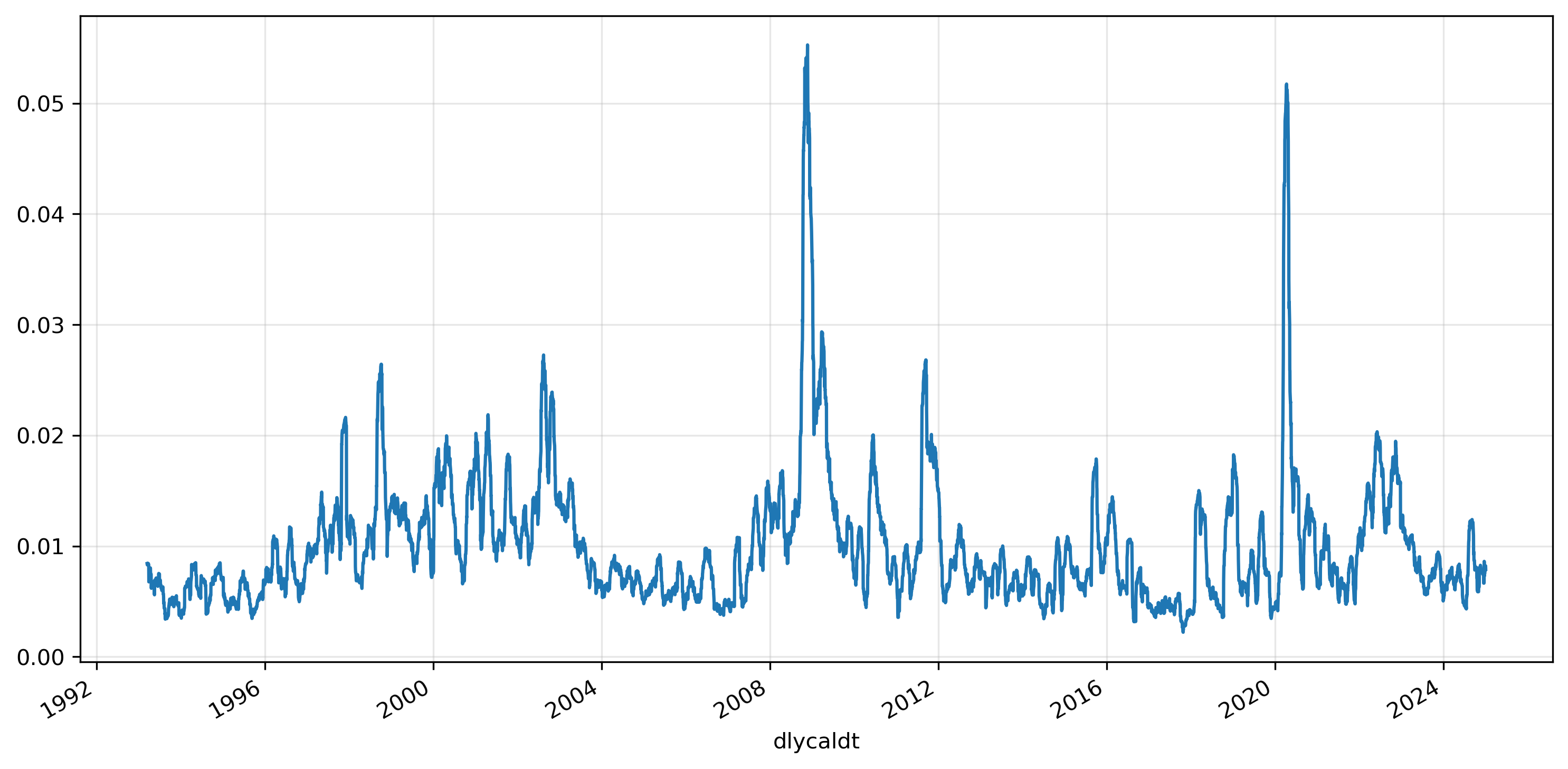

spy.rolling(30).std().plot(grid=True);

