Applications#

import numpy as np

import pandas as pd

import pandas_datareader as pdr

import matplotlib.pyplot as plt

import statsmodels

import statsmodels.api as sm

from statsmodels.tsa import stattools as st

from statsmodels.tsa.arima_process import ArmaProcess

from statsmodels.tsa.ar_model import AutoReg, ar_select_order

from statsmodels.tsa.arima.model import ARIMA

# Suppress all warnings about future changes to syntax

from warnings import simplefilter

simplefilter(action='ignore', category=FutureWarning)

Unemployment#

This application follows example in Tsay (2018), chapter 1. We’ll begin by downloading monthly unemployment data. This series, calculated by the Bureau of Labor Statistics, is seasonally adjusted and begins in 1948.

ur = pdr.get_data_fred('UNRATE', 1948)

We’ll begin by calculating the average rate on a quarterly basis. This is simple to do using the resample method in pandas, which is possible since we have a DatetimeIndex.

ur.index

DatetimeIndex(['1948-01-01', '1948-02-01', '1948-03-01', '1948-04-01',

'1948-05-01', '1948-06-01', '1948-07-01', '1948-08-01',

'1948-09-01', '1948-10-01',

...

'2025-05-01', '2025-06-01', '2025-07-01', '2025-08-01',

'2025-09-01', '2025-10-01', '2025-11-01', '2025-12-01',

'2026-01-01', '2026-02-01'],

dtype='datetime64[ns]', name='DATE', length=938, freq=None)

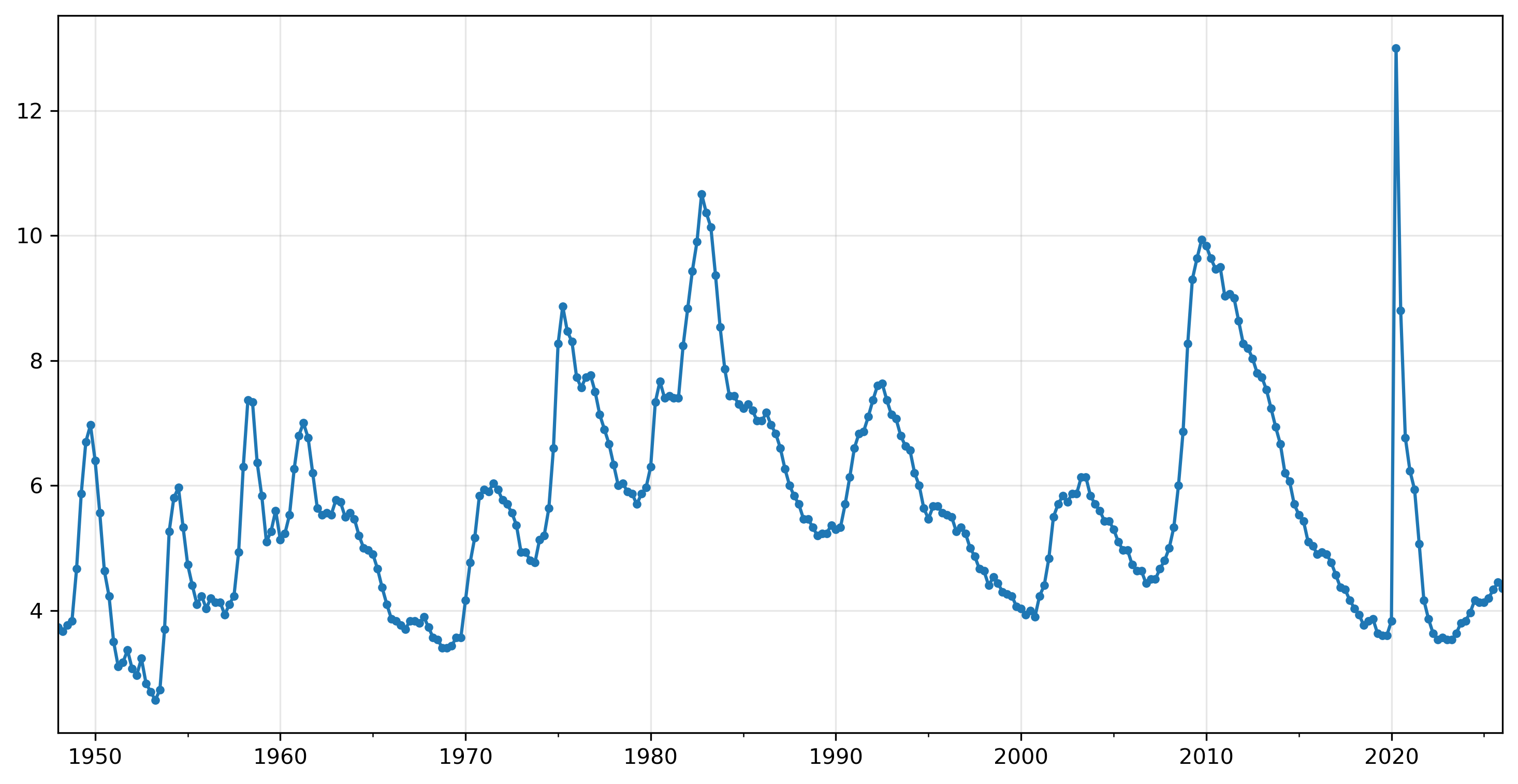

urq = ur.resample('Q')['UNRATE'].mean()

urq

DATE

1948-03-31 3.733333

1948-06-30 3.666667

1948-09-30 3.766667

1948-12-31 3.833333

1949-03-31 4.666667

...

2025-03-31 4.133333

2025-06-30 4.200000

2025-09-30 4.333333

2025-12-31 4.450000

2026-03-31 4.350000

Freq: QE-DEC, Name: UNRATE, Length: 313, dtype: float64

urq.plot(marker='.', xlabel='', grid=True);

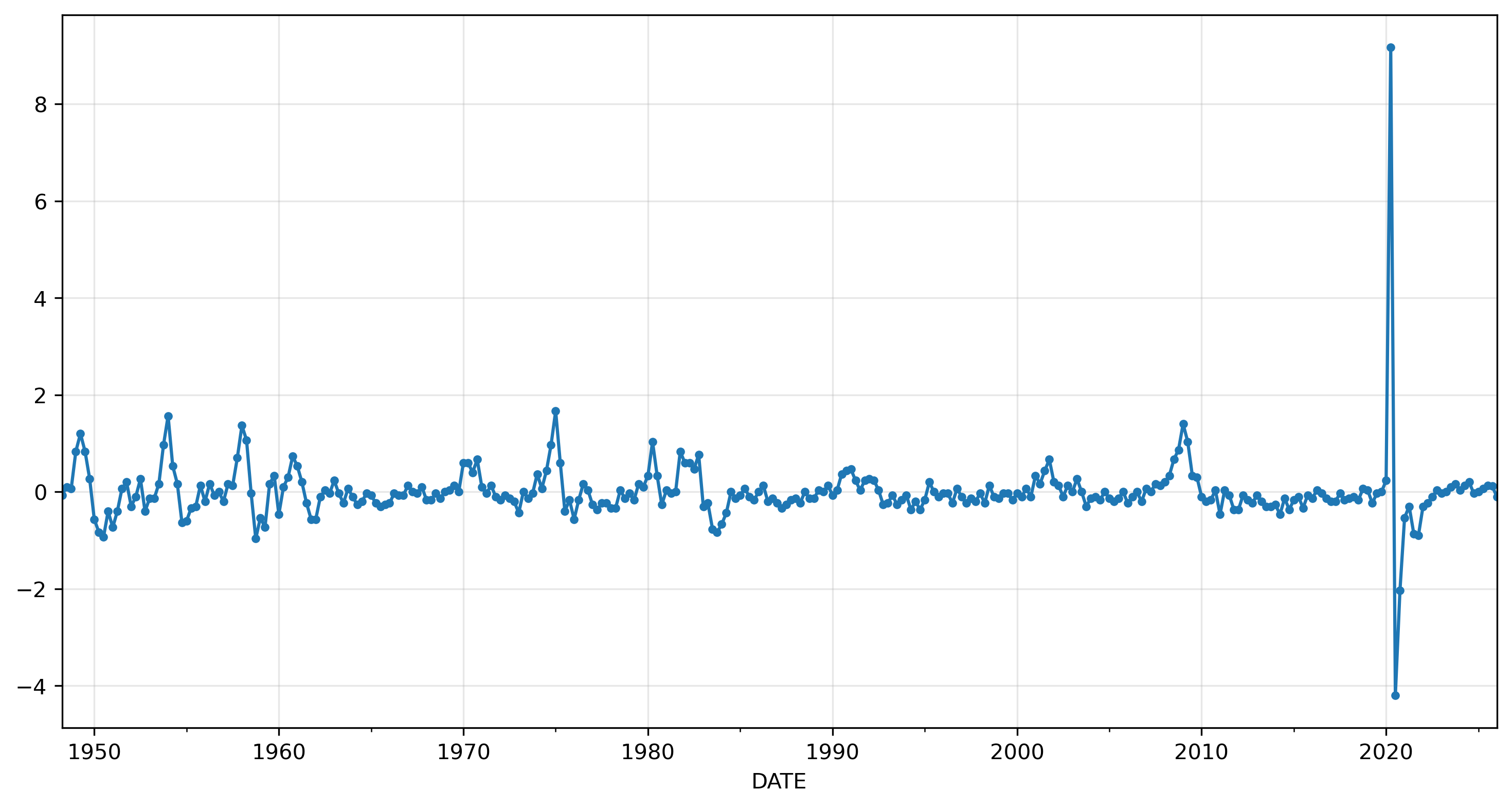

urqd = urq.diff().dropna()

urqd.plot(marker='.', grid=True);