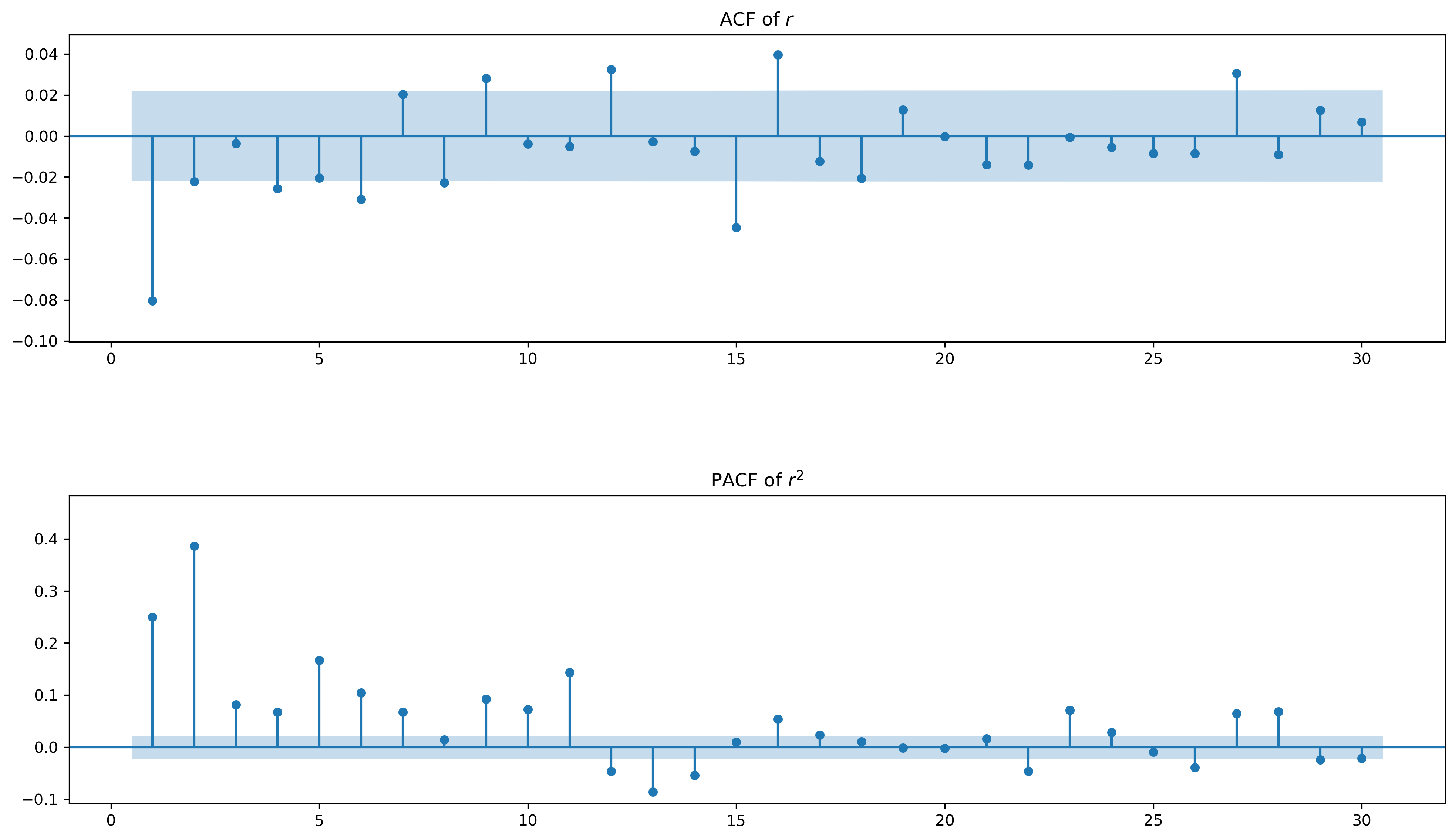

fig, (ax1,ax2) = plt.subplots(2,1,figsize=(16,9))

fig = sm.graphics.tsa.plot_acf(spy, lags=30, zero=False, auto_ylims=True, ax=ax1)

ax1.set_title('ACF of $r$')

fig = sm.graphics.tsa.plot_pacf(spy**2, lags=30, ax=ax2, zero=False, auto_ylims=True)

ax2.set_title('PACF of $r^2$')

plt.subplots_adjust(hspace=0.5)

plt.show()

GARCH#

If we specify an ARMA model for \(\sigma^2\), the model is called a generalized autoregressive conditional heteroskedasticity (GARCH) model.

Notice that as \(\sigma_t\) changes, the volatility of \(\varepsilon_t\) changes. Obviously, if \(\sigma_t=1\) then \(\varepsilon_t=e_t\) has a variance of 1. But suppose that \(\sigma_t=1.5\). Now

so the volatility of \(\varepsilon_t\) is 1.5. In other words, the volatility of the noise term is controlled entirely by \(\sigma_t\), which we allow to vary over time.

More generally, a GARCH(\(p,q\)) model specifies a variance of

# scaling helps with log-likelihood maximization

spy = spy*100

mod1 = ConstantMean(spy)

mod1.volatility = GARCH(p=1,q=1)

res1 = mod1.fit(disp='on')

print(res1.summary())

Iteration: 1, Func. Count: 6, Neg. LLF: 20062887524.700806

Iteration: 2, Func. Count: 15, Neg. LLF: 4466900010.967097

Iteration: 3, Func. Count: 22, Neg. LLF: 15260.542033681926

Iteration: 4, Func. Count: 29, Neg. LLF: 412871363.43178666

Iteration: 5, Func. Count: 36, Neg. LLF: 10990.878452086183

Iteration: 6, Func. Count: 42, Neg. LLF: 10888.236448941509

Iteration: 7, Func. Count: 48, Neg. LLF: 10996.484425467956

Iteration: 8, Func. Count: 54, Neg. LLF: 10864.646830478745

Iteration: 9, Func. Count: 59, Neg. LLF: 10959.529518585998

Iteration: 10, Func. Count: 65, Neg. LLF: 10864.334592763795

Iteration: 11, Func. Count: 70, Neg. LLF: 10864.327018863847

Iteration: 12, Func. Count: 75, Neg. LLF: 10864.326967600262

Iteration: 13, Func. Count: 80, Neg. LLF: 10864.326964939455

Iteration: 14, Func. Count: 84, Neg. LLF: 10864.32696493941

Constant Mean - GARCH Model Results

==============================================================================

Dep. Variable: ret R-squared: 0.000

Mean Model: Constant Mean Adj. R-squared: 0.000

Vol Model: GARCH Log-Likelihood: -10864.3

Distribution: Normal AIC: 21736.7

Method: Maximum Likelihood BIC: 21764.6

No. Observations: 8037

Date: Wed, Apr 23 2025 Df Residuals: 8036

Time: 09:26:54 Df Model: 1

Mean Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

mu 0.0753 8.903e-03 8.456 2.770e-17 [5.783e-02,9.273e-02]

Volatility Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

omega 0.0206 4.078e-03 5.058 4.229e-07 [1.264e-02,2.862e-02]

alpha[1] 0.1126 1.159e-02 9.711 2.719e-22 [8.984e-02, 0.135]

beta[1] 0.8720 1.227e-02 71.079 0.000 [ 0.848, 0.896]

============================================================================

Covariance estimator: robust

The estimated model is

Notice that \(\alpha+\beta \approx 1\). This is commonly observed with financial data, and the related IGARCH model requires \(\alpha+\beta=1\) as a constraint in the estimation.

res1.params

mu 0.075280

omega 0.020628

alpha[1] 0.112557

beta[1] 0.871952

Name: params, dtype: float64

The conditional volatility is the estimate of the time series of \(\sigma^2\).

res1.conditional_volatility

dlycaldt

1993-02-01 0.774564

1993-02-02 0.767641

1993-02-03 0.732493

1993-02-04 0.772639

1993-02-05 0.744587

...