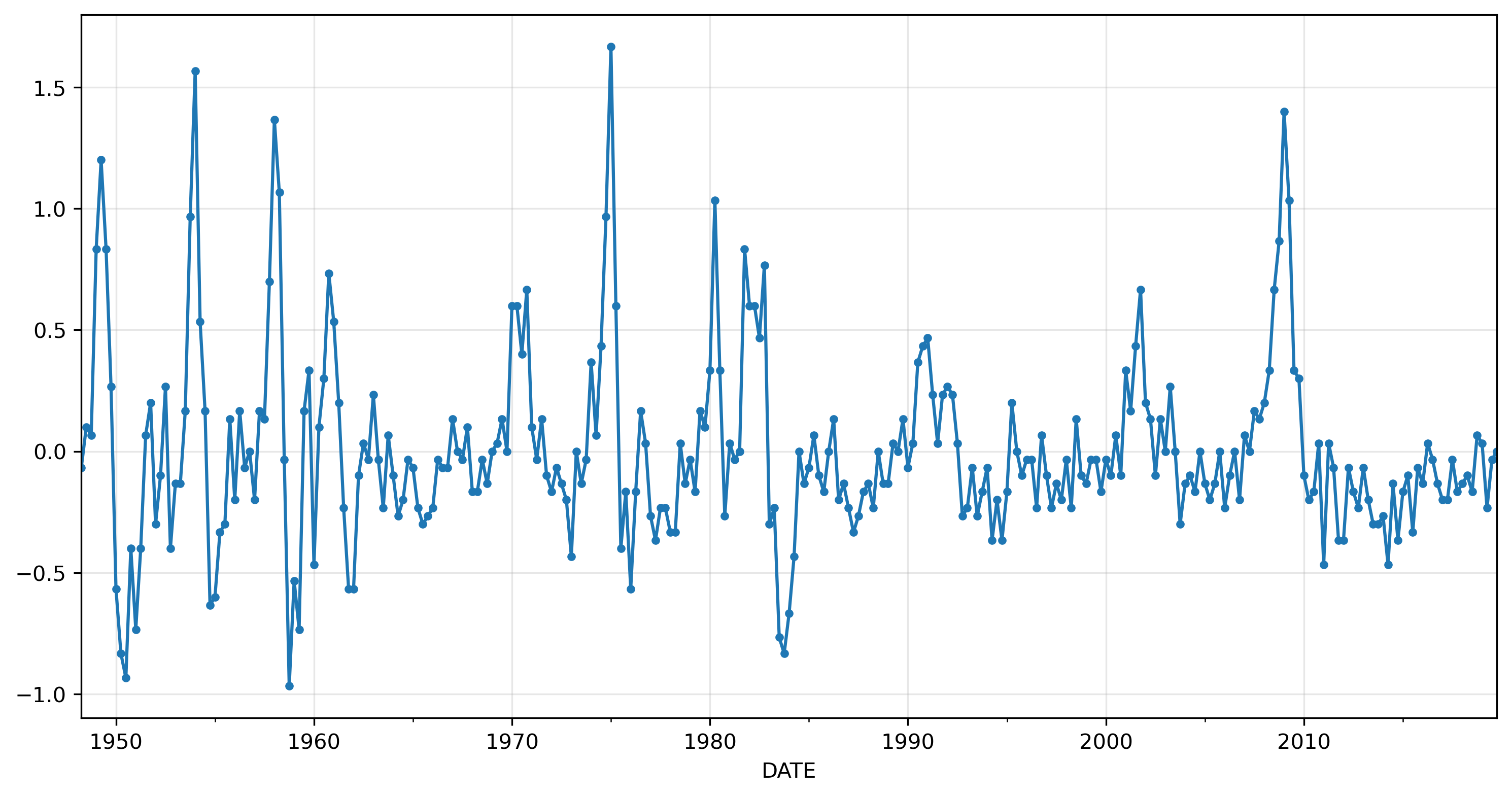

To simplify the analysis, we’ll drop the period at the end of the sample, when the pandemic caused a massive, never-before-seen change in unemployment.

urqd = urqd.loc[:'2019']

urqd.plot(marker='.', grid=True);

Model selection#

modsel = ar_select_order(urqd, maxlag=18, old_names=False)

# pass modsel.aic to pd.Series to get a nice table of AIC values

pd.Series(modsel.aic).round(4)

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13) 54.3214

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12) 54.4209

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14) 55.8434

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17) 57.2608

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18) 57.6978

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15) 57.7964

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16) 59.4825

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11) 61.8631

(1, 2, 3, 4, 5, 6, 7, 8, 9) 63.4146

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10) 65.3997

(1, 2, 3, 4, 5, 6, 7, 8) 71.0780

(1, 2, 3, 4, 5, 6, 7) 77.3457

(1, 2, 3, 4, 5) 77.6608

(1, 2, 3, 4) 78.0792

(1, 2, 3, 4, 5, 6) 78.5765

(1, 2, 3) 79.5936

(1, 2) 81.4666

(1,) 84.6806

0 222.6336

dtype: float64

pd.Series(modsel.bic).round(4)

(1,) 91.8701

(1, 2) 92.2507

(1, 2, 3) 93.9724

(1, 2, 3, 4) 96.0527

(1, 2, 3, 4, 5) 99.2291

(1, 2, 3, 4, 5, 6, 7, 8, 9) 99.3617

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12) 101.1522

(1, 2, 3, 4, 5, 6, 7, 8) 103.4304

(1, 2, 3, 4, 5, 6) 103.7395

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13) 104.6474

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10) 104.9415

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11) 104.9996

(1, 2, 3, 4, 5, 6, 7) 106.1034

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14) 109.7641

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15) 115.3118

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16) 120.5926

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17) 121.9656

(1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18) 125.9974

0 226.2283

dtype: float64

ar_select_order(urqd, maxlag=18, old_names=False, ic='aic').ar_lags

[1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13]

ar_select_order(urqd, maxlag=18, old_names=False, ic='bic').ar_lags

[1]

Using BIC would choose \(p=1\), but AIC indicates \(p=13\).

Comparing these two models using both AIC and BIC suggests \(p=13\) is a good model.

ar1 = AutoReg(urqd, lags=1).fit()

print(ar1.summary())

AutoReg Model Results

==============================================================================

Dep. Variable: UNRATE No. Observations: 287

Model: AutoReg(1) Log Likelihood -51.751

Method: Conditional MLE S.D. of innovations 0.290

Date: Mon, 30 Mar 2026 AIC 109.501

Time: 11:27:01 BIC 120.469

Sample: 09-30-1948 HQIC 113.898

- 12-31-2019

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 6.993e-05 0.017 0.004 0.997 -0.034 0.034

UNRATE.L1 0.6500 0.045 14.466 0.000 0.562 0.738

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 1.5385 +0.0000j 1.5385 0.0000

-----------------------------------------------------------------------------

ar13 = AutoReg(urqd, lags=13).fit()

print(ar13.summary())

AutoReg Model Results

==============================================================================

Dep. Variable: UNRATE No. Observations: 287

Model: AutoReg(13) Log Likelihood -16.418

Method: Conditional MLE S.D. of innovations 0.257

Date: Mon, 30 Mar 2026 AIC 62.836

Time: 11:27:05 BIC 117.033

Sample: 09-30-1951 HQIC 84.590

- 12-31-2019

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0010 0.016 0.061 0.951 -0.029 0.031

UNRATE.L1 0.7109 0.060 11.827 0.000 0.593 0.829

UNRATE.L2 -0.0097 0.072 -0.135 0.893 -0.151 0.132

UNRATE.L3 -0.0635 0.072 -0.881 0.378 -0.205 0.078

UNRATE.L4 -0.2520 0.072 -3.506 0.000 -0.393 -0.111

UNRATE.L5 0.0935 0.072 1.290 0.197 -0.049 0.235

UNRATE.L6 0.1542 0.069 2.220 0.026 0.018 0.290

UNRATE.L7 0.0011 0.070 0.016 0.987 -0.136 0.138

UNRATE.L8 -0.3298 0.069 -4.751 0.000 -0.466 -0.194

UNRATE.L9 0.1800 0.072 2.509 0.012 0.039 0.321

UNRATE.L10 0.0809 0.071 1.136 0.256 -0.059 0.220

UNRATE.L11 -0.0135 0.071 -0.190 0.849 -0.153 0.126

UNRATE.L12 -0.2278 0.071 -3.209 0.001 -0.367 -0.089

UNRATE.L13 0.0949 0.058 1.639 0.101 -0.019 0.208

Roots

==============================================================================

Real Imaginary Modulus Frequency

------------------------------------------------------------------------------

AR.1 -1.0734 -0.3600j 1.1321 -0.4485

AR.2 -1.0734 +0.3600j 1.1321 0.4485

AR.3 -0.8641 -0.8669j 1.2240 -0.3747

AR.4 -0.8641 +0.8669j 1.2240 0.3747

AR.5 -0.3644 -1.0261j 1.0889 -0.3043

AR.6 -0.3644 +1.0261j 1.0889 0.3043

AR.7 0.4348 -1.0201j 1.1089 -0.1859

AR.8 0.4348 +1.0201j 1.1089 0.1859

AR.9 0.8500 -0.7549j 1.1369 -0.1156

AR.10 0.8500 +0.7549j 1.1369 0.1156

AR.11 1.0908 -0.3209j 1.1371 -0.0455

AR.12 1.0908 +0.3209j 1.1371 0.0455

AR.13 2.2514 -0.0000j 2.2514 -0.0000

------------------------------------------------------------------------------

Let’s prune the model to keep only coefficients that are statistically significant.

ar13.tvalues

const 0.061384

UNRATE.L1 11.827093

UNRATE.L2 -0.134720

UNRATE.L3 -0.881150

UNRATE.L4 -3.506309

UNRATE.L5 1.289900

UNRATE.L6 2.220079

UNRATE.L7 0.016272

UNRATE.L8 -4.750995

UNRATE.L9 2.509202

UNRATE.L10 1.136459

UNRATE.L11 -0.190377

UNRATE.L12 -3.208969

UNRATE.L13 1.639165

dtype: float64

# 5% significance level

ar13.tvalues[ar13.tvalues.abs() > 1.96]

UNRATE.L1 11.827093

UNRATE.L4 -3.506309

UNRATE.L6 2.220079

UNRATE.L8 -4.750995

UNRATE.L9 2.509202

UNRATE.L12 -3.208969

dtype: float64

# 1% significance level

ar13.pvalues[ar13.pvalues < 0.01]

UNRATE.L1 2.827644e-32

UNRATE.L4 4.543675e-04

UNRATE.L8 2.024185e-06

UNRATE.L12 1.332118e-03

dtype: float64

ar_v2 = AutoReg(urqd, lags=[1, 4, 8, 12]).fit()

print(ar_v2.summary())

AutoReg Model Results

==============================================================================

Dep. Variable: UNRATE No. Observations: 287

Model: Restr. AutoReg(12) Log Likelihood -29.081

Method: Conditional MLE S.D. of innovations 0.269

Date: Mon, 30 Mar 2026 AIC 70.161

Time: 11:27:09 BIC 91.862

Sample: 06-30-1951 HQIC 78.870

- 12-31-2019

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0004 0.016 0.025 0.980 -0.031 0.032