2024-12-24 1.061264

2024-12-26 1.059975

2024-12-27 1.000418

2024-12-30 1.018096

2024-12-31 1.044503

Name: cond_vol, Length: 8037, dtype: float64

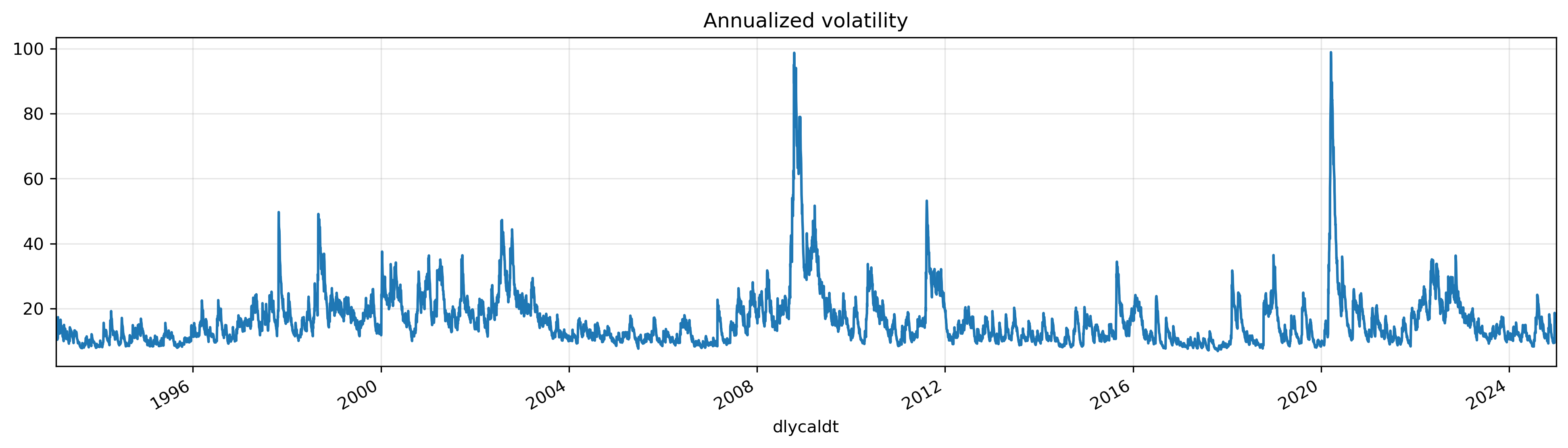

(res1.conditional_volatility * np.sqrt(252)).plot(figsize=(16, 4), grid=True)

plt.xlim(spy.index[0], spy.index[-1])

plt.title('Annualized volatility')

plt.show()