UNRATE.L1 0.6276 0.045 14.010 0.000 0.540 0.715

UNRATE.L4 -0.1772 0.044 -3.987 0.000 -0.264 -0.090

UNRATE.L8 -0.1174 0.043 -2.733 0.006 -0.202 -0.033

UNRATE.L12 -0.1222 0.043 -2.856 0.004 -0.206 -0.038

Roots

==============================================================================

Real Imaginary Modulus Frequency

------------------------------------------------------------------------------

AR.1 1.0301 -0.3268j 1.0807 -0.0489

AR.2 1.0301 +0.3268j 1.0807 0.0489

AR.3 0.8843 -0.7578j 1.1645 -0.1128

AR.4 0.8843 +0.7578j 1.1645 0.1128

AR.5 0.4442 -1.1222j 1.2069 -0.1900

AR.6 0.4442 +1.1222j 1.2069 0.1900

AR.7 -0.3140 -1.1605j 1.2023 -0.2921

AR.8 -0.3140 +1.1605j 1.2023 0.2921

AR.9 -1.1815 -0.3878j 1.2435 -0.4495

AR.10 -1.1815 +0.3878j 1.2435 0.4495

AR.11 -0.8630 -0.9177j 1.2597 -0.3701

AR.12 -0.8630 +0.9177j 1.2597 0.3701

------------------------------------------------------------------------------

print(AutoReg(urqd, lags=[1, 4, 6, 8, 9, 12], trend='n').fit().summary())

AutoReg Model Results

==============================================================================

Dep. Variable: UNRATE No. Observations: 287

Model: Restr. AutoReg(12) Log Likelihood -19.055

Method: Conditional MLE S.D. of innovations 0.259

Date: Mon, 30 Mar 2026 AIC 52.110

Time: 11:27:10 BIC 77.427

Sample: 06-30-1951 HQIC 62.270

- 12-31-2019

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

UNRATE.L1 0.6668 0.044 15.141 0.000 0.580 0.753

UNRATE.L4 -0.2399 0.047 -5.126 0.000 -0.332 -0.148

UNRATE.L6 0.1848 0.049 3.745 0.000 0.088 0.282

UNRATE.L8 -0.3058 0.061 -5.047 0.000 -0.425 -0.187

UNRATE.L9 0.1861 0.056 3.323 0.001 0.076 0.296

UNRATE.L12 -0.1472 0.042 -3.512 0.000 -0.229 -0.065

Roots

==============================================================================

Real Imaginary Modulus Frequency

------------------------------------------------------------------------------

AR.1 1.0569 -0.2923j 1.0966 -0.0429

AR.2 1.0569 +0.2923j 1.0966 0.0429

AR.3 0.8633 -0.7253j 1.1275 -0.1112

AR.4 0.8633 +0.7253j 1.1275 0.1112

AR.5 0.4598 -1.0438j 1.1406 -0.1840

AR.6 0.4598 +1.0438j 1.1406 0.1840

AR.7 -1.0861 -0.3895j 1.1538 -0.4452

AR.8 -1.0861 +0.3895j 1.1538 0.4452

AR.9 -0.4159 -1.0497j 1.1290 -0.3100

AR.10 -0.4159 +1.0497j 1.1290 0.3100

AR.11 -0.8780 -1.1148j 1.4190 -0.3562

AR.12 -0.8780 +1.1148j 1.4190 0.3562

------------------------------------------------------------------------------

Using glob=True performs a global search over all \(2^{12}=4096\) possible models. Clearly trying all possible models for a large number of lags would eventually become infeasible; using 20 lags requires testing over 1 million models, for example.

sel = ar_select_order(urqd, 12, old_names=False, glob=True)

sel.ar_lags

[1, 4, 6, 8, 9, 12]

Residuals#

The standardized residuals are calculated by scaling the residuals from their estimated standard deviation, \(\epsilon_t / \sigma.\)

std_resid = ar_v2.resid / np.sqrt(ar_v2.sigma2)

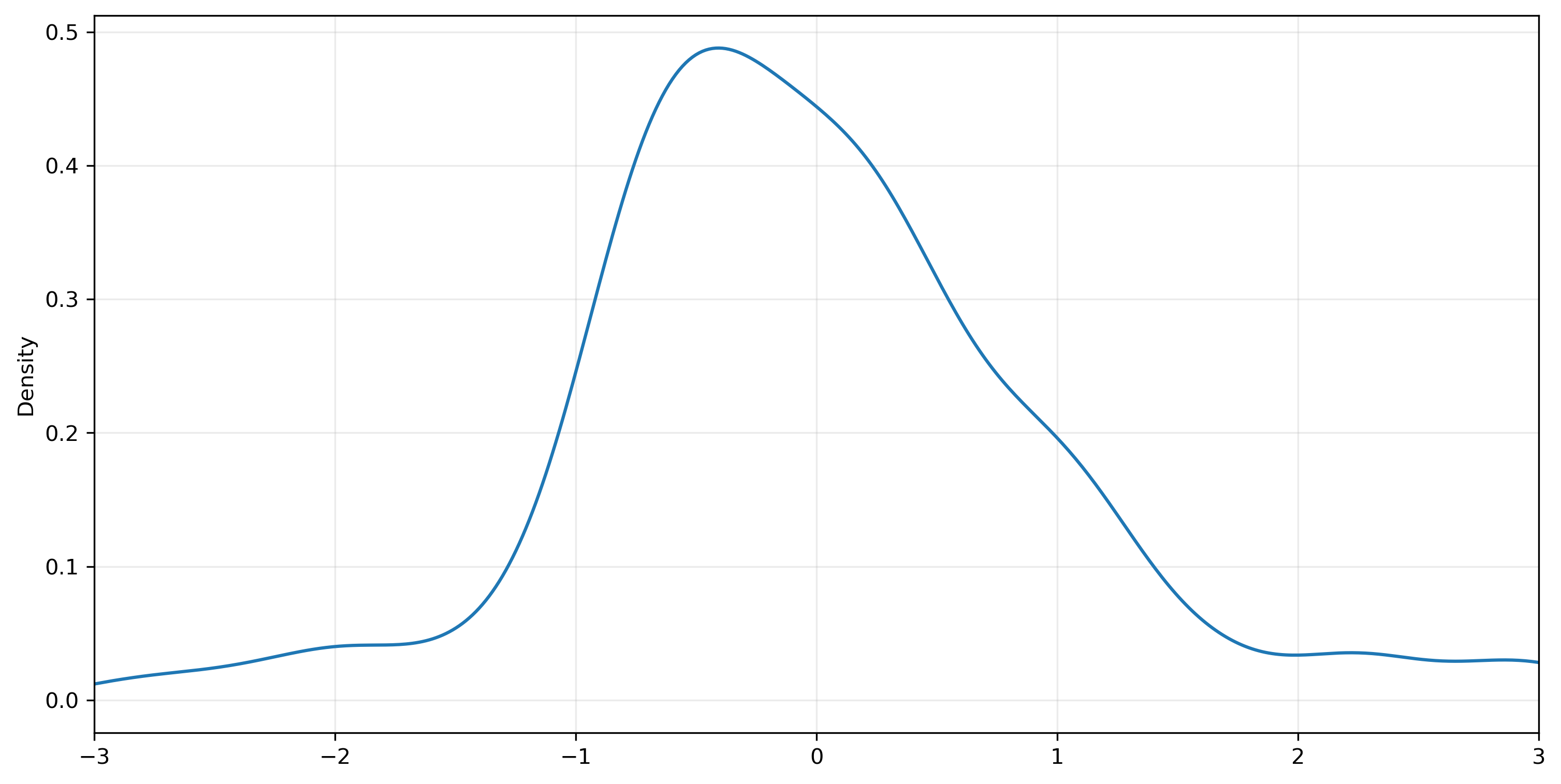

We can use kernel density estimation to get an empirical estimate of the PDF.

ax = std_resid.plot.kde(xlim=(-3,3), bw_method=0.25)

ax.grid(alpha=0.25)

std_resid.skew(), std_resid.kurtosis()

(0.5712214353027926, 1.8777501533375105)

There are several statistical tests we can use to test the null hypothesis that data are drawn from a normal distribution. Two that are available in scipy are due to D’Agostino and Pearson (1973) and the Shapiro and Wilk (1965). The former combines information about the skewness and kurtosis of a series; the latter is a more complicated test that uses information about order statistics.

from scipy.stats import normaltest, shapiro

normaltest(std_resid)

NormaltestResult(statistic=28.285962906502313, pvalue=7.207442680254298e-07)

shapiro(std_resid)

ShapiroResult(statistic=0.958171619651281, pvalue=4.0510448979408166e-07)

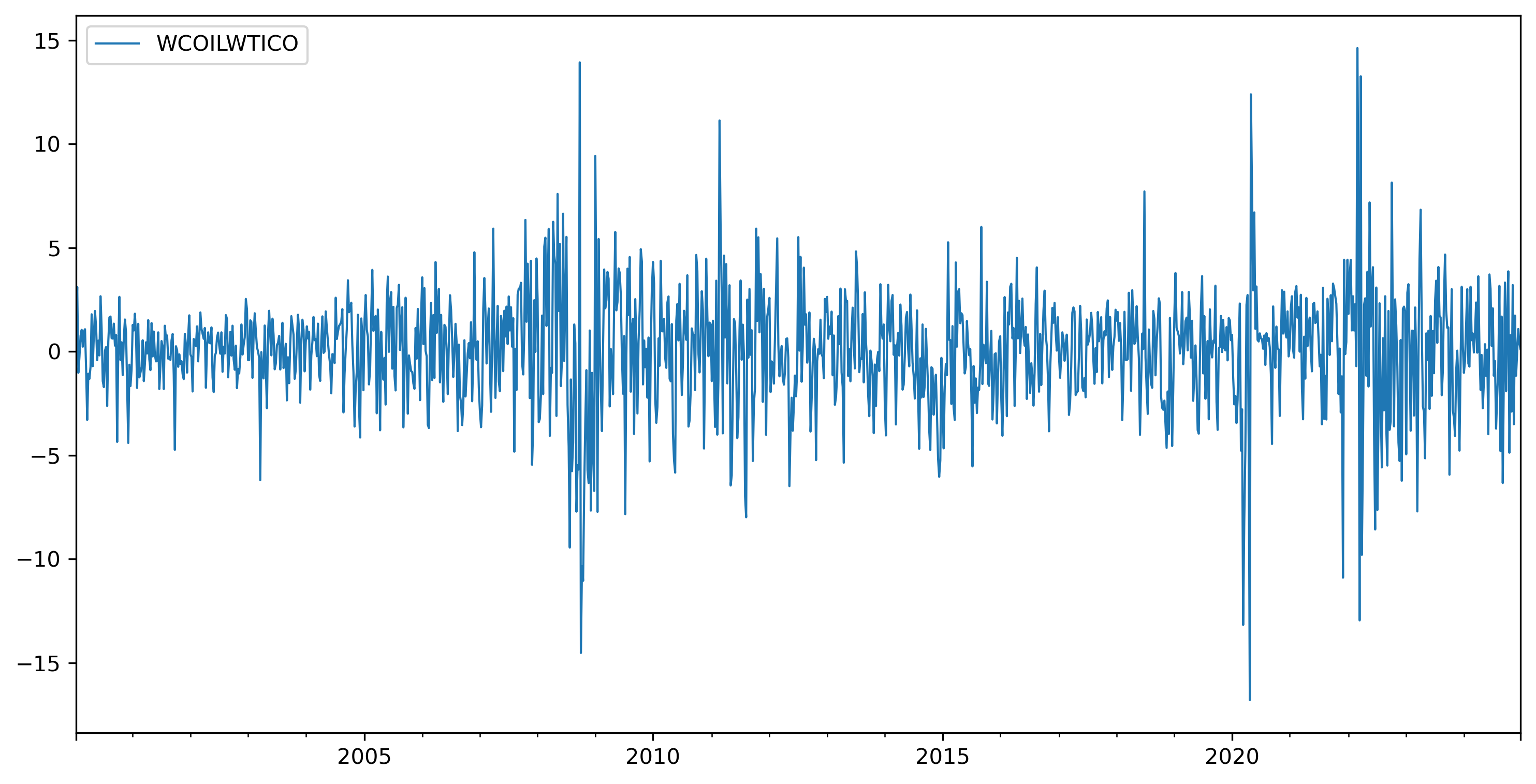

Oil prices#

Next we’ll use the Crude Oil Price series for West Texas Intermediate at Cushing, Oklahoma (WTI), available from FRED.

oil = pdr.get_data_fred('WCOILWTICO', 2000, 2025)

oil.index

DatetimeIndex(['2000-01-07', '2000-01-14', '2000-01-21', '2000-01-28',

'2000-02-04', '2000-02-11', '2000-02-18', '2000-02-25',

'2000-03-03', '2000-03-10',

...

'2024-10-25', '2024-11-01', '2024-11-08', '2024-11-15',

'2024-11-22', '2024-11-29', '2024-12-06', '2024-12-13',

'2024-12-20', '2024-12-27'],

dtype='datetime64[ns]', name='DATE', length=1304, freq=None)

# specify a frequency for the series

oil.index = pd.DatetimeIndex(oil.index, freq='W-FRI')

ax = oil.plot(xlabel='')

ax.grid(alpha=0.3)

oild = oil.diff().dropna()

oild.plot(lw=1, xlabel='');

ar_select_order(oild, maxlag=18, old_names=False, ic='aic').ar_lags

[1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17]

ar = AutoReg(oild, lags=17, old_names=False).fit()

print(ar.summary())

AutoReg Model Results

==============================================================================

Dep. Variable: WCOILWTICO No. Observations: 1303

Model: AutoReg(17) Log Likelihood -3096.451

Method: Conditional MLE S.D. of innovations 2.688

Date: Mon, 30 Mar 2026 AIC 6230.902

Time: 12:10:56 BIC 6328.929

Sample: 05-12-2000 HQIC 6267.702

- 12-27-2024

==================================================================================

coef std err z P>|z| [0.025 0.975]

----------------------------------------------------------------------------------

const 0.0246 0.075 0.329 0.743 -0.122 0.172

WCOILWTICO.L1 0.1428 0.028 5.128 0.000 0.088 0.197

WCOILWTICO.L2 -0.0012 0.028 -0.043 0.965 -0.056 0.054

WCOILWTICO.L3 0.0630 0.028 2.248 0.025 0.008 0.118

WCOILWTICO.L4 -0.0087 0.028 -0.308 0.758 -0.064 0.046

WCOILWTICO.L5 0.0439 0.028 1.569 0.117 -0.011 0.099

WCOILWTICO.L6 0.0337 0.028 1.200 0.230 -0.021 0.089

WCOILWTICO.L7 -0.0216 0.028 -0.770 0.441 -0.077 0.033

WCOILWTICO.L8 0.1108 0.028 3.942 0.000 0.056 0.166

WCOILWTICO.L9 -0.0605 0.028 -2.140 0.032 -0.116 -0.005

WCOILWTICO.L10 0.0056 0.028 0.199 0.842 -0.050 0.061

WCOILWTICO.L11 -0.0049 0.028 -0.173 0.862 -0.060 0.050

WCOILWTICO.L12 0.0184 0.028 0.654 0.513 -0.037 0.074

WCOILWTICO.L13 -0.0640 0.028 -2.272 0.023 -0.119 -0.009

WCOILWTICO.L14 0.0492 0.028 1.744 0.081 -0.006 0.105

WCOILWTICO.L15 -0.0174 0.028 -0.616 0.538 -0.073 0.038

WCOILWTICO.L16 -0.0737 0.028 -2.613 0.009 -0.129 -0.018

WCOILWTICO.L17 0.0593 0.028 2.116 0.034 0.004 0.114

Roots

==============================================================================

Real Imaginary Modulus Frequency

------------------------------------------------------------------------------

AR.1 -1.1847 -0.1382j 1.1927 -0.4815

AR.2 -1.1847 +0.1382j 1.1927 0.4815

AR.3 -0.9510 -0.6157j 1.1329 -0.4086

AR.4 -0.9510 +0.6157j 1.1329 0.4086

AR.5 -0.6576 -0.8816j 1.0998 -0.3520

AR.6 -0.6576 +0.8816j 1.0998 0.3520

AR.7 -0.2201 -1.1087j 1.1303 -0.2812

AR.8 -0.2201 +1.1087j 1.1303 0.2812

AR.9 0.1814 -1.1568j 1.1709 -0.2252

AR.10 0.1814 +1.1568j 1.1709 0.2252

AR.11 0.6172 -1.0118j 1.1852 -0.1628

AR.12 0.6172 +1.0118j 1.1852 0.1628

AR.13 0.9385 -0.7602j 1.2078 -0.1084

AR.14 0.9385 +0.7602j 1.2078 0.1084

AR.15 1.2165 -0.2853j 1.2495 -0.0367

AR.16 1.2165 +0.2853j 1.2495 0.0367

AR.17 1.3631 -0.0000j 1.3631 -0.0000

------------------------------------------------------------------------------

# 1% significance level

ar.tvalues[ar.tvalues.abs() > 2.326]

WCOILWTICO.L1 5.128402

WCOILWTICO.L8 3.942358

WCOILWTICO.L16 -2.613228

dtype: float64

ar_b = AutoReg(oild, lags=[1,8,16], old_names=False).fit()

print(ar_b.summary())

AutoReg Model Results

==============================================================================

Dep. Variable: WCOILWTICO No. Observations: 1303

Model: Restr. AutoReg(16) Log Likelihood -3111.642

Method: Conditional MLE S.D. of innovations 2.715

Date: Mon, 30 Mar 2026 AIC 6233.284

Time: 12:12:39 BIC 6259.085

Sample: 05-05-2000 HQIC 6242.970

- 12-27-2024

==================================================================================

coef std err z P>|z| [0.025 0.975]

----------------------------------------------------------------------------------

const 0.0296 0.076 0.392 0.695 -0.119 0.178

WCOILWTICO.L1 0.1317 0.027 4.803 0.000 0.078 0.185

WCOILWTICO.L8 0.1056 0.028 3.829 0.000 0.052 0.160

WCOILWTICO.L16 -0.0735 0.028 -2.659 0.008 -0.128 -0.019

Roots

==============================================================================

Real Imaginary Modulus Frequency

------------------------------------------------------------------------------

AR.1 1.1493 -0.1948j 1.1657 -0.0267

AR.2 1.1493 +0.1948j 1.1657 0.0267

AR.3 0.9566 -0.6670j 1.1662 -0.0969

AR.4 0.9566 +0.6670j 1.1662 0.0969

AR.5 0.6846 -0.9526j 1.1730 -0.1508

AR.6 0.6846 +0.9526j 1.1730 0.1508

AR.7 0.2118 -1.1545j 1.1737 -0.2211

AR.8 0.2118 +1.1545j 1.1737 0.2211

AR.9 -0.1919 -1.1663j 1.1820 -0.2760

AR.10 -0.1919 +1.1663j 1.1820 0.2760

AR.11 -0.6725 -0.9724j 1.1823 -0.3463

AR.12 -0.6725 +0.9724j 1.1823 0.3463

AR.13 -0.9684 -0.6871j 1.1874 -0.4018

AR.14 -0.9684 +0.6871j 1.1874 0.4018

AR.15 -1.1693 -0.2068j 1.1875 -0.4721

AR.16 -1.1693 +0.2068j 1.1875 0.4721

------------------------------------------------------------------------------

std_resid = ar_b.resid / np.sqrt(ar_b.sigma2)

std_resid.skew(), std_resid.kurtosis()

(-0.2535073744148516, 5.4491566084082415)

normaltest(std_resid)

NormaltestResult(statistic=171.8329216954173, pvalue=4.863569756405212e-38)