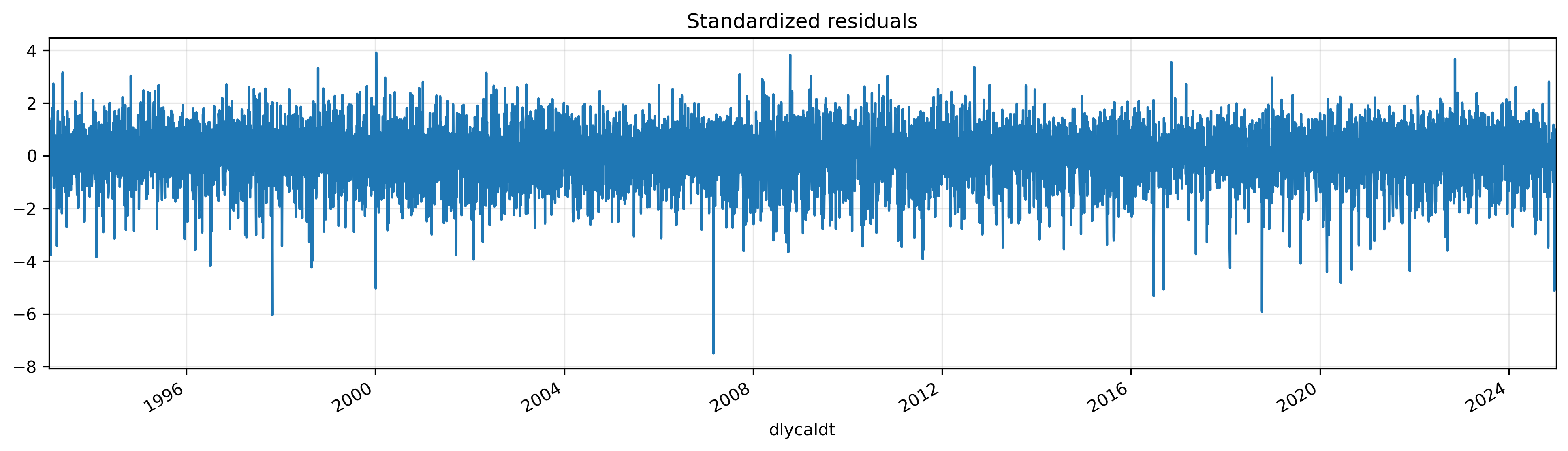

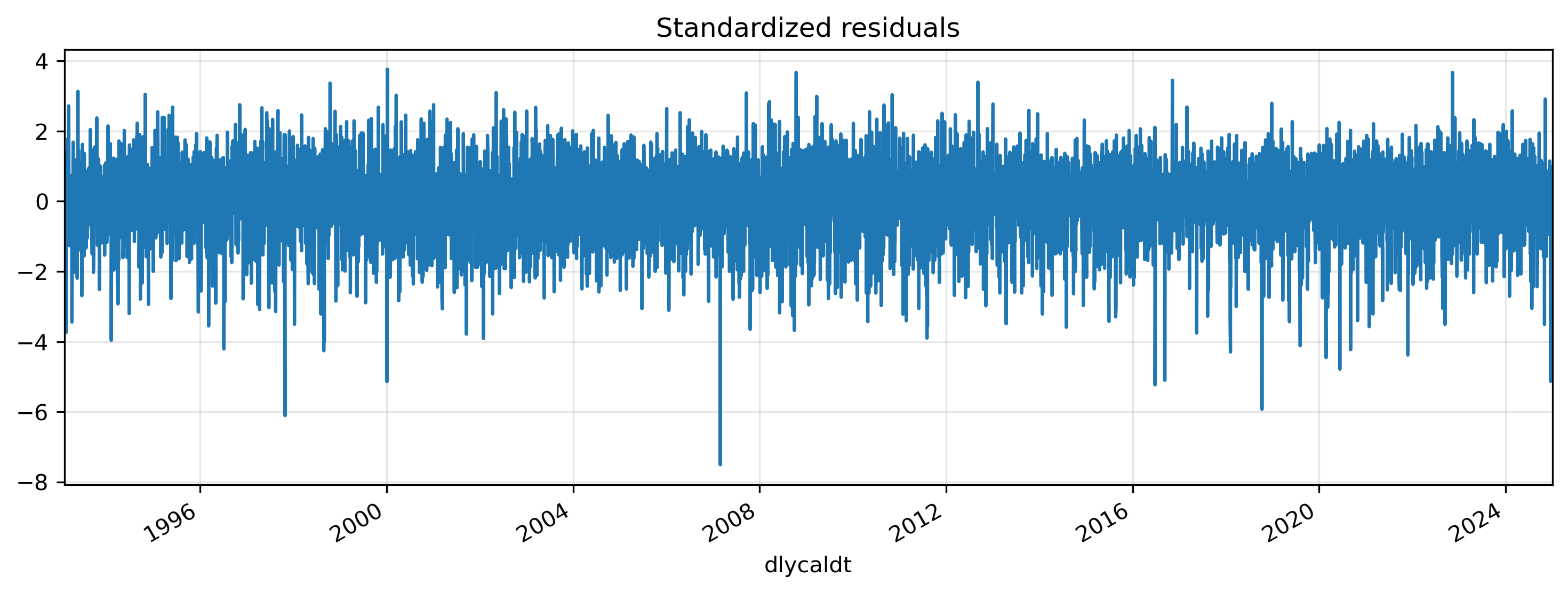

std_resid = res1.resid / res1.conditional_volatility

std_resid.plot(figsize=(16,4), grid=True)

plt.xlim(spy.index[0], spy.index[-1])

plt.title('Standardized residuals')

plt.show();

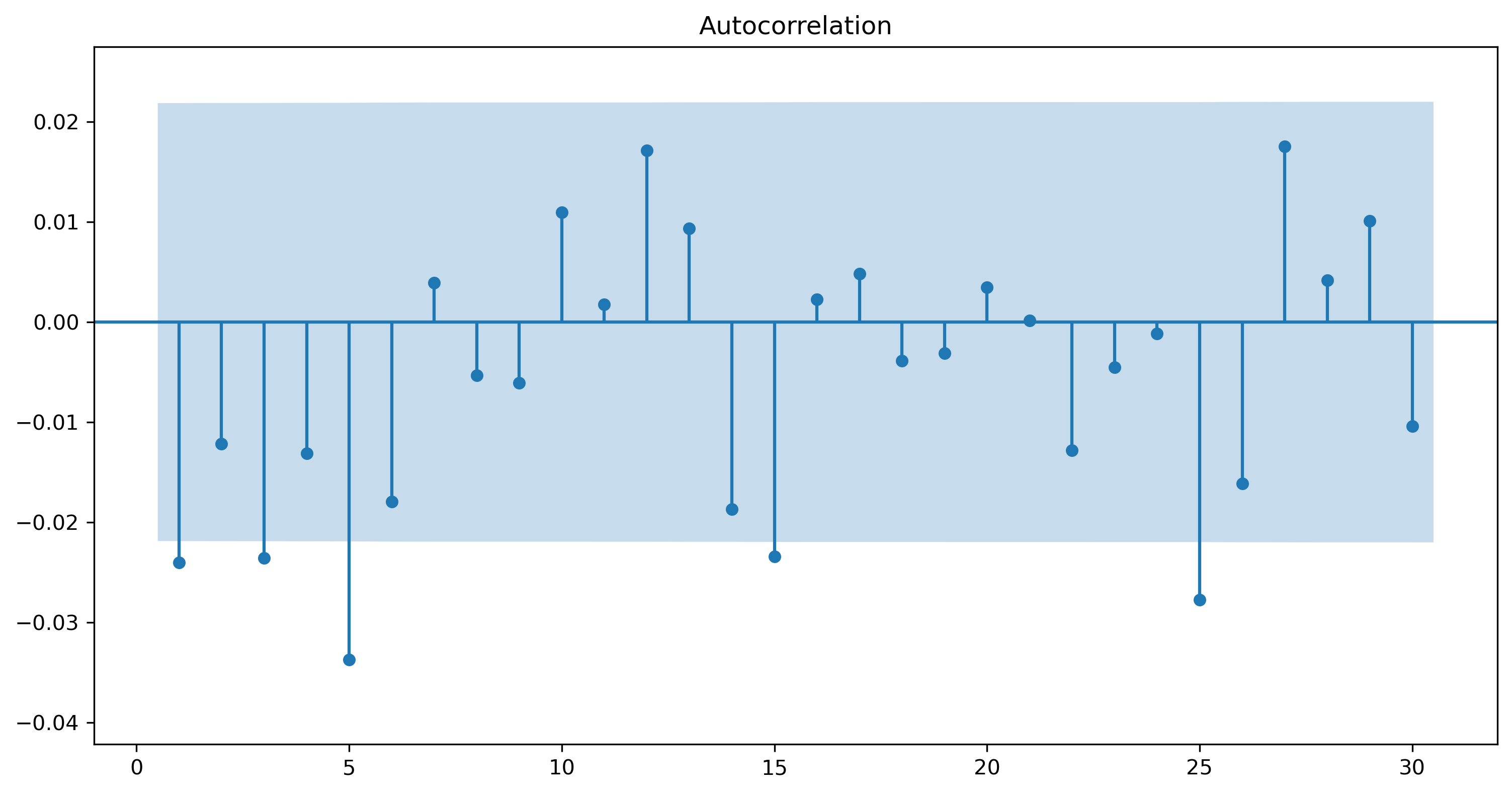

fig = sm.graphics.tsa.plot_acf(std_resid.values, lags=30, zero=False, auto_ylims=True)

We don’t have to assume a constant mean for the return process. Instead, we can combine an AR process in the return with GARCH volatility. For example, we can fit an AR(3) model to the data. We’ll start with just an AR(3), and then add in the GARCH process for the volatility.

ar3 = ARIMA(spy, order=(3,0,0)).fit()

print(ar3.summary())

SARIMAX Results

==============================================================================

Dep. Variable: ret No. Observations: 8037

Model: ARIMA(3, 0, 0) Log Likelihood -12642.957

Date: Wed, 23 Apr 2025 AIC 25295.913

Time: 09:31:31 BIC 25330.872

Sample: 0 HQIC 25307.876

- 8037

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0461 0.012 3.735 0.000 0.022 0.070

ar.L1 -0.0829 0.006 -13.956 0.000 -0.095 -0.071

ar.L2 -0.0296 0.005 -6.379 0.000 -0.039 -0.021

ar.L3 -0.0080 0.006 -1.387 0.165 -0.019 0.003

sigma2 1.3611 0.009 150.470 0.000 1.343 1.379

===================================================================================

Ljung-Box (L1) (Q): 0.00 Jarque-Bera (JB): 38747.82

Prob(Q): 0.98 Prob(JB): 0.00

Heteroskedasticity (H): 0.87 Skew: -0.20

Prob(H) (two-sided): 0.00 Kurtosis: 13.75

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

mod2 = ARX(spy, lags=3)

mod2.volatility = GARCH(p=1,q=1)

res2 = mod2.fit(disp='off')

print(res2.summary())

AR - GARCH Model Results

==============================================================================

Dep. Variable: ret R-squared: 0.004

Mean Model: AR Adj. R-squared: 0.003

Vol Model: GARCH Log-Likelihood: -10852.4

Distribution: Normal AIC: 21718.8

Method: Maximum Likelihood BIC: 21767.7

No. Observations: 8034

Date: Wed, Apr 23 2025 Df Residuals: 8030

Time: 09:31:46 Df Model: 4

Mean Model

==============================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------------

Const 0.0818 9.455e-03 8.650 5.134e-18 [6.326e-02, 0.100]

ret[1] -0.0371 1.192e-02 -3.110 1.870e-03 [-6.044e-02,-1.371e-02]

ret[2] -0.0173 1.294e-02 -1.337 0.181 [-4.266e-02,8.062e-03]

ret[3] -0.0303 1.235e-02 -2.451 1.425e-02 [-5.448e-02,-6.065e-03]

Volatility Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

omega 0.0205 4.096e-03 5.012 5.393e-07 [1.250e-02,2.856e-02]

alpha[1] 0.1118 1.172e-02 9.539 1.443e-21 [8.881e-02, 0.135]

beta[1] 0.8727 1.243e-02 70.204 0.000 [ 0.848, 0.897]

============================================================================

Covariance estimator: robust

In a model with \(k\) lags of the time series, the conditional volatility will be missing for \(k\) periods.

res2.conditional_volatility

dlycaldt

1993-02-01 NaN

1993-02-02 NaN

1993-02-03 NaN

1993-02-04 0.796735

1993-02-05 0.769729

...

2024-12-24 1.054962

2024-12-26 1.058383

2024-12-27 0.999064

2024-12-30 1.012957

2024-12-31 1.041451

Name: cond_vol, Length: 8037, dtype: float64

We can “prune” the model by dropping insignificant parameters.

mod2 = ARX(spy, lags=[1,3])

mod2.volatility = GARCH(p=1,q=1)

res2 = mod2.fit(disp='off')

print(res2.summary())

AR - GARCH Model Results

==============================================================================

Dep. Variable: ret R-squared: 0.003

Mean Model: AR Adj. R-squared: 0.003

Vol Model: GARCH Log-Likelihood: -10853.4

Distribution: Normal AIC: 21718.9

Method: Maximum Likelihood BIC: 21760.8

No. Observations: 8034

Date: Wed, Apr 23 2025 Df Residuals: 8031

Time: 09:32:21 Df Model: 3

Mean Model

==============================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------------

Const 0.0804 9.277e-03 8.668 4.408e-18 [6.223e-02,9.860e-02]

ret[1] -0.0365 1.190e-02 -3.068 2.154e-03 [-5.984e-02,-1.319e-02]

ret[3] -0.0299 1.232e-02 -2.427 1.521e-02 [-5.406e-02,-5.759e-03]

Volatility Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

omega 0.0206 4.087e-03 5.039 4.670e-07 [1.259e-02,2.861e-02]

alpha[1] 0.1121 1.166e-02 9.613 7.060e-22 [8.926e-02, 0.135]

beta[1] 0.8723 1.237e-02 70.494 0.000 [ 0.848, 0.897]

============================================================================

Covariance estimator: robust

std_resid2 = res2.resid / res2.conditional_volatility

ax = std_resid2.plot(figsize=(12,4), grid=True)

plt.xlim(spy.index[0], spy.index[-1])

plt.title('Standardized residuals')

plt.show()

<>:5: SyntaxWarning: invalid escape sequence '\h'

<>:10: SyntaxWarning: invalid escape sequence '\h'

<>:5: SyntaxWarning: invalid escape sequence '\h'