Housing starts#

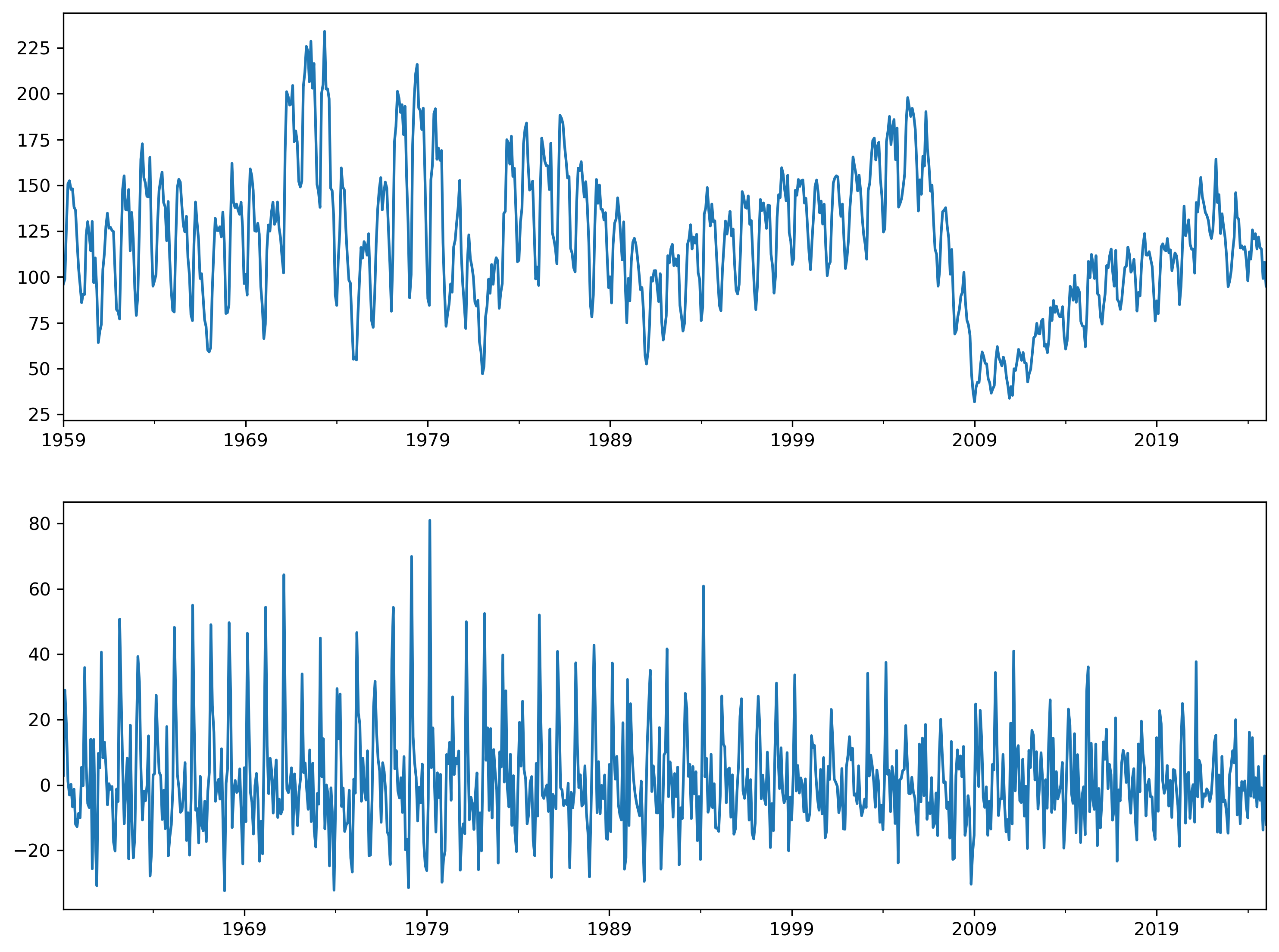

Next we’ll examine housing starts using the series Housing Starts: Total: New Privately Owned Housing Units Started (HOUSTNSA).

hstarts = pdr.get_data_fred('HOUSTNSA', 1959, 2025).asfreq('MS').squeeze()

sel = ar_select_order(hstartsd, 24, old_names=False)

# fit selected model

res = sel.model.fit()

print(res.summary())

AutoReg Model Results

==============================================================================

Dep. Variable: HOUSTNSA No. Observations: 792

Model: AutoReg(24) Log Likelihood -2848.436

Method: Conditional MLE S.D. of innovations 9.875

Date: Mon, 30 Mar 2026 AIC 5748.872

Time: 12:15:21 BIC 5869.610

Sample: 02-01-1961 HQIC 5795.343

- 01-01-2025

================================================================================

coef std err z P>|z| [0.025 0.975]

--------------------------------------------------------------------------------

const 1.5393 0.461 3.341 0.001 0.636 2.442

HOUSTNSA.L1 -0.2832 0.035 -8.062 0.000 -0.352 -0.214

HOUSTNSA.L2 -0.1187 0.036 -3.254 0.001 -0.190 -0.047

HOUSTNSA.L3 -0.0450 0.037 -1.225 0.220 -0.117 0.027

HOUSTNSA.L4 -0.0753 0.037 -2.057 0.040 -0.147 -0.004

HOUSTNSA.L5 -0.0107 0.036 -0.293 0.769 -0.082 0.061

HOUSTNSA.L6 -0.0470 0.036 -1.289 0.197 -0.119 0.024

HOUSTNSA.L7 -0.0481 0.036 -1.321 0.186 -0.119 0.023

HOUSTNSA.L8 -0.0775 0.036 -2.130 0.033 -0.149 -0.006

HOUSTNSA.L9 -0.0279 0.036 -0.769 0.442 -0.099 0.043

HOUSTNSA.L10 -0.1118 0.036 -3.087 0.002 -0.183 -0.041

HOUSTNSA.L11 0.0277 0.036 0.762 0.446 -0.044 0.099

HOUSTNSA.L12 0.3472 0.035 9.879 0.000 0.278 0.416

HOUSTNSA.L13 0.2475 0.035 7.042 0.000 0.179 0.316

HOUSTNSA.L14 0.0466 0.036 1.287 0.198 -0.024 0.118

HOUSTNSA.L15 -0.0273 0.036 -0.757 0.449 -0.098 0.043

HOUSTNSA.L16 -0.1371 0.036 -3.803 0.000 -0.208 -0.066

HOUSTNSA.L17 -0.0259 0.036 -0.714 0.475 -0.097 0.045

HOUSTNSA.L18 -0.0848 0.036 -2.340 0.019 -0.156 -0.014

HOUSTNSA.L19 0.0015 0.036 0.042 0.966 -0.070 0.073

HOUSTNSA.L20 -0.0930 0.036 -2.559 0.010 -0.164 -0.022

HOUSTNSA.L21 -0.0929 0.036 -2.553 0.011 -0.164 -0.022

HOUSTNSA.L22 -0.0094 0.037 -0.258 0.797 -0.081 0.062

HOUSTNSA.L23 0.0607 0.036 1.675 0.094 -0.010 0.132

HOUSTNSA.L24 0.2272 0.035 6.525 0.000 0.159 0.295

Roots

==============================================================================

Real Imaginary Modulus Frequency

------------------------------------------------------------------------------

AR.1 -1.1039 -0.0000j 1.1039 -0.5000

AR.2 -1.0266 -0.2516j 1.0570 -0.4617

AR.3 -1.0266 +0.2516j 1.0570 0.4617

AR.4 -0.8897 -0.5143j 1.0276 -0.4166

AR.5 -0.8897 +0.5143j 1.0276 0.4166

AR.6 -0.7635 -0.7742j 1.0874 -0.3739

AR.7 -0.7635 +0.7742j 1.0874 0.3739

AR.8 -0.5372 -0.9002j 1.0483 -0.3356

AR.9 -0.5372 +0.9002j 1.0483 0.3356

AR.10 -0.3285 -1.0522j 1.1023 -0.2982

AR.11 -0.3285 +1.0522j 1.1023 0.2982

AR.12 -0.0143 -1.0421j 1.0422 -0.2522

AR.13 -0.0143 +1.0421j 1.0422 0.2522

AR.14 0.2139 -1.0530j 1.0745 -0.2181

AR.15 0.2139 +1.0530j 1.0745 0.2181

AR.16 0.5019 -0.8717j 1.0059 -0.1669

AR.17 0.5019 +0.8717j 1.0059 0.1669

AR.18 0.7584 -0.8062j 1.1068 -0.1299

AR.19 0.7584 +0.8062j 1.1068 0.1299

AR.20 0.8700 -0.5015j 1.0042 -0.0832

AR.21 0.8700 +0.5015j 1.0042 0.0832

AR.22 1.0827 -0.2575j 1.1129 -0.0372

AR.23 1.0827 +0.2575j 1.1129 0.0372

AR.24 1.1026 -0.0000j 1.1026 -0.0000

------------------------------------------------------------------------------

Removing seasonality#

By allowing each month of the year to have its own intercept — or “dummy variable” — we can remove the seasonal variation in the series.

hstartsd.groupby(hstartsd.index.month).mean()

DATE

1 -4.269131

2 4.160395

3 31.359965

4 13.224910

5 4.059291

6 0.538924

7 -3.537971

8 -1.794444

9 -4.022403

10 2.524579

11 -15.054469

12 -13.934532

Name: HOUSTNSA, dtype: float64

When estimating an autoregression or running order selection, we can include seasonal dummies. Here’s we’ll exclude the main intercept and instead have 12 dummies (one for each month).

sel = ar_select_order(hstartsd, 24, seasonal=True, trend='n', old_names=False)

sel.ar_lags

[1]

The initial data begin in January, but when we difference the data we end up with a series that starts in February. Therefore, the s(1,12) coefficient is automatically defined as the February dummy.

res = sel.model.fit()

print(res.summary())

AutoReg Model Results

==============================================================================

Dep. Variable: HOUSTNSA No. Observations: 792

Model: Seas. AutoReg(1) Log Likelihood -2932.672

Method: Conditional MLE S.D. of innovations 9.861

Date: Mon, 30 Mar 2026 AIC 5893.345

Time: 12:15:36 BIC 5958.771

Sample: 03-01-1959 HQIC 5918.492

- 01-01-2025

===============================================================================

coef std err z P>|z| [0.025 0.975]

-------------------------------------------------------------------------------

s(1,12) 3.2422 1.232 2.633 0.008 0.828 5.656

s(2,12) 32.2999 1.222 26.424 0.000 29.904 34.696

s(3,12) 20.3096 1.629 12.466 0.000 17.117 23.503

s(4,12) 7.0470 1.297 5.431 0.000 4.504 9.590

s(5,12) 1.4560 1.222 1.192 0.233 -0.939 3.851

s(6,12) -3.4162 1.214 -2.814 0.005 -5.796 -1.037

s(7,12) -2.5937 1.220 -2.126 0.034 -4.985 -0.203

s(8,12) -4.4278 1.215 -3.643 0.000 -6.810 -2.046

s(9,12) 1.6159 1.222 1.323 0.186 -0.779 4.011

s(10,12) -14.4841 1.217 -11.902 0.000 -16.869 -12.099

s(11,12) -17.3356 1.321 -13.121 0.000 -19.925 -14.746

s(12,12) -7.4172 1.306 -5.678 0.000 -9.978 -4.857

HOUSTNSA.L1 -0.2259 0.035 -6.520 0.000 -0.294 -0.158

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 -4.4264 +0.0000j 4.4264 0.5000