<>:10: SyntaxWarning: invalid escape sequence '\h'

/var/folders/8b/3b5yf0214zvg3prfcqs6wx3c0000gq/T/ipykernel_34885/12402403.py:5: SyntaxWarning: invalid escape sequence '\h'

ax1.set_title('ACF of $\hat{e}$')

/var/folders/8b/3b5yf0214zvg3prfcqs6wx3c0000gq/T/ipykernel_34885/12402403.py:10: SyntaxWarning: invalid escape sequence '\h'

ax2.set_title('ACF of $\hat{e}^2$')

acfn, qstats, pvals = acf(std_resid, qstat=True, nlags=15)

pvals

array([0.0312882 , 0.05431309, 0.01626493, 0.01993702, 0.00087765,

0.00067057, 0.00137535, 0.00251076, 0.00420409, 0.00528902,

0.00894994, 0.00672621, 0.00869598, 0.00566077, 0.00219161])

acfn, qstats, pvals = acf(std_resid**2, qstat=True, nlags=15)

pvals

array([0.2082051 , 0.026455 , 0.05056582, 0.0409472 , 0.06895238,

0.10024628, 0.15057953, 0.21706441, 0.25550552, 0.07400785,

0.10384168, 0.1058008 , 0.13347933, 0.17488681, 0.13722661])

EGARCH#

The EGARCH(\(p,q\)) model specifies the log-volatility process as follows:

where

Modeling the log of volatility ensures that volatility is always positive, so no additional constraints are required. And the weighted error structure allows for an asymmetric effect of a return innovation on the volatility:

That is, when an innovation \(e_{t-k}\) is positive, log-variance increases by \(\alpha_k(\theta+\lambda)\), but when the innovation is negative the log-variance decreases by \(\alpha_k(\theta-\lambda)\). This asymmetry allows for a “leverage effect” as we’ll soon see. (In either case, we also reduce the log-variance by \(\lambda E(|e_t|)\), which we’ll soon see is simply a number we can calculate.)

The arch package parameterizes the model as EGARCH(\(p,o,q\)) with

Comparing (18) and (19), we see that:

implementing the typical EGARCH(\(p,q\)) model implies that \(p=o\);

\(\gamma_k\) maps to \(\theta\alpha_k\) in equation (1); and

\(\alpha_k\) (in equation 2) maps to \(\lambda\alpha_k\) in equation (1).

The \(\gamma_k\) parameter is called the leverage parameter. If \(\gamma_k=0\) then there is no asymmetry in the volaility — positive and negative values of \(e_t\) have the same effect on \(\sigma_t^2\). If, however, \(\gamma<0\), then negative shocks will lead to larger increases in volatility than positive shocks.

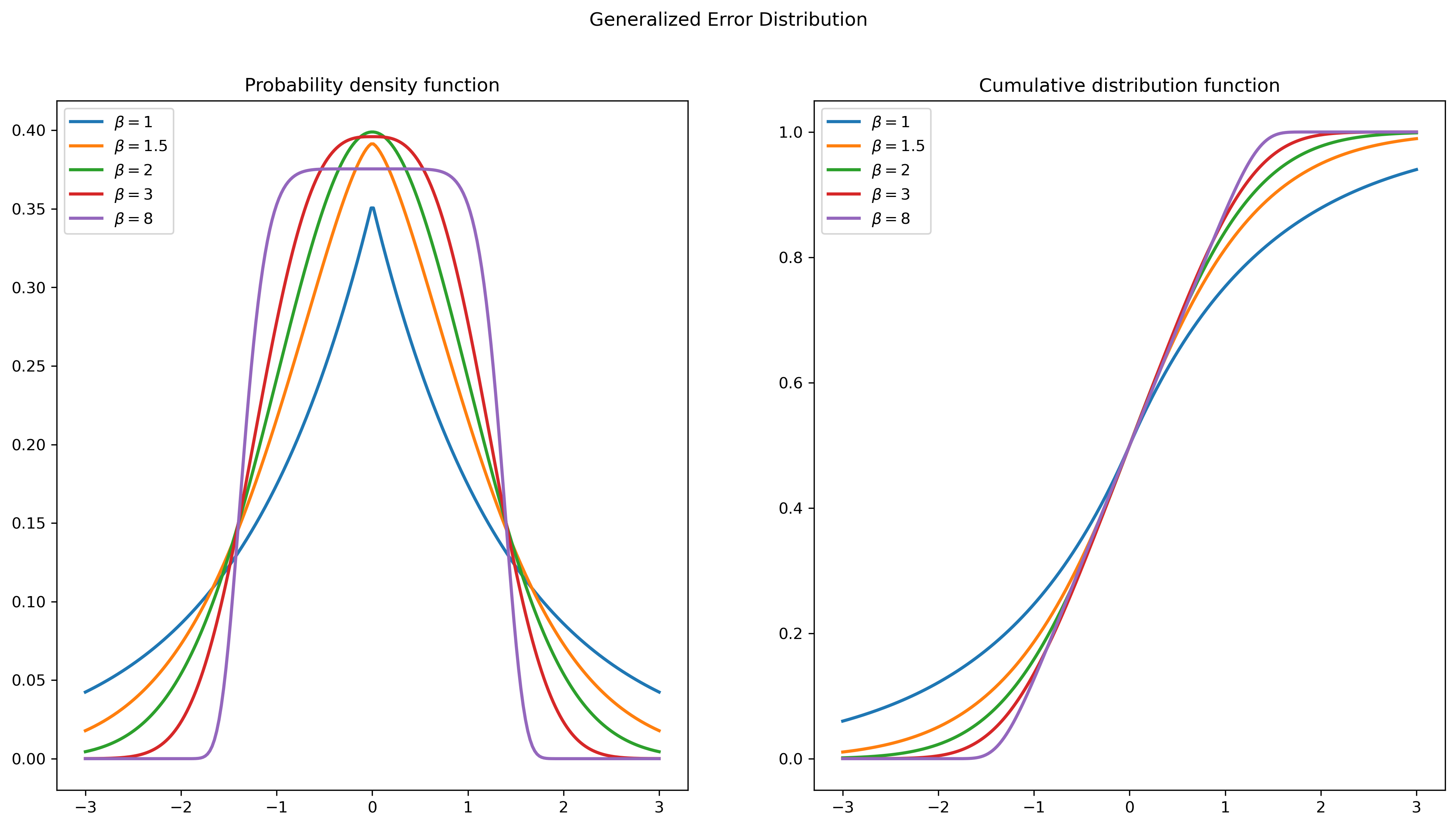

Error distributions#

Three distributions are often used for the innovation \(e_t\):

the Normal distribution;

the Student’s T distribution; or

the Generalized Error Distribution.

Each distributional assumption leads to a different value of \(E(|e_{t}|)\). With a Normal distribution we have

from scipy.stats import norm, t

from numpy import pi as π

# calculate E(|e|) for e~N(0,1)

norm().expect(lambda x: np.abs(x))

np.float64(0.7978845608028655)

np.sqrt(2/π)

np.float64(0.7978845608028654)

With a Student’s T distribution,

where \(\Gamma(z)\) is the gamma function.

def exp_abs_e(ν):

"""Calculate E(|e_t|) for a Student's T distribution"""

from scipy.special import gamma as Γ

return (2 * np.sqrt(ν-2) * Γ((ν+1)/2)) / ((ν-1) * Γ(ν/2) * np.sqrt(π))

df = 5

exp_abs_e(df)

np.float64(0.7351051938957227)

# standardized T-distribution

s = 1/np.sqrt(df/(df-2))

t_std = t(df=df, scale=s)

t_std.expect(lambda x: np.abs(x))

np.float64(0.7351051938957227)

The Generalized Error Distribution is an alternative distribution that nests the Normal distribution, as well as several other continuous distributions.

Estimation#

mod3 = ARX(spy, lags=1)

mod3.volatility = EGARCH(1,1,1)

res3 = mod3.fit()

print(res3.summary())

Iteration: 1, Func. Count: 8, Neg. LLF: 658936358519798.0

Iteration: 2, Func. Count: 20, Neg. LLF: 659173899730214.5

Iteration: 3, Func. Count: 31, Neg. LLF: 13060330235107.09

Iteration: 4, Func. Count: 42, Neg. LLF: 567638731477.8679

Iteration: 5, Func. Count: 53, Neg. LLF: 5037293988613.256

Iteration: 6, Func. Count: 64, Neg. LLF: 37499.435287587694

Iteration: 7, Func. Count: 74, Neg. LLF: 10832.126223824762

Iteration: 8, Func. Count: 82, Neg. LLF: 10695.267458503542

Iteration: 9, Func. Count: 89, Neg. LLF: 10695.264292207961

Iteration: 10, Func. Count: 96, Neg. LLF: 10695.264193180004

Iteration: 11, Func. Count: 103, Neg. LLF: 10695.264191980066

Iteration: 12, Func. Count: 109, Neg. LLF: 10695.26419197779

Optimization terminated successfully (Exit mode 0)

Current function value: 10695.264191980066

Iterations: 12

Function evaluations: 109

Gradient evaluations: 12

AR - EGARCH Model Results

==============================================================================

Dep. Variable: ret R-squared: 0.004

Mean Model: AR Adj. R-squared: 0.004

Vol Model: EGARCH Log-Likelihood: -10695.3

Distribution: Normal AIC: 21402.5

Method: Maximum Likelihood BIC: 21444.5

No. Observations: 8036

Date: Wed, Apr 23 2025 Df Residuals: 8034

Time: 09:35:59 Df Model: 2

Mean Model

==============================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------------

Const 0.0445 8.833e-03 5.037 4.729e-07 [2.718e-02,6.180e-02]

ret[1] -0.0293 1.244e-02 -2.354 1.858e-02 [-5.365e-02,-4.898e-03]

Volatility Model

=============================================================================

coef std err t P>|t| 95.0% Conf. Int.

-----------------------------------------------------------------------------

omega 1.1732e-03 2.615e-03 0.449 0.654 [-3.953e-03,6.299e-03]

alpha[1] 0.1633 1.539e-02 10.606 2.784e-26 [ 0.133, 0.193]

gamma[1] -0.1349 1.358e-02 -9.936 2.891e-23 [ -0.162, -0.108]

beta[1] 0.9718 4.199e-03 231.447 0.000 [ 0.964, 0.980]

=============================================================================

Covariance estimator: robust

mod4 = ARX(spy, lags=1)

mod4.volatility = EGARCH(2,2,2)

res4 = mod4.fit(disp='off')

print(res4.summary())

AR - EGARCH Model Results

==============================================================================

Dep. Variable: ret R-squared: 0.005

Mean Model: AR Adj. R-squared: 0.005

Vol Model: EGARCH Log-Likelihood: -10672.8

Distribution: Normal AIC: 21363.6

Method: Maximum Likelihood BIC: 21426.6

No. Observations: 8036

Date: Wed, Apr 23 2025 Df Residuals: 8034

Time: 09:36:12 Df Model: 2

Mean Model

==============================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------------

Const 0.0440 6.668e-03 6.599 4.150e-11 [3.093e-02,5.707e-02]

ret[1] -0.0408 7.131e-03 -5.728 1.015e-08 [-5.482e-02,-2.687e-02]

Volatility Model

=============================================================================

coef std err t P>|t| 95.0% Conf. Int.