-----------------------------------------------------------------------------

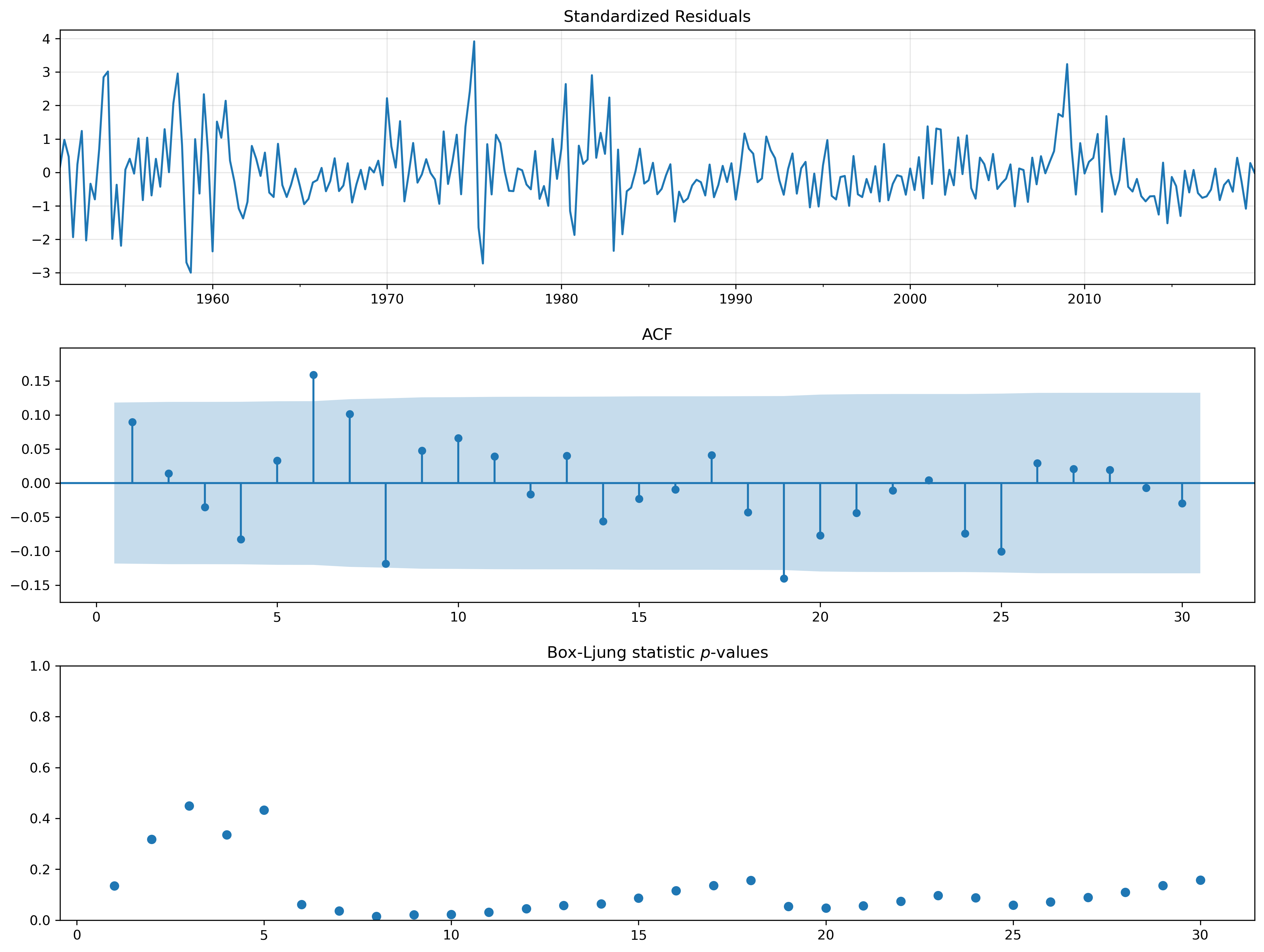

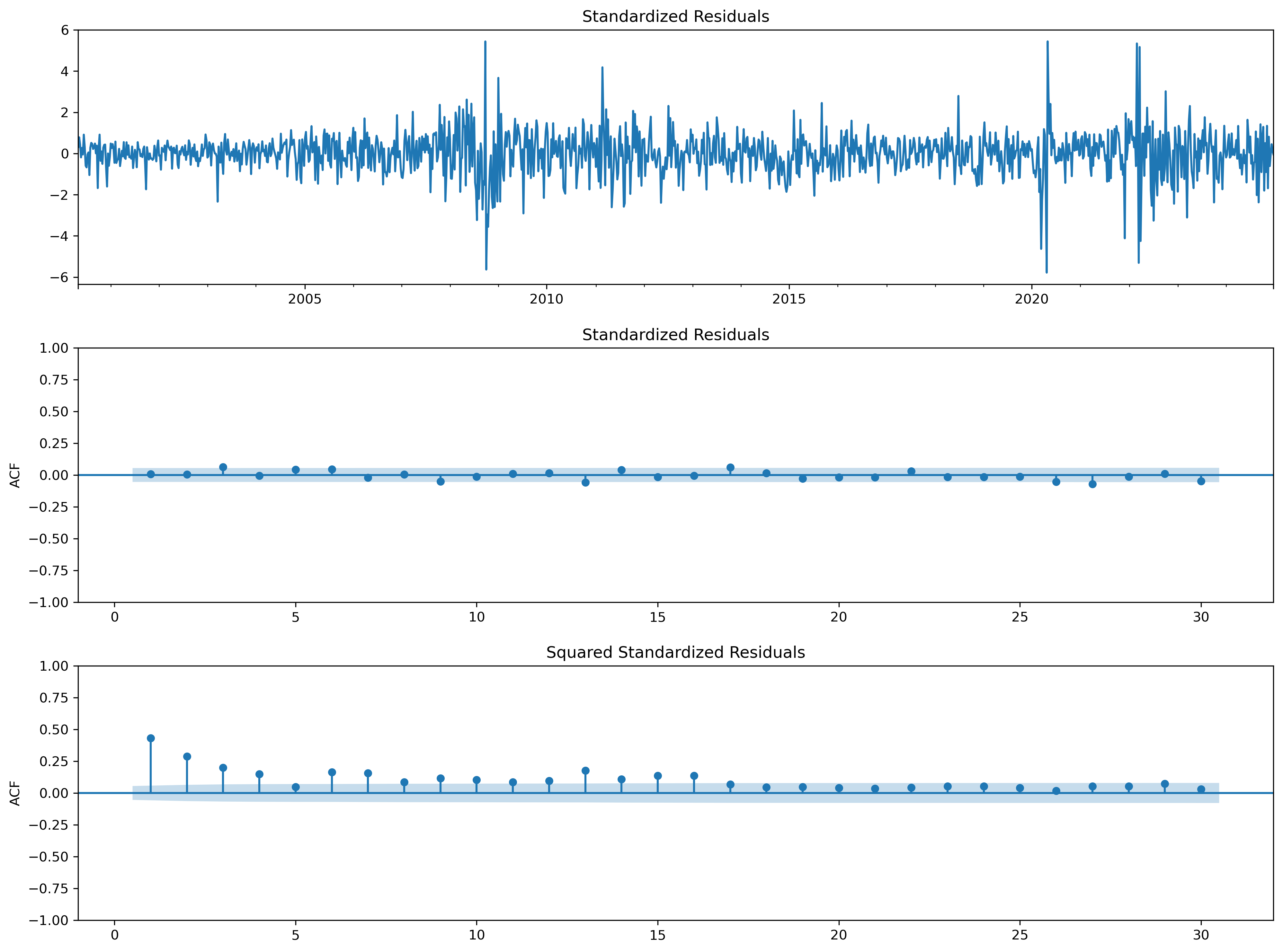

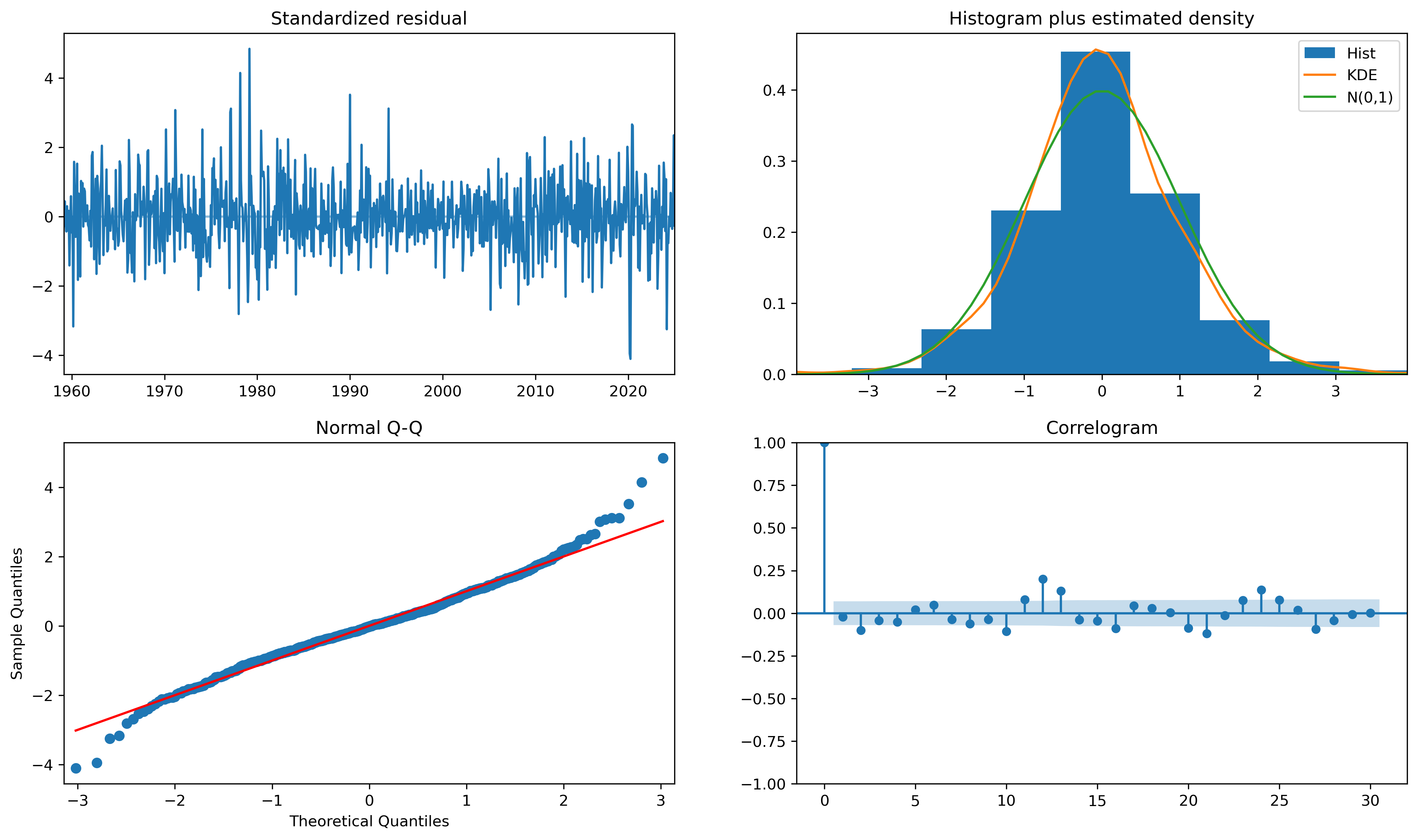

fig = plt.figure(figsize=(16,9))

fig = res.plot_diagnostics(fig=fig, lags=30)