-----------------------------------------------------------------------------

omega 1.5742e-03 2.624e-03 0.600 0.549 [-3.568e-03,6.717e-03]

alpha[1] 0.0431 4.314e-02 0.998 0.318 [-4.149e-02, 0.128]

alpha[2] 0.1319 7.768e-02 1.698 8.960e-02 [-2.039e-02, 0.284]

gamma[1] -0.2048 1.806e-02 -11.341 8.235e-30 [ -0.240, -0.169]

gamma[2] 0.0760 5.247e-02 1.448 0.147 [-2.684e-02, 0.179]

beta[1] 0.9700 0.307 3.159 1.584e-03 [ 0.368, 1.572]

beta[2] 0.0000 0.298 0.000 1.000 [ -0.584, 0.584]

=============================================================================

Covariance estimator: robust

mod5 = ARX(spy, lags=1)

mod5.volatility = EGARCH(1,1,1)

mod5.distribution = StudentsT()

res5 = mod5.fit(disp='off')

print(res5.summary())

AR - EGARCH Model Results

====================================================================================

Dep. Variable: ret R-squared: 0.004

Mean Model: AR Adj. R-squared: 0.004

Vol Model: EGARCH Log-Likelihood: -10521.6

Distribution: Standardized Student's t AIC: 21057.2

Method: Maximum Likelihood BIC: 21106.2

No. Observations: 8036

Date: Wed, Apr 23 2025 Df Residuals: 8034

Time: 09:36:14 Df Model: 2

Mean Model

==============================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------------

Const 0.0646 8.224e-03 7.856 3.976e-15 [4.849e-02,8.072e-02]

ret[1] -0.0326 1.068e-02 -3.056 2.246e-03 [-5.356e-02,-1.170e-02]

Volatility Model

==============================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------------

omega -1.0493e-03 2.366e-03 -0.443 0.657 [-5.687e-03,3.589e-03]

alpha[1] 0.1556 1.203e-02 12.938 2.752e-38 [ 0.132, 0.179]

gamma[1] -0.1471 1.065e-02 -13.815 2.060e-43 [ -0.168, -0.126]

beta[1] 0.9795 3.081e-03 317.900 0.000 [ 0.973, 0.986]

Distribution

========================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------

nu 6.6792 0.500 13.358 1.065e-40 [ 5.699, 7.659]

========================================================================

Covariance estimator: robust

# for the log-variance equation

exp_abs_e(res5.params['nu'])

np.float64(0.7566670989670168)

GJR-GARCH#

Glosten, Jagannathan, and Runkle (1993) develop another model that allows asymmetric effects on volatility, which became known as GJR-GARCH. They specify the following process for the variance:

where \(I\{\cdot\}\) is an indicator variable that equals one when the condition it evaluates is true, and zero otherwise.

mod6 = ARX(spy, lags=1)

mod6.volatility = GARCH(p=1,o=1,q=1)

res6 = mod6.fit(disp='off')

print(res6.summary())

AR - GJR-GARCH Model Results

==============================================================================

Dep. Variable: ret R-squared: 0.003

Mean Model: AR Adj. R-squared: 0.003

Vol Model: GJR-GARCH Log-Likelihood: -10725.2

Distribution: Normal AIC: 21462.3

Method: Maximum Likelihood BIC: 21504.3

No. Observations: 8036

Date: Wed, Apr 23 2025 Df Residuals: 8034

Time: 09:36:25 Df Model: 2

Mean Model

==============================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------------

Const 0.0437 8.902e-03 4.907 9.267e-07 [2.623e-02,6.113e-02]

ret[1] -0.0259 1.258e-02 -2.057 3.966e-02 [-5.054e-02,-1.225e-03]

Volatility Model

=============================================================================

coef std err t P>|t| 95.0% Conf. Int.

-----------------------------------------------------------------------------

omega 0.0213 4.986e-03 4.262 2.023e-05 [1.148e-02,3.103e-02]

alpha[1] 7.1828e-03 9.346e-03 0.769 0.442 [-1.113e-02,2.550e-02]

gamma[1] 0.1672 2.611e-02 6.405 1.504e-10 [ 0.116, 0.218]

beta[1] 0.8892 1.827e-02 48.669 0.000 [ 0.853, 0.925]

=============================================================================

Covariance estimator: robust

res6.std_resid.plot(figsize=(16,4), grid=True)

plt.title('Standardized residuals')

plt.xlim(spy.index[0], spy.index[-1])

plt.show()

TARCH#

The Threshold Autoregressive Conditional Heteroskedasticity model uses an indicator variable as in GJR–GARCH but also models the volatility using the absolute value of the innovations rather than modeling variance with the squares:

This is implemented by specifying a power variable of 1, rather than the default value of 2.

mod7 = ARX(spy, lags=1)

mod7.volatility = GARCH(1,1,1,power=1)

res7 = mod7.fit(disp='off')

print(res7.summary())

AR - TARCH/ZARCH Model Results

==============================================================================

Dep. Variable: ret R-squared: 0.004

Mean Model: AR Adj. R-squared: 0.003

Vol Model: TARCH/ZARCH Log-Likelihood: -10673.4

Distribution: Normal AIC: 21358.7

Method: Maximum Likelihood BIC: 21400.7

No. Observations: 8036

Date: Wed, Apr 23 2025 Df Residuals: 8034

Time: 09:36:50 Df Model: 2

Mean Model

==============================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------------

Const 0.0390 8.844e-03 4.413 1.019e-05 [2.169e-02,5.636e-02]

ret[1] -0.0274 1.257e-02 -2.178 2.942e-02 [-5.203e-02,-2.739e-03]

Volatility Model

=============================================================================

coef std err t P>|t| 95.0% Conf. Int.

-----------------------------------------------------------------------------

omega 0.0296 4.233e-03 7.002 2.523e-12 [2.134e-02,3.794e-02]

alpha[1] 0.0121 9.570e-03 1.263 0.207 [-6.668e-03,3.085e-02]

gamma[1] 0.1649 1.653e-02 9.980 1.872e-23 [ 0.133, 0.197]

beta[1] 0.8986 9.538e-03 94.210 0.000 [ 0.880, 0.917]

=============================================================================

Covariance estimator: robust

More general models can be obtained by specifying different values for the power, \(k\):