Inflation#

Consumer Price Index for All Urban Consumers: All Items in U.S. City Average (CPIAUCNS)

cpi = pdr.get_data_fred('CPIAUCNS', start=1970).squeeze()

cpi.index = pd.DatetimeIndex(cpi.index, freq='MS')

cpi.tail(10)

DATE

2025-05-01 321.465

2025-06-01 322.561

2025-07-01 323.048

2025-08-01 323.976

2025-09-01 324.800

2025-10-01 NaN

2025-11-01 324.122

2025-12-01 324.054

2026-01-01 325.252

2026-02-01 326.785

Freq: MS, Name: CPIAUCNS, dtype: float64

# calculating an annualized inflation rate in percent

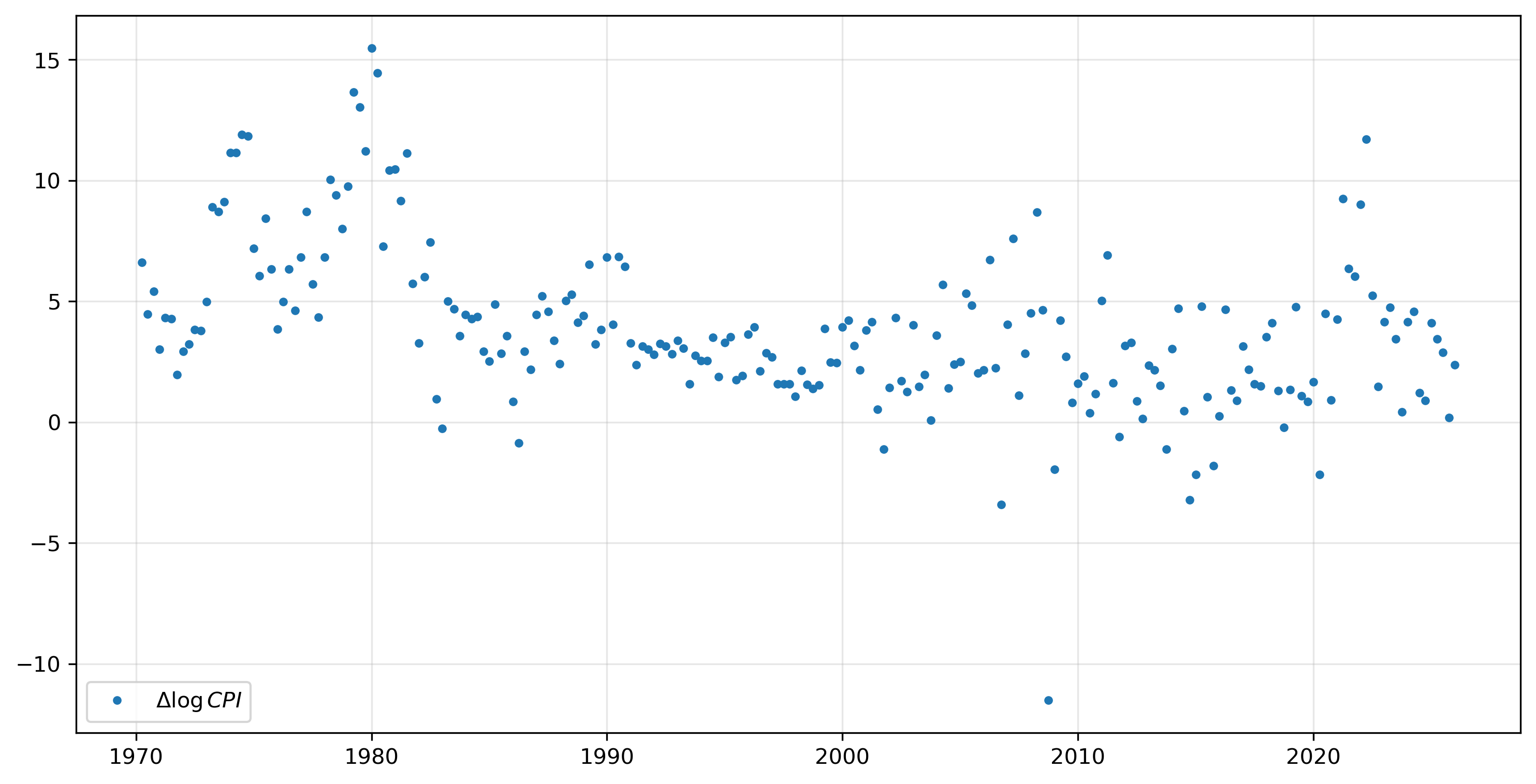

inf = np.log(cpi).resample('QS').mean().diff()[1:] * 400

inf.tail(10)

DATE

2023-10-01 0.419097

2024-01-01 4.143722

2024-04-01 4.582997

2024-07-01 1.206464

2024-10-01 0.898997

2025-01-01 4.113436

2025-04-01 3.443490

2025-07-01 2.892898

2025-10-01 0.182036

2026-01-01 2.374514

Freq: QS-JAN, Name: CPIAUCNS, dtype: float64

Another flexible model for estimation are seasonal autoregressive integrated moving average models, or SARIMAX. These models are a class of state space models,

Here, we observe the time series \(y_t\), but it depends on the state variable, \(\alpha_{t}\), which is unobservable. The \(\varepsilon\) and \(\eta\) terms are both noise processes. (Uppercase letters denote matrices, while lowercase letters are vectors.) The first equation is called the observation equation while the second set of equations are the state equations.

This class of models nests ARMA models as well as other types of models. For example, we can write the ARMA(1,1) model

as a state-space model:

To see this, note that the observation equation says

which implies that

The two state equations imply that

and

Substituting these into (15), we get

which is the desired ARMA(1,1) model.

The following examples are based on those of Chad Fulton, an economist at the Federal Reserve.

# Estimate ARMA(1,1) model with SARIMAX

inf_model2 = sm.tsa.SARIMAX(inf, order=(1, 0, 1))

inf_results2 = inf_model2.fit()

print(inf_results2.summary())

RUNNING THE L-BFGS-B CODE

* * *

Machine precision = 2.220D-16

N = 3 M = 10

At X0 0 variables are exactly at the bounds

At iterate 0 f= 2.40150D+00 |proj g|= 1.02415D-01

At iterate 5 f= 2.36720D+00 |proj g|= 6.26196D-02

At iterate 10 f= 2.35807D+00 |proj g|= 1.00190D-03

At iterate 15 f= 2.35804D+00 |proj g|= 1.58860D-06

* * *

Tit = total number of iterations

Tnf = total number of function evaluations

Tnint = total number of segments explored during Cauchy searches

Skip = number of BFGS updates skipped

Nact = number of active bounds at final generalized Cauchy point

Projg = norm of the final projected gradient

F = final function value

* * *

N Tit Tnf Tnint Skip Nact Projg F

3 15 17 1 0 0 1.589D-06 2.358D+00

F = 2.3580439428985573

CONVERGENCE: NORM_OF_PROJECTED_GRADIENT_<=_PGTOL

SARIMAX Results

==============================================================================

Dep. Variable: CPIAUCNS No. Observations: 224

Model: SARIMAX(1, 0, 1) Log Likelihood -528.202

Date: Mon, 30 Mar 2026 AIC 1062.404

Time: 12:17:59 BIC 1072.639

Sample: 04-01-1970 HQIC 1066.535

- 01-01-2026

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ar.L1 0.9771 0.015 64.390 0.000 0.947 1.007

ma.L1 -0.6176 0.056 -11.014 0.000 -0.727 -0.508

sigma2 6.4916 0.317 20.457 0.000 5.870 7.114

===================================================================================

Ljung-Box (L1) (Q): 4.32 Jarque-Bera (JB): 558.70

Prob(Q): 0.04 Prob(JB): 0.00

Heteroskedasticity (H): 1.82 Skew: -1.17

Prob(H) (two-sided): 0.01 Kurtosis: 10.37

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

This problem is unconstrained.

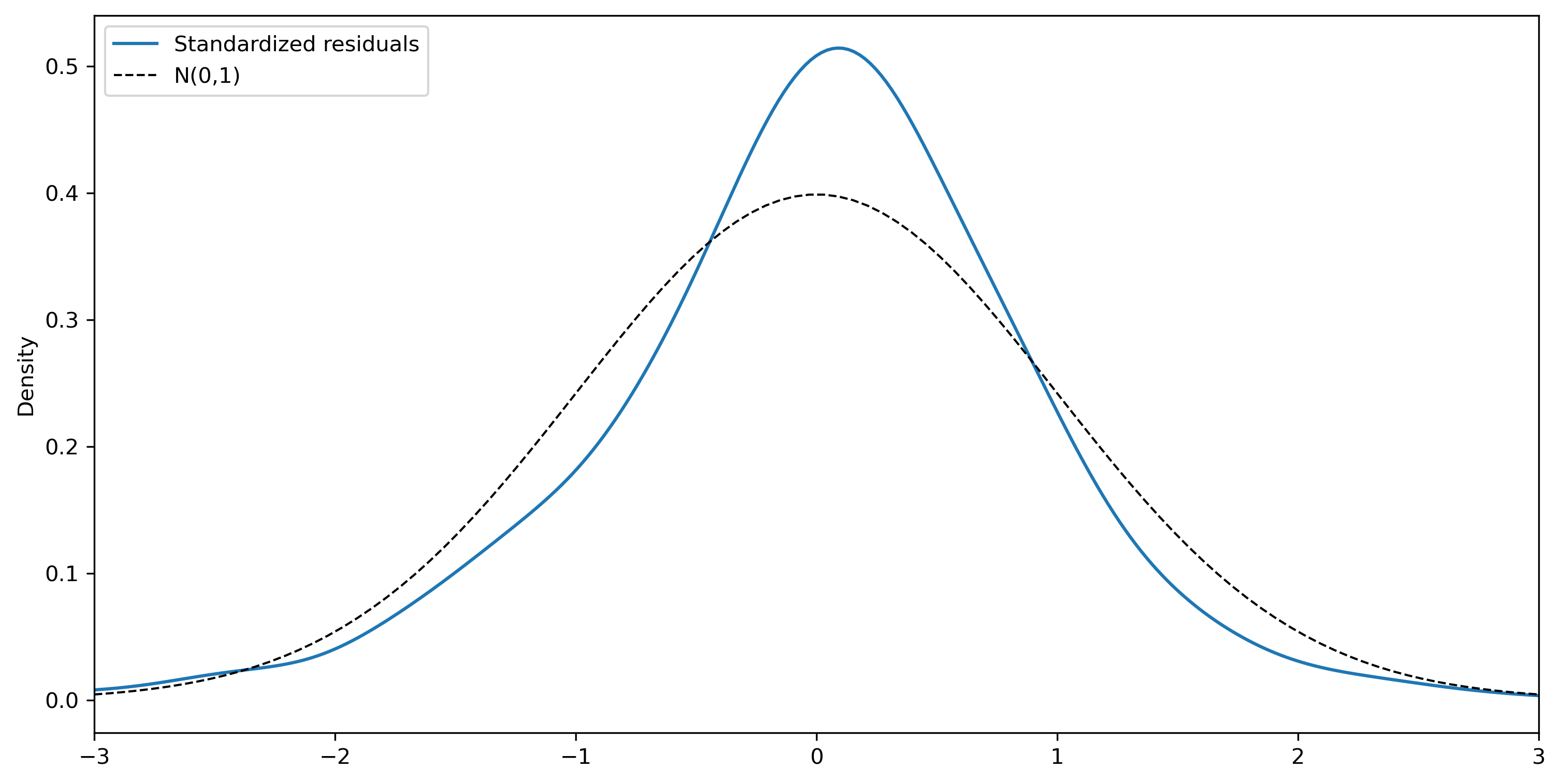

Notice that the observation from October 2008 is quite different from all the other data. This outlier might be having a out-sized impact on our results, so we can remove its effect by letting it have its own intercept. We do this by including an additional exogenous variable in the regression using the exog argument; in this case the variable is a vector that is zero for every observation except the one for October 2008.

outlier = pd.Series(np.zeros(len(inf)), index=inf.index, name='outlier')

outlier['2008-10-01'] = 1

inf_model3 = sm.tsa.SARIMAX(inf, order=(1, 0, 1), exog=outlier)

inf_results3 = inf_model3.fit()

print(inf_results3.summary())

RUNNING THE L-BFGS-B CODE

* * *

Machine precision = 2.220D-16

N = 4 M = 10

At X0 0 variables are exactly at the bounds

At iterate 0 f= 2.30107D+00 |proj g|= 1.14907D-01

At iterate 5 f= 2.26805D+00 |proj g|= 3.18944D-02

At iterate 10 f= 2.26137D+00 |proj g|= 1.75196D-03

At iterate 15 f= 2.25957D+00 |proj g|= 1.20166D-03

* * *

Tit = total number of iterations

Tnf = total number of function evaluations

Tnint = total number of segments explored during Cauchy searches

Skip = number of BFGS updates skipped

Nact = number of active bounds at final generalized Cauchy point

Projg = norm of the final projected gradient

F = final function value

* * *

N Tit Tnf Tnint Skip Nact Projg F

4 18 21 1 0 0 8.724D-06 2.260D+00

F = 2.2595629677557780

CONVERGENCE: NORM_OF_PROJECTED_GRADIENT_<=_PGTOL

SARIMAX Results

==============================================================================

Dep. Variable: CPIAUCNS No. Observations: 224

Model: SARIMAX(1, 0, 1) Log Likelihood -506.142

Date: Mon, 30 Mar 2026 AIC 1020.284

Time: 12:18:01 BIC 1033.931

Sample: 04-01-1970 HQIC 1025.793

- 01-01-2026

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

outlier -14.5575 1.717 -8.480 0.000 -17.922 -11.193

ar.L1 0.9772 0.014 71.008 0.000 0.950 1.004

ma.L1 -0.5745 0.057 -10.092 0.000 -0.686 -0.463

sigma2 5.3281 0.474 11.231 0.000 4.398 6.258

===================================================================================

Ljung-Box (L1) (Q): 2.61 Jarque-Bera (JB): 2.16

Prob(Q): 0.11 Prob(JB): 0.34

Heteroskedasticity (H): 1.28 Skew: -0.09

Prob(H) (two-sided): 0.28 Kurtosis: 3.45

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

This problem is unconstrained.

We can also add additional structure to the model to remove seasonality using the by specifying values for the seasonal_order(p,d,q,s) argument. The final s parameter indicates the periodicity of the time series; the first three parameters are analogous to the parameters to the order arguement, but are applied with lags defined by the periodicity.

For example, since we’re working with quarterly data, it is natural to specify s=4. Setting p=1 and s=1 therefore takes 4-period differences of the data and includes an additional autoregressive term at a lag of 4.

inf_model3 = sm.tsa.SARIMAX(inf, order=(3, 0, 0), seasonal_order=(1, 1, 0, 4), exog=outlier)

inf_results3 = inf_model3.fit()

print(inf_results3.summary())

RUNNING THE L-BFGS-B CODE

* * *

Machine precision = 2.220D-16

N = 6 M = 10

At X0 0 variables are exactly at the bounds

At iterate 0 f= 2.26680D+00 |proj g|= 1.47627D-01

At iterate 5 f= 2.24409D+00 |proj g|= 3.24593D-03

At iterate 10 f= 2.24282D+00 |proj g|= 2.24330D-02

At iterate 15 f= 2.24052D+00 |proj g|= 1.48140D-03

* * *

Tit = total number of iterations

Tnf = total number of function evaluations

Tnint = total number of segments explored during Cauchy searches

Skip = number of BFGS updates skipped

Nact = number of active bounds at final generalized Cauchy point

Projg = norm of the final projected gradient

F = final function value

* * *

N Tit Tnf Tnint Skip Nact Projg F

6 18 21 1 0 0 3.794D-06 2.241D+00

F = 2.2405167990716035

CONVERGENCE: NORM_OF_PROJECTED_GRADIENT_<=_PGTOL

SARIMAX Results

=========================================================================================

Dep. Variable: CPIAUCNS No. Observations: 216

Model: SARIMAX(3, 0, 0)x(1, 1, 0, 4) Log Likelihood -483.952

Date: Mon, 04 Mar 2024 AIC 979.903

Time: 20:58:09 BIC 1000.043

Sample: 04-01-1970 HQIC 988.043

- 01-01-2024

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

outlier -11.1106 1.449 -7.670 0.000 -13.950 -8.271

ar.L1 0.4959 0.059 8.400 0.000 0.380 0.612

ar.L2 -0.0471 0.068 -0.697 0.486 -0.179 0.085

ar.L3 0.1884 0.064 2.967 0.003 0.064 0.313

ar.S.L4 -0.3854 0.059 -6.546 0.000 -0.501 -0.270

sigma2 5.6065 0.560 10.020 0.000 4.510 6.703

===================================================================================

Ljung-Box (L1) (Q): 0.47 Jarque-Bera (JB): 0.56

Prob(Q): 0.49 Prob(JB): 0.76

Heteroskedasticity (H): 1.14 Skew: -0.10

Prob(H) (two-sided): 0.59 Kurtosis: 3.14

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

This problem is unconstrained.

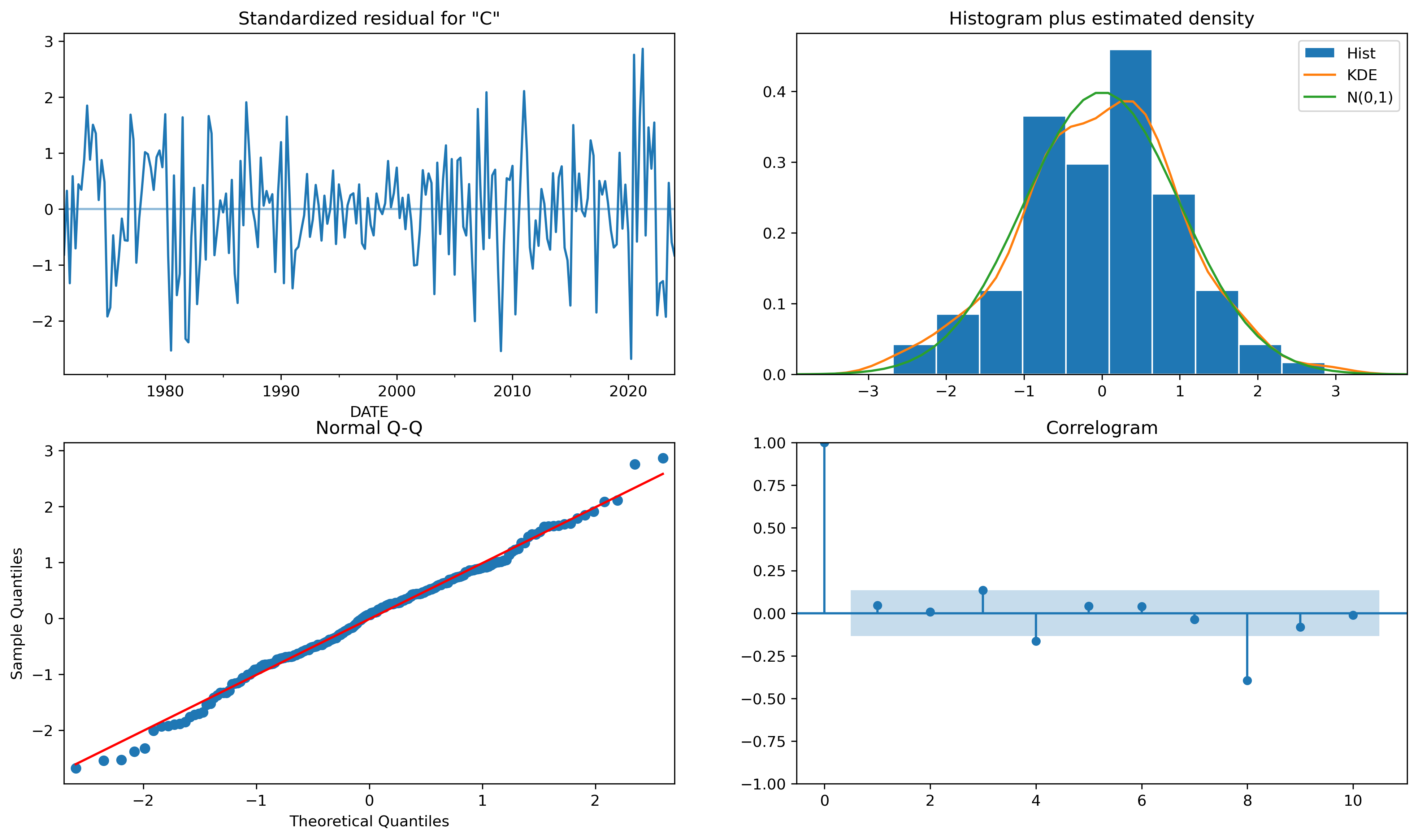

inf_results3.plot_diagnostics(figsize=(16,9));

inf_results3.forecast(4, exog=np.zeros(4))

2024-04-01 4.967205

2024-07-01 2.598361

2024-10-01 -0.654048

2025-01-01 1.485415

Freq: QS-JAN, Name: predicted_mean, dtype: float